储蓄和金融系统

Section outline

-

Savings & the Financial Systems

::储蓄和金融系统- Companies can raise early-stage financial capital in several ways: from their owners’ or managers’ personal savings, or credit cards and from private investors like angel investors and venture capital firms.

Universal Generalizations

::普遍化-

Banks and other financial institutions provide opportunities for saving and investing by individuals, which in turn provides opportunities for businesses to borrow and expand.

::银行和其他金融机构为个人储蓄和投资提供机会,这反过来又为企业提供借贷和扩大的机会。

Guiding Questions

::问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问-

Why is it important for individuals to save and to invest?

::为什么个人储蓄和投资很重要? -

In addition to the depository institutions, what non-depository institutions exist to serve as financial intermediaries?

::除保存机构外,还有哪些非储存机构作为金融中介机构? -

What effect do interest rates have on levels of investment?

::利率对投资水平有什么影响? -

How do you assess risk before making an investment?

::在投资前如何评估风险? -

What types of accounts are offered to consumers? What are the costs associated with these accounts?

::向消费者提供哪类账户?与这些账户相关的费用是什么?

Video: Basics of Investing

::视频:投资的基本内容There are only two things you can do with money: save it or spend it. "Saving" means the absence of spending, while "savings" refers to dollars that are made available when people abstain from consumption. For an economic system to grow, there must be both saving and spending. People must save so that banks can lend the money to those that need to borrow it to buy things such as cars, homes, or pay for college or vacations. In addition, banks lend money to those who own businesses who need extra money to buy tools, equipment, build additional factories, hire more employees, or expand their business. Savings makes economic growth possible.

::只有两件事你可以用金钱做:储蓄或支出。“储蓄”是指没有支出,而“储蓄”是指当人们放弃消费时提供的美元。 经济体系要想增长,就必须有储蓄和支出。 人们必须储蓄,以便银行能够借钱购买汽车、住宅或支付大学或假期费用。 此外,银行还贷钱给那些需要额外钱购买工具、设备、建造更多工厂、雇用更多雇员或扩大业务的企业。 储蓄使得经济增长成为可能。Financial System

::金融系统金融系统The financial system , a network of savers, investors and financial institutions, works together to transfer savings to those that need it and that in turn helps the economy grow.

::金融系统是一个由储蓄者、投资者和金融机构组成的网络,它共同努力将储蓄转移给那些需要储蓄的人,而这反过来又有助于经济增长。The Financial System

::金融系统

(Source: )

)

Financial Assets

::金融资产There are various ways that people save and invest. A certificate of deposit (CD) is an interest-bearing loan to a bank, or the government, or a corporation. Because this is a type of investment, it is also called a financial asset or a claim on the property and the income of the borrower. This asset has value and it specifies the amount of money loaned and the terms of that loan, such as interest rate and due date. A certificate of deposit can be set up for a short amount of time, such as six months, or longer depending on the terms.

::储蓄和投资有多种方式。存款证明(CD)是银行、政府或公司的一种有息贷款。由于这是一种投资,它也被称为金融资产或对借款人财产和收入的债权。该资产有价值,并指明贷款金额和贷款条件,如利率和到期日。存款证明(CD)是给银行、政府或公司的一种有息贷款。由于这是一种投资,它也被称为金融资产或对借款人财产和收入的债权。该资产有价值,它规定贷款金额和贷款条件,如利率和到期日。存款证明(CD)可以在很短的时间内开立,例如六个月或更长的时间,视贷款条件而定。Financial Intermediaries

::金融中介机构A financial intermediary is a bank, however, there are non-financial intermediaries that also allow people to save and make loans to members. Households and businesses are the most important savers in the circular flow of economic activity, while governments and businesses are the largest borrowers. The smooth operation of these financial intermediaries ensures that savers have a place to save and borrowers have a place to go to get funds.

::然而,金融中介机构是一家银行,有非金融中介机构也允许人们储蓄和向成员提供贷款。 在经济活动循环流动中,家庭和企业是最重要的储蓄者,而政府和企业则是最大的借款人。 这些金融中介机构的顺利运作确保了储蓄者有地方储蓄,借款人有地方去获取资金。Examples of Non-financial Intermediaries

::非金融中介机构实例Finance companies are firms that specialize in making loans directly to consumers and in buying installment contracts from members who sell goods on credit. Merchants cannot wait for years for their customers to pay off high-cost items on an installment plan. Instead, the merchant sells the customer's installment contract to a finance company for a lump sum. This allows a merchant to advertise instant credit without having to carry the loan the full term or accept the risk involved in the loan. A good example of a finance company would be one that works with automobile manufacturers or car lots such as: Bank of America Merrill Lynch Dealer Financial Services, Chase Auto Finance, and Ford Motor Credit Company.

::金融公司是专门向消费者直接提供贷款和向以信贷方式出售货物的成员购买分期付款合同的公司,商人不能等多年才让客户在分期付款计划中支付高成本项目,相反,商人将客户的分期付款合同一次性卖给了一家金融公司,这样,商人就可以在无需承担贷款全额或接受贷款所涉风险的情况下立即做信贷广告。 金融公司的一个良好例子是与汽车制造商或汽车批量公司合作,例如:美国梅瑞尔银行、林奇经销商金融服务公司、大通自动金融公司和福特汽车信贷公司。To read more about financial companies read the Forbes article .

::更多关于金融公司的文章,A life insurance company 's primary purpose is to provide financial protection for survivors of the insured, however after insurance policies have been paid out by the company, it tends to have a great deal of cash on hand. This cash it then lent to others, or those people who have insurance policies may borrow against the policy based on what they have already given to the company. The loan from the insurance company must be paid back, plus interest.

::人寿保险公司的主要目的是为被保险人的遗属提供财务保护,然而,在保险单由公司支付后,它往往拥有大量现金,然后借给他人,或者那些持有保险单的人可以根据他们已经给予该公司的贷款来借给保险单,保险公司的贷款必须偿还,加上利息。A mutual fund is a company that sells stock in itself to individual investors and then invests the money it receives in stocks and bonds issued by other corporations. Mutual fund stockholders receive dividends earned from the mutual fund's investment. Stockholders can also sell their mutual fund shares for a profit just like other stocks. Mutual funds allow people to diversify without taking too much of a risk. The mutual fund company's assets are calculated by taking the net value of the mutual fund and dividing it by the number of shares issued by the mutual fund to find its market value.

::共同基金是一家公司,将股票本身出售给个人投资者,然后将所得资金投资于其他公司发行的股票和债券;共同基金股东从共同基金的投资中获得股息;共同基金股东也可以出售共同基金股份,以获得与其他股票一样的利润;共同基金允许人们在不承担太大风险的情况下实现多样化;共同基金公司的资产的计算方法是采用共同基金的净价值,将其除以共同基金发行的股票数量,以寻找其市场价值。Pension funds are set up to plan for the retirement or disability of employees. Workers have a portion or percentage of their pay withheld and placed in the pension fund. The managers of the fund then take that money and invest it in stocks, bonds, and mutual funds to earn more money. A portion of the pension fund is paid out to those employees who have retired or are no longer working for the company. A pension plan helps workers set aside money that they will need when they retire.

::设立退休基金是为了计划雇员的退休或残疾; 工人有部分或部分工资被扣留并存入退休基金; 基金管理者然后拿走这笔钱,将其投资于股票、债券和共同基金,以赚取更多的钱; 养恤金基金的一部分付给已经退休或不再为公司工作的雇员; 养恤金计划帮助工人在退休时保留他们需要的钱。REIT is a real estate investment trust . It is a company that is organized primarily to make loans to construction companies that build homes. This type of non-financial intermediary helps provide billions of dollars for home construction.

::REIT是一家房地产投资信托机构,其组织主要是为了向建造房屋的建筑公司提供贷款。 这种非金融中介机构帮助为房屋建设提供数十亿美元。No matter which type of financial or non-financial intermediary consumers use, the purpose is still the same, help consumers borrow available funds and participate in the circular flow of economic activity.

::无论金融或非金融中介消费者使用哪类金融或非金融中介消费者,目的仍然不变,帮助消费者借用可用资金并参与经济活动的循环流动。Demand and Supply in Financial Markets

::金融市场的需求和供应United States’ households and businesses saved almost $2.9 trillion in 2012. Where did that savings go and what was it used for? Some of the savings ended up in banks, which in turn loaned the money to individuals or businesses that wanted to borrow money. Some was invested in private companies or loaned to government agencies that wanted to borrow money to raise funds for purposes like building roads or mass transit. Some firms reinvested their savings in their own businesses.

::美国家庭和企业在2012年储蓄了近2.9万亿美元。 2012年,美国家庭和企业储蓄了近2.9万亿美元。 储蓄去向何方及其用途? 一些储蓄最终出现在银行,而银行又将资金借给想借钱的个人或企业。 有些投资于私人公司或借给想借钱以修建公路或大众交通等目的筹集资金的政府机构。 一些公司将储蓄再投资于自己的企业。In this section, we will determine how the demand and supply model links those who wish to supply financial capital (i.e., savings) with those who demand financial capital (i.e., borrowing). Those who save money (or make financial investments, which is the same thing), whether individuals or businesses are on the supply side of the financial market. Those who borrow money are on the demand side of the financial market.

::在本节中,我们将确定供求模式如何将那些希望提供金融资本(即储蓄)的人与那些要求金融资本(即借贷)的人联系起来,那些储蓄资金(或进行金融投资,这是同样的事情)的人,个人或企业是否在金融市场的供应方,那些借钱的人是在金融市场的需求方。Who Demands and Who Supplies in Financial Markets?

::谁在金融市场中提出要求,谁在金融市场中供应?In any market, the price is what suppliers receive and what demanders pay. In financial markets, those who supply financial capital through saving expect to receive a rate of return, while those who demand financial capital by receiving funds expect to pay a rate of return. This rate of return can come in a variety of forms, depending on the type of investment.

::在任何市场中,价格都是供应商得到的,需求者要付出什么代价。 在金融市场中,通过储蓄提供金融资本的人期望得到回报率,而通过接受资金要求金融资本的人则期望得到回报率。 这一回报率可以有多种形式,取决于投资类型。The simplest example of a rate of return is the interest rate. For example, when you supply money into a savings account at a bank, you receive interest on your deposit. The interest paid to you as a percent of your deposits is the interest rate. Similarly, if you demand a loan to buy a car or a computer, you will need to pay interest on the money you borrow.

::回报率的最简单例子就是利率。例如,当您向银行储蓄账户提供资金时,您将获得存款的利息。按存款的一定百分比向您支付的利息是利率。同样,如果您要求贷款购买汽车或计算机,您需要为您借的钱支付利息。Let’s consider the market for borrowing money with credit cards. In 2012, more than 180 million Americans were cardholders. Credit cards allow you to borrow money from the card's issuer, and pay back the borrowed amount plus interest, though most allow you a period of time in which you can repay the loan without paying interest. A typical credit card interest rate ranges from 12% to 18% per year. In 2010, Americans had about $900 billion outstanding in credit card debts. About half of U.S. families with credit cards report that they almost always pay the full balance on time, but one-quarter of U.S. families with credit cards say that they “hardly ever” pay off the card in full. In fact, as of March 2013, CreditCards.com reported that nearly two out of every five Americans (39%) carry credit card debt from one month to the next. Let’s say that, on average, the annual interest rate for credit card borrowing is 15% per year. So, Americans pay tens of billions of dollars every year in interest on their credit cards—plus basic fees for the credit card or fees for late payments.

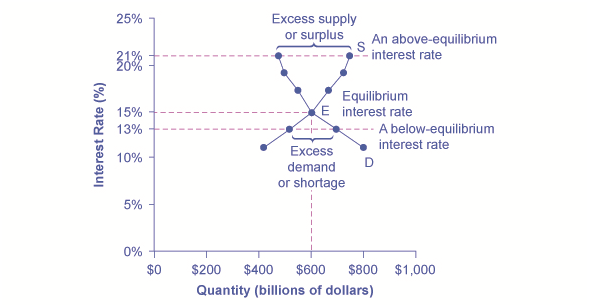

::让我们来考虑用信用卡借钱的市场。 2012年,超过1.8亿美国人是持卡人。 信用卡允许你从开卡人那里借钱,还回借借金额加上利息,尽管大部分人允许你用一段时间偿还贷款而不付利息。 典型的信用卡利率从每年12 % 至 18 % 。 2010年,美国人的信用卡债务约为9 000亿美元。 大约一半持有信用卡的美国家庭报告说,他们几乎总是按时全额支付余额,但四分之一持有信用卡的美国家庭说,他们“从未”全额支付信用卡。 事实上,截至2013年3月,信用卡公司(CreditCards.com)报告,每5个美国人中就有近2个(39 % ) 将信用卡债务从1个月持续到下一个月。 比方说,信用卡借款的年利率平均为每年15 % 。 因此,美国人每年为信用卡支付数十亿美元利息 — — 再加上信用卡的基本费用或逾期付款费用。2 illustrates demand and supply in the financial market for credit cards. The horizontal axis of the financial market shows the quantity of money that is loaned or borrowed in this market. The vertical or price axis shows the rate of return, which in the case of credit card borrowing can be measured with an interest rate. 1 shows the quantity of financial capital that consumers demand at various interest rates and the quantity that credit card firms (often banks) are willing to supply.

::2说明信用卡金融市场的供需情况。金融市场的横向轴线显示在该市场借入或借入的资金数量。纵向轴线或价格轴线显示收益率,在信用卡借贷的情况下,回报率可以用利率来衡量。 1 显示消费者以各种利率要求的金融资本数量以及信用卡公司(通常是银行)愿意提供的数量。- Demand and Supply for Borrowing Money with Credit Cards

In this market for credit card borrowing, the demand curve (D) for borrowing financial capital intersects the supply curve (S) for lending financial capital at equilibrium €. At the equilibrium, the interest rate (the “price” in this market) is 15% and the quantity of financial capital being loaned and borrowed is $600 billion. The equilibrium price is where the quantity demanded and the quantity supplied are equal. At an above-equilibrium interest rate like 21%, the quantity of financial capital supplied would increase to $750 billion, but the quantity demanded would decrease to $480 billion. At a below-equilibrium interest rate like 13%, the quantity of financial capital demanded would increase to $700 billion, but the quantity of financial capital supplied would decrease to $510 billion.

::在这个信用卡借贷市场中,借贷金融资本的需求曲线(D)交叉了以平衡欧元借出金融资本的供给曲线(S ) 。 在平衡时,利率(这个市场的“价格 ” ) 为15%,借出和借出金融资本的数量为6000亿美元。 平衡价格是需求数量和供应数量相等的地方。 在平衡利率(如21%)高于平衡利率的情况下,所提供金融资本的数量将增加到7500亿美元,但所需数量将下降到4800亿美元。 在平衡利率(即13%)以下,所需金融资本的数量将增加到7000亿美元,但所提供金融资本的数量将下降到5100亿美元。Demand and Supply for Borrowing Money with Credit Cards

::以信用卡借款的资金的需求和供应Interest Rate (%)

::利率(%)Quantity of Financial Capital Demanded (Borrowing) ($ billions)

::所需金融资本(借款)数量(10亿美元)Quantity of Financial Capital Supplied (Lending) ($ billions)

::供应(贷款)的金融资本数量(10亿美元)11

$800

$420

13

$700

$510

15

$600

$600

17

$550

$660

19

$500

$720

21

$480

$750

The laws of demand and supply continue to apply in the financial markets. According to the law of demand, a higher rate of return (that is, a higher price) will decrease the quantity demanded. As the interest rate rises, consumers will reduce the quantity that they borrow. According to the law of supply, higher price increases the quantity supplied. Consequently, as the interest rate paid on credit card borrowing rises, more firms will be eager to issue credit cards and to encourage customers to use them. Conversely, if the interest rate on credit cards falls, the quantity of financial capital supplied in the credit card market will decrease and the quantity demanded will fall.

::根据需求法,较高的回报率(即更高的价格)将减少所需数额; 随着利率的上升,消费者将减少借款额; 根据供应法,更高的价格将增加供应量; 因此,随着信用卡借贷利率的上升,更多的公司将急于发放信用卡并鼓励客户使用信用卡; 相反,如果信用卡利率下降,信用卡市场提供的金融资本数量将减少,所需数额也将下降。Equilibrium in Financial Markets

::金融市场的平衡In the financial market for credit cards shown in 2, the supply curve (S) and the demand curve (D) cross at the equilibrium point (E). The equilibrium occurs at an interest rate of 15%, where the quantity of funds demanded and the quantity supplied are equal at an equilibrium quantity of $600 billion.

::在2中显示的信用卡金融市场中,在平衡点(E),供应曲线(S)和需求曲线(D)交叉。 平衡以15%的利率发生,要求的资金数量和供应的数量相等,平均数量为6 000亿美元。If the interest rate (remember, this measures the “price” in the financial market) is above the equilibrium level, then an excess supply, or a surplus, of financial capital will arise in this market. For example, at an interest rate of 21%, the quantity of funds supplied increases to $750 billion, while the quantity demanded decreases to $480 billion. At this above-equilibrium interest rate, firms are eager to supply loans to credit card borrowers, but relatively few people or businesses wish to borrow. As a result, some credit card firms will lower the interest rates (or other fees) they charge to attract more business. This strategy will push the interest rate down toward the equilibrium level.

::如果利率(记住,这衡量金融市场的“价格 ” ) 高于平衡水平,那么金融市场就会出现金融资本过剩或盈余。 比如,以21%的利率计算,所提供资金的数量将增至7500亿美元,而所需数量则将降至4800亿美元。 以这种平衡利率计算,公司渴望向信用卡借款人提供贷款,但希望借款的人或企业相对较少。 因此,一些信用卡公司将降低利率(或其他收费 ) , 以吸引更多的企业。 这一战略将把利率降低到平衡水平。If the interest rate is below the equilibrium, then excess demand or a shortage of funds occurs in this market. At an interest rate of 13%, the quantity of funds credit card borrowers demand increases to $700 billion; but the quantity credit card firms are willing to supply is only $510 billion. In this situation, credit card firms will perceive that they are overloaded with eager borrowers and conclude that they have an opportunity to raise interest rates or fees. The interest rate will face economic pressures to creep up toward the equilibrium level.

::如果利率低于平衡水平,那么这个市场就会出现超额需求或资金短缺。 以13%的利率计算,资金信用卡借款人的需求量将增加到7000亿美元;但信用卡公司愿意提供的数量只有5100亿美元。 在这种情况下,信用卡公司会发现他们已经与热心的借款人过量,并得出结论他们有机会提高利率或收费。 利率将面临向平衡水平攀升的经济压力。Shifts in Demand and Supply in Financial Markets

::金融市场需求和供应变化Those who supply financial capital face two broad decisions: how much to save, and how to divide up their savings among different forms of financial investments. We will discuss each of these in turn.

::那些提供金融资本的人面临两大决定:储蓄多少,以及如何将其储蓄分成不同形式的金融投资,我们将依次讨论其中的每一项。Participants in financial markets must decide when they prefer to consume goods: now or in the future. Economists call this inter-temporal decision making because it involves decisions across time. Unlike a decision about what to buy from the grocery store, decisions about investment or saving are made across a period of time, sometimes a long period.

::金融市场的参与者必须决定他们更愿意何时消费商品:现在还是将来。 经济学家称这种时际决策是时间间决策,因为它涉及时间间决策。 与从杂货店购买什么的决定不同,投资或储蓄的决定是在一段时间内做出的,有时是很长的一段时间。Most workers save for retirement because their income in the present is greater than their needs, while the opposite will be true once they retire. So they save today and supply financial markets. If their income increases, they save more. If their perceived situation in the future changes, they change the amount of their saving. For example, there is some evidence that Social Security, the program that workers pay into in order to qualify for government checks after retirement, has tended to reduce the quantity of financial capital that workers save. If this is true, Social Security has shifted the supply of financial capital at any interest rate to the left.

::大部分工人储蓄退休,因为他们目前的收入高于其需要,而退休后情况则相反。因此,他们今天储蓄并供应金融市场。如果他们的收入增加,他们储蓄更多。如果他们认为未来情况会发生变化,他们就会改变储蓄数额。例如,有证据表明,工人为退休后获得政府检查资格而支付工资的社会保障计划往往会减少工人储蓄的金融资本数量。 如果确实如此,社会保障已经将任何利率的金融资本供应转移到了左边。By contrast, many college students need money today when their income is low (or nonexistent) to pay their college expenses. As a result, they borrow today and demand from financial markets. Once they graduate and become employed, they will pay back the loans. Individuals borrow money to purchase homes or cars. A business seeks financial investment so that it has the funds to build a factory or invest in a research and development project that will not pay off for five years, ten years, or even more. So when consumers and businesses have greater confidence that they will be able to repay in the future, the quantity demanded of financial capital at any given interest rate will shift to the right.

::相比之下,许多大学生在收入低(或根本不存在)时需要钱来支付大学开支,因此,他们现在需要钱来支付大学开支。因此,他们现在要借钱和金融市场需求。一旦他们毕业并就业,他们就会偿还贷款。 个人借钱购买房屋或汽车。 企业寻求金融投资,以便拥有资金来建造工厂或投资一个五年、十年甚至更长时间无法偿还的研发项目。 因此,当消费者和企业更有信心将来能够偿还债务时,以任何特定利率要求的金融资本数量将转移到右翼。For example, in the technology boom of the late 1990s, many businesses became extremely confident that investments in new technology would have a high rate of return, and their demand for financial capital shifted to the right. Conversely, during the Great Recession of 2008 and 2009, their demand for financial capital at any given interest rate shifted to the left.

::例如,在1990年代后期的技术繁荣中,许多企业对新技术投资的回报率将很高,对金融资本的需求将转向右翼。 相反,在2008年和2009年大衰退期间,它们以任何特定利率对金融资本的需求将转向左翼。To this point, we have been looking at saving in total. Now let us consider what affects saving in different types of financial investments. In deciding between different forms of financial investments, suppliers of financial capital will have to consider the rates of return and the risks involved. Rate of return is a positive attribute of investments, but risk is a negative. If Investment A becomes more risky, or the return diminishes, then savers will shift their funds to Investment B—and the supply curve of financial capital for Investment A will shift back to the left while the supply curve of capital for Investment B shifts to the right.

::在这一点上,我们一直在研究总储蓄问题。 现在让我们考虑一下不同类型金融投资的储蓄影响。 在决定不同形式的金融投资时,金融资本的提供者必须考虑回报率和所涉风险。 收益率是投资的积极属性,但风险是负的。 如果投资A风险更大,或者收益减少,那么储蓄者将把资金转向投资B — — 投资A的金融资本供应曲线将转向左边,而投资B的资本供应曲线则转向右边。Price Ceilings in Financial Markets: Usury Laws

::金融市场的物价上限:高贵法律As we noted earlier, more than 180 million Americans own credit cards, and their interest payments and fees total tens of billions of dollars each year. It is little wonder that political pressures sometimes arise for setting limits on the interest rates or fees that credit card companies charge. The firms that issue credit cards, including banks, oil companies, phone companies, and retail stores, respond that the higher interest rates are necessary to cover the losses created by those who borrow on their credit cards and who do not repay on time or at all. These companies also point out that cardholders can avoid paying interest if they pay their bills on time.

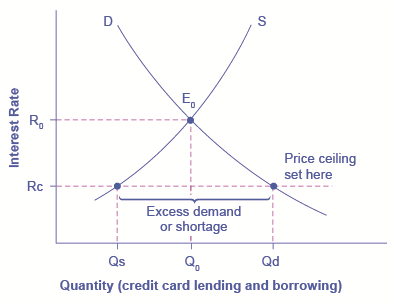

::正如我们早些时候指出的,每年超过1.8亿美国人拥有信用卡,他们的利息支付和手续费总额每年达数千亿美元。 毫不奇怪,对信用卡公司收取的利率或收费设定限制有时会产生政治压力。 发行信用卡的公司,包括银行、石油公司、电话公司和零售商店,回应说高利率对于弥补信用卡借款人和不按时或根本不还债人造成的损失是必要的。 这些公司还指出,持卡人如果按时支付账单,可以避免支付利息。Consider the credit card market as illustrated in 3. In this financial market, the vertical axis shows the interest rate (which is the price in the financial market). Demanders in the credit card market are households and businesses; suppliers are the companies that issue credit cards. This figure does not use specific numbers, which would be hypothetical in any case, but instead focuses on the underlying economic relationships. Imagine a law imposes a price ceiling that holds the interest rate charged on credit cards at the rate Rc, which lies below the interest rate R 0 that would otherwise have prevailed in the market. The price ceiling is shown by the horizontal dashed line in 3. The demand and supply model predicts that at the lower price ceiling interest rate, the quantity demanded of credit card debt will increase from its original level of Q 0 to Qd; however, the quantity supplied of credit card debt will decrease from the original Q 0 to Qs. At the price ceiling (Rc), quantity demanded will exceed quantity supplied. Consequently, a number of people who want to have credit cards and are willing to pay the prevailing interest rate will find that companies are unwilling to issue cards to them. The result will be a credit shortage.

::考虑信贷卡市场(见3.),在这个金融市场中,垂直轴线显示利率(即金融市场的价格);信用卡市场的需求者是家庭和企业;供应商是发放信用卡的公司;该数字没有使用特定数字,无论如何都是假设的,而是侧重于潜在的经济关系。设想一项法律规定一个最高价格,将信用卡收取的利率维持在Rc利率之下,该利率维持在R0利率之下,否则在市场上会占上风;最高价格由3的横向破折线显示。 供求模式预测,在较低的价格上限利率下,信用卡债务要求的数量将从原来的Q0到Qd水平上增加;然而,信用卡债务供应的数量将从原来的Q0到Qs下降。在最高价格(Rc)下,所需数额将超过供应的数量。因此,一些想要获得信用卡并愿意支付当前利率的人会发现,公司不愿意向他们发放卡。结果将是信用短缺。- Credit Card Interest Rates: Another Price Ceiling Example

The original intersection of demand D and supply S occurs at equilibrium E 0 . However, a price ceiling is set at the interest rate Rc, below the equilibrium interest rate R 0 , and so the interest rate cannot adjust upward to the equilibrium. At the price ceiling, the quantity demanded, Qd, exceeds the quantity supplied, Qs. There is excess demand, also called a shortage.

::需求D和供应S的最初交叉点是在E0平衡点。 但是,将利率上限设定在低于平衡利率R0的Rc利率之下,因此利率无法向上调整到平衡点。 在价格上限上,要求的数量QD超过供应的数量Qs。 存在需求过剩,也被称为短缺。Many states do have usury laws, which impose an upper limit on the interest rate that lenders can charge. However, in many cases these upper limits are well above the market interest rate. For example, if the interest rate is not allowed to rise above 30% per year, it can still fluctuate below that level according to market forces. A price ceiling that is set at a relatively high level is non-binding, and it will have no practical effect unless the equilibrium price soars high enough to exceed the price ceiling.

::许多州确实有高利贷法,对放款人可以收取的利率规定了上限。 但是,在许多情况下,这些上限远远高于市场利率。 比如,如果利率不能每年超过30%,根据市场力量,它仍然可以低于这一水平。 相对较高的最高限价是不具约束力的,除非均衡价格猛涨到足以超过最高限价,否则它不会产生实际效果。In the demand and supply analysis of financial markets, the “price” is the rate of return or the interest rate received. The quantity is measured by the money that flows from those who supply financial capital to those who demand it.

::在对金融市场的供需分析中,“价格”是收益率或收到的利率,数量用从提供金融资本者流向需求者的资金来衡量。Two factors can shift the supply of financial capital to a certain investment: if people want to alter their existing levels of consumption, and if the riskiness or return on one investment changes relative to other investments. Factors that can shift demand for capital include business confidence and consumer confidence in the future—since financial investments received in the present are typically repaid in the future.

::有两个因素可以将金融资本的供应转向某种投资:如果人们想改变其现有的消费水平,如果一种投资相对于其他投资的风险或回报率,可以改变对资本的需求的因素包括商业信心和消费者对未来的信心,因为目前收到的金融投资通常在今后偿还。

Many people choose to purchase their home rather than rent. This chapter explores how the global financial crisis has influenced home ownership. (Credit: modification of work by Diana Parkhouse/Flickr Creative Commons)

The Housing Bubble and the Financial Crisis of 2007

::2007年住房泡沫和金融危机In 2006, housing equity in the United States peaked at $13 trillion. That means that the market prices of homes, less what was still owed on the loans used to buy these houses, equaled $13 trillion. This was a very good number, since the equity represented the value of the financial asset most U.S. citizens owned.

::2006年,美国住房产权最高值为13万亿美元。 这意味着房屋市场价格减去购买这些房屋的贷款所拖欠的金额,相当于13万亿美元。 这是一个非常好的数字,因为股权代表了美国大多数公民拥有的金融资产的价值。However, by 2008 this number had gone down to $8.8 trillion, and it declined further still in 2009. Combined with the decline in value of other financial assets held by U.S. citizens, by 2010, U.S. homeowners’ wealth had declined by $14 trillion! This is a staggering result, and it affected millions of lives: people had to alter their retirement decisions, housing decisions, and other important consumption decisions. Just about every other large economy in the world suffered a decline in the market value of financial assets, as a result of the global financial crisis of 2008–2009.

::然而,到2008年,这一数字已经下降到8.8万亿美元,2009年还会进一步下降。 加上美国公民持有的其他金融资产价值的下降,到2010年,美国房主的财富已经下降了14万亿美元。 这是一个惊人的结果,它影响到数百万人的生活:人们不得不改变退休决定、住房决定和其他重要的消费决定。 与世界上其他所有大型经济体一样,由于2008-2009年全球金融危机,金融资产的市场价值也下降了。This chapter will explain why people buy houses (other than as a place to live), why they buy other types of financial assets, and why businesses sell those financial assets in the first place. The chapter will also give us insight into why financial markets and assets go through boom and bust cycles like the one described here.

::本章将解释人们为什么买房(而不是作为生活的地方 ) , 为什么他们买其他类型的金融资产,为什么企业首先出售这些金融资产。 本章还将让我们深入了解金融市场和资产为什么像这里描述的那样经历繁荣和萧条的周期。When a firm needs to buy new equipment or build a new facility, it often must go to the financial market to raise funds. Usually firms will add capacity during an economic expansion when profits are on the rise and consumer demand is high. Business investment is one of the critical ingredients needed to sustain economic growth. Even in the sluggish economy of 2009, U.S. firms invested $1.4 trillion in new equipment and structures, in the hope that these investments would generate profits in the years ahead.

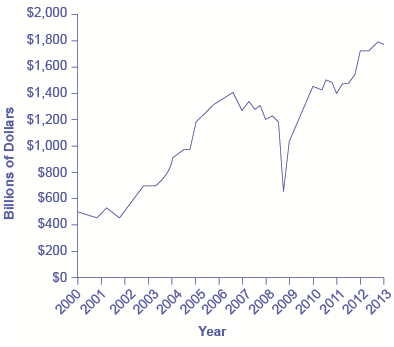

::当企业需要购买新设备或建造新设施时,它往往必须去金融市场筹集资金。 通常,当利润增加,消费者需求高时,公司会在经济扩张期间增加能力。 商业投资是维持经济增长的关键要素之一。 即使在2009年的疲软经济中,美国公司也在新的设备和结构上投资了1.4万亿美元,希望这些投资在未来几年能产生利润。Between the end of the recession in 2009 through the second quarter 2013, profits for the S&P 500 companies grew to 9.7 % despite the weak economy, with much of that amount driven by cost cutting and reductions in input costs, according to the Wall Street Journal . 5 shows corporate profits after taxes (adjusted for inventory and capital consumption). Despite the steep decline in quarterly net profit in 2008, profits have recovered and surpassed pre-Recession levels.

::2009年衰退结束至2013年第二季度期间,尽管经济疲软,但S & P 500公司的利润仍增长至9.7%,其中很大一部分是由成本削减和投入成本降低驱动的,据《华尔街日报》称。 5 显示公司在税后利润(按库存和资本消耗调整 ) 。 尽管2008年季度净利润大幅下降,但利润已经恢复并超过了衰退前的水平。Corporate Profits After Tax (Adjusted for Inventory and Capital Consumption)

::公司税后利润(库存和资本消费调整)Since 2000, corporate profits after tax have mostly continued to increase each year save for a substantial decrease between 2008 and 2009. (Source: )

Many firms, from huge companies like General Motors to startup firms writing computer software, do not have the financial resources within the firm to make all the desired investments. These firms need financial capital from outside investors, and they are willing to pay interest for the opportunity to get a rate of return on the investment for that financial capital.

::许多公司,从通用汽车公司等大型公司到编写计算机软件的新建公司,都不具备公司内部的财政资源来进行所有理想投资。 这些公司需要外部投资者的金融资本,它们愿意为获得投资回报率的机会支付利息。On the other side of the financial capital market, suppliers of financial capital, like households, wish to use their savings in a way that will provide a return. Individuals cannot, however, take the few thousand dollars that they save in any given year, write a letter to General Motors or some other firm, and negotiate to invest their money with that firm. Financial capital markets bridge this gap: that is, they find ways to take the inflow of funds from many separate suppliers of financial capital and transform it into the funds desired by demanders of financial capital. Such financial markets include stocks, bonds, bank loans, and other financial investments.

::在金融资本市场的另一侧,金融资本的提供者,像家庭一样,希望以能够带来回报的方式利用储蓄。 然而,个人不能拿出他们在任何特定年份储蓄的几千美元,写一封信给通用汽车公司或其他公司,并谈判将其资金投给该公司。 金融资本市场缩小了这一差距:即他们找到办法从许多不同的金融资本提供者处吸收资金流入,并将其转化为金融资本需求者所希望的资金。 这些金融市场包括股票、债券、银行贷款和其他金融投资。Our perspective then shifts to consider how these financial investments appear to suppliers of capital such as the households that are saving funds. Households have a range of investment options: bank accounts, certificates of deposit, money market mutual funds, bonds, stocks, stock and bond mutual funds, housing, and even tangible assets like gold. Finally, the chapter investigates two methods for becoming rich: a quick and easy method that does not work very well at all, and a slow, reliable method that can work very well indeed over a lifetime.

::然后,我们的观点转向考虑这些金融投资如何出现在资本提供者(比如储蓄资金的家庭)身上。 家庭有一系列投资选择:银行账户、存款单、货币市场共同基金、债券、股票、股票、股票和债券共同基金、住房,甚至金等有形资产。 最后,本章探讨了两种致富的方法:一种是效果极差的快速易行方法,另一种是一生可以非常成功的缓慢、可靠方法。Mutual Funds

::互助基金Buying stocks or bonds issued by a single company is always somewhat risky. An individual firm may find itself buffeted by unfavorable supply and demand conditions or hurt by unlucky or unwise managerial decisions. Thus, a standard recommendation from financial investors is diversification, which means buying stocks or bonds from a wide range of companies. A saver who diversifies is following the old proverb: “Don’t put all your eggs in one basket.” In any broad group of companies, some firms will do better than expected and some will do worse—but the extremes have a tendency to cancel out extreme increases and decreases in value.

::由一家单一公司发行的购买股票或债券总是有些风险。 单个公司可能发现自己受到不利的供求条件的冲击,或受到不善或不明智的管理决定的伤害。 因此,金融投资者的标准建议是多样化,这意味着从各种各样的公司购买股票或债券。 分散投资的储蓄者遵循古老的谚语 : “ 不要把所有的鸡蛋都放在一个篮子里。 ”在任何广泛的公司集团中,有些公司会做得比预期的好,有些公司会做得更糟 — — 但极端的情况倾向于取消价值的极端增减。Purchasing a diversified group of the stocks or bonds has gotten easier in the Internet age, but it remains something of a task. To simplify the process, companies offer mutual funds, which are organizations that buy a range of stocks or bonds from different companies. The financial investor buys shares of the mutual fund, and then receives a return based on how the fund as a whole performs. In 2012, according to the Investment Company Factbook, about 44% of U.S. households had a financial investment in a mutual fund—including many people who have their retirement savings or pension money invested in this way.

::购买多样化的股票或债券集团在互联网时代已经变得更加容易,但是这仍然是一个任务。为了简化程序,公司提供共同基金,这是从不同公司购买一系列股票或债券的组织。 金融投资者购买共同基金的股份,然后根据整个基金的业绩获得回报。 2012年,根据投资公司《概况介绍》,大约44%的美国家庭在共同基金中进行了金融投资,包括许多退休储蓄或养老金投资的人。Mutual funds can be focused in certain areas: one mutual fund might invest only in stocks of companies based in Indonesia, or only in bonds issued by large manufacturing companies, or only in stock of biotechnology companies. At the other end of the spectrum, a mutual fund might be quite broad; at the extreme, some mutual funds own a tiny share of every firm in the stock market, and thus the value of the mutual fund will fluctuate with the average of the overall stock market. A mutual fund that seeks only to mimic the overall performance of the market is called an index fund.

::互助基金可以集中在某些领域:一个互助基金可能只投资于设在印度尼西亚的公司股票,或只投资于大型制造公司发行的债券,或只投资于生物技术公司的股票;另一方面,互助基金可能相当广泛;在最极端的情况下,一些互助基金拥有股市中每一家公司的一小部分,因此,互助基金的价值将与整个股票市场的平均价值波动;一个只试图模仿市场总体业绩的共同基金称为指数基金。Diversification can offset some of the risks of individual stocks rising or falling. Even investors who buy an indexed mutual fund designed to mimic some measure of the broad stock market, like the Standard & Poor’s 500, had better buckle their seat-belts against some ups and downs, like those the stock market experienced in the first decade of the 2000s. In 2008 average U.S. stock funds declined 38%, reducing the wealth of individuals and households. This steep drop in value hit hardest those who were close to retirement and were counting on their stock funds to supplement retirement income.

::多样化可以抵消个别股票上升或下降的某些风险。 即使那些购买一个指数化共同基金以模仿大股市的某些规模(如标准普尔的500美元 ) 的投资者,其安全带也比2000年代头十年的股票市场更能扣住一些安全带来抵消一些起伏。 2008年,美国平均股票基金下跌了38 % , 减少了个人和家庭的财富。 这一价值的急剧下降对接近退休并依靠其股票基金来补充退休收入的人打击最大。The bottom line on investing in mutual funds is that the rate of return over time will be high; the risks are also high, but the risks and returns for an individual mutual fund will be lower than those for an individual stock. As with stocks, liquidity is also high provided the mutual fund or stock index fund is readily traded.

::共同基金投资的底线是,随着时间的推移,回报率将很高;风险也很高,但单个共同基金的风险和回报率将低于单个股票的风险和回报率,与股票一样,如果共同基金或股票指数基金易于交易,流动性也很高。How Capital Markets Transform Financial Flows

::资本市场如何改变资金流动Financial capital markets have the power to repackage money as it moves from those who supply financial capital to those who demand it. Banks accept checking account deposits and turn them into long-term loans to companies. Individual firms sell shares of stock and issue bonds to raise capital. Firms make and sell an astonishing array of goods and services, but an investor can receive a return on the company’s decisions by buying stock in that company. Stocks and bonds are sold and resold by financial investors to one another. Venture capitalists and angel investors search for promising small companies. Mutual funds combine the stocks and bonds—and thus, indirectly, the products and investments—of many different companies.

::金融资本市场有权重新包装资金,因为资金从那些提供金融资本的人转移到那些要求资金的人。银行接受支票帐户存款,并将它们变成对公司的长期贷款。 个别公司出售股票股份,发行债券来筹集资本。 公司制造和销售一系列惊人的商品和服务,但投资者可以通过购买公司股票来获得公司决策的回报。 股票和债券被金融投资者相互出售和转售。 风险资本家和天使投资者寻找有前途的小公司。 共同基金将许多不同公司的股票和债券 — — 从而间接地将产品和投资 — — 合并在一起。In this chapter, we discussed the basic mechanisms of financial markets. The fundamentals of those financial capital markets remain the same: Firms are trying to raise financial capital and households are looking for a desirable combination of rate of return, risk, and liquidity. Financial markets are society’s mechanisms for bringing together these forces of demand and supply.

::在本章中,我们讨论了金融市场的基本机制。 这些金融资本市场的基本原理依然不变:公司正在试图增加金融资本,家庭正在寻求将收益率、风险和流动性结合起来。 金融市场是社会整合这些供需力量的机制。Answer the self check questions below to monitor your understanding of the concepts in this section.

::回答下面的自我核对问题,以监测你对本节概念的理解。Self Check Questions

::自查问题1. Define the terms "saving" and "savings."

::1. 界定 " 储蓄 " 和 " 储蓄 " 这两个术语的定义。2. Why is it important for individuals to save?

::2. 为什么个人储蓄很重要?3. What is a financial system?

::3. 什么是金融体系?4. Define "certificate of deposit," "financial asset," and "financial intermediary."

::4. 定义“存款证书”、“金融资产”和“金融中介”。5. How does the circular flow of funds work?

::5. 循环资金流动如何运作?6. Which sector of the economy has the largest savers?

::6. 哪个经济部门的储蓄者最多?7. Which sector of the economy has the largest borrowers?

::7. 哪个经济部门的借款人最多?8. List examples of nonbank financial intermediaries.

::8. 非银行金融中介机构的例子清单。9. Define the term "finance company" and give an example.

::9. 给 " 金融公司 " 一词下定义并举一个例子。10. Define the term "life insurance company" and give an example.

::10. 界定“人寿保险公司”一词,并举一例。11. Define the term "mutual fund" and give an example.

::11. 界定 " 互助基金 " 一词,并举一例。12. Define the term "pension fund" and give an example.

::12. 定义“养恤基金”一词,并举一个例子。13. Define the term "real estate investment trusts."

::13. 界定“房地产投资信托”一词的定义。