货币政策、银行业和经济

章节大纲

-

Monetary Policy, Banking & the Economy

::货币政策、银行业和经济The crucial question is how long will it take for the Fed’s policies to affect the economy? The influence of the Federal Reserve and monetary policy is enormous and complex. Not even the Fed can truly calculate exactly what will happen in the short-run or the long-run when it conducts monetary policy because there are various other issues to consider such as the timing and burden of that policy. When all the elements of the economic performance are analyzed and monetary policy is adjusted, the Fed may find the economy is difficult to “fine-tune”.

::关键的问题是美联储政策影响经济需要多长时间? 美联储和货币政策的影响是巨大而复杂的。 即使是美联储也无法真正准确计算在短期或长期实施货币政策时会发生什么,因为还有其他各种问题需要考虑,比如该政策的时间和负担。 当对经济表现的所有要素进行分析并调整货币政策时,美联储可能发现经济难以“稳健 ” 。Universal Generalizations

::普遍化-

Changes in the money supply affect the interest rate, the availability of credit, and the price level.

::货币供应的变化影响到利率、信贷供应和价格水平。 -

Expansion and contraction of the money supply affect the cost of credit.

::货币供应的扩大和收缩影响到信贷成本。 -

The quantity theory of money has been repeated throughout history.

::金钱的数量理论在整个历史中反复出现。

Guiding Questions

::问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问-

What is the short-run impact of monetary policy?

::货币政策的短期影响是什么? -

Why do people view the interest rate as a measurement of the overall health of the economy?

::为什么人们认为利率是衡量经济总体健康的一个尺度? -

Why does the Fed try to avoid political confrontations, especially during election years?

::为什么美联储试图避免政治对抗,

This table shows the different types of money commonly defined by economists. The bottom represents the most liquid forms of money, M0, which is used primarily as a means of exchange. The broadest measure of money defined here is M3. This includes forms of money used as a store of value.

::本表显示了经济学家通常定义的不同货币类型。 底部代表最流动的货币形式,即货币M0,主要用作交换手段。 这里定义的最宽泛货币衡量尺度是M3, 包括用作价值储存的货币形式。Cash in your pocket certainly serves as money, but what about checks or credit cards? Are they money, too? Rather than trying to state a single way of measuring money, economists offer broader definitions of money based on liquidity. Liquidity refers to how quickly a financial asset can be used to buy a good or service. For example, cash is very liquid. Your $10 bill can be easily used to buy a hamburger at lunchtime. However, $10 that you have in your savings account is not so easy to use. You must go to the bank or ATM machine and withdraw that cash to buy your lunch. Thus, $10 in your savings account is less liquid.

::现金在你的口袋中当然是现金,但支票或信用卡呢?它们也是钱吗?经济学家不是要说明衡量货币的单一方法,而是要根据流动性提供更广泛的货币定义。流动性是指金融资产能够以多快的速度用于购买货物或服务。例如,现金非常流动。你的10美元账单可以在午餐时间很容易地用来购买汉堡。然而,在你的储蓄账户中,10美元不是那么容易使用的。你必须去银行或自动取款机取回现金购买午餐。因此,你的储蓄账户中的10美元流动性较小。Video: Fiscal and Monetary Policy

::录像:财政和货币政策Measuring Money: Currency, M1, and M2

::货币:货币、M1和M2The Federal Reserve Bank, which is the central bank of the United States, is a bank regulator and is responsible for monetary policy and defines money according to its liquidity. There are two definitions of money: M1 and M2 money supply. M1 money supply includes those monies that are very liquid such as cash, checkable (demand) deposits, and traveler’s checks. M2 money supply is less liquid in nature and includes M1 plus savings and time deposits, certificates of deposits, and money market funds.

::作为美国中央银行的联邦储备银行是一家银行监管机构,负责货币政策,并根据其流动性界定货币。 货币供应有两种定义:M1和M2货币供应。 M1货币供应包括流动性很强的货币,如现金、可核对(需求)存款和旅行支票。 M2货币供应在性质上流动性较小,包括M1加上储蓄和定期存款、存款证明和货币市场基金。M1 money supply includes coins and currency in circulation—the coins and bills that circulate in an economy that are not held by the U.S. Treasury, at the Federal Reserve Bank, or in bank vaults. Closely related to currency are checkable deposits, also known as demand deposits . These are the amounts held in checking accounts. They are called demand deposits or checkable deposits because the banking institution must give the deposit holder his money “on demand” when a check is written or a debit card is used. These items together—currency, and checking accounts in banks—make up the definition of money known as M1, which is measured daily by the Federal Reserve System. Traveler’s checks are a also included in M1, but have decreased in use over the recent past.

::M1货币供应包括流通中的硬币和货币——在非由美国财政部、联邦储备银行或银行保险库持有的经济体中流通的硬币和帐单。 与货币密切相关的是可核实的存款,也称为活期存款。 这些是支票账户中持有的金额。 它们被称为活期存款或可核实存款,因为银行机构在开具支票或使用借记卡时必须“按需”向存款持有人提供其货币。 这些项目——货币和银行中的支票 — — 共同构成称为M1的货币定义,每天由联邦储备系统进行计量。 旅行者支票也包含在M1中,但在最近的过去使用量有所下降。A broader definition of money, M2 includes everything in M1 but also adds other types of deposits. For example, M2 includes savings deposits in banks, which are bank accounts on which you cannot write a check directly, but from which you can easily withdraw the money at an automatic teller machine or bank. Many banks and other financial institutions also offer a chance to invest in money market funds, where the deposits of many individual investors are pooled together and invested in a safe way, such as short-term government bonds. Another ingredient of M2 are the relatively small (that is, less than about $100,000) certificates of deposit (CDs) or time deposits, which are accounts that the depositor has committed to leaving in the bank for a certain period of time, ranging from a few months to a few years, in exchange for a higher interest rate. In short, all these types of M2 are money that you can withdraw and spend, but which require a greater effort to do so than the items in M1. 2 should help in visualizing the relationship between M1 and M2. Note that M1 is included in the M2 calculation.

::货币的定义更为宽泛,M2包括了M1中的所有内容,但也增加了其他类型的存款。例如,M2包括银行储蓄存款,这些存款是银行存款,你不能直接开支票,但可以很容易地在自动出纳机或银行提取资金。许多银行和其他金融机构也提供了投资货币市场基金的机会,许多个人投资者的存款都集中在一起,并以安全的方式投资,例如短期政府债券。M2的另一个成分是相对小(不到100 000美元)的存款(CD)或定期存款,这是存款人承诺离开银行一段时间的账户,从几个月到几年不等,以换取更高的利率。简言之,所有这些M2是你可以提取和支出的货币,但需要做出更大的努力才能这样做,而不是M1中的物品。 2应该有助于直观M1和M2之间的关系。 注意M1在M2计算中包括了M1。- The Relationship Between M1 and M2 Money

M1 and M2 money have several definitions, ranging from narrow to broad. M1 = coins and currency in circulation + checkable (demand) deposit + traveler’s checks. M2 = M1 + savings deposits + money market funds + certificates of deposit + other time deposits.

The Federal Reserve System is responsible for tracking the amounts of M1 and M2 and prepares a weekly release of information about the money supply. To provide an idea of what these amounts sound like, according to the Federal Reserve Bank’s measure of the U.S. money stock, at year-end 2012, M1 in the United States was $2.4 trillion, while M2 was $10.4 trillion. For comparison, the size of the U.S. GDP in 2012 was $16.3 trillion. A breakdown of the portion of each type of money that comprised M1 and M2 in 2012, as provided by the Federal Reserve Bank, is provided in 1.

::美联储系统负责跟踪M1和M2的金额,并准备每周发布有关货币供应的信息。 根据美联储银行对美国货币存量的测量,2012年底,美国M1的金额为2.4万亿美元,而M2为10.4万亿美元。 相比之下,2012年美联储GDP规模为16.3万亿美元。 2012年美联储银行提供的2012年M1和M2构成的每类货币份额的细目为1。Components of M1 in the United States in 2012

::2012年美国M1的构成成分$ billions

::10亿美元Currency

::货币货币货币货币$1,090.0

Traveler’s checks

::旅行支票$3.8

Demand deposits and other checking accounts

::活期存款和其他支票账户$1,351.1

Total M1

::M1共计$2,444.9 (or $2.4 trillion)

::2 444.9(或2.4万亿美元)Components of M2 in the United States in 2012

::2012年美国M2的构成成分$ billions

::10亿美元M1 money supply

::M1货币供应$2,444.9

Savings accounts

::储蓄账户$6,692.0

Time deposits

::定期定期存款$631.0

Individual money market mutual fund balances

::个人货币市场共同基金余额$640.1

Total M2

::M2共计$10,408.7 billion (or $10.4 trillion)

::10 408.7亿美元(10.4万亿美元)M1 and M2 Federal Reserve Statistical Release, Money Stock Measures(Source: Federal Reserve Statistical Release,

The lines separating M1 and M2 can become a little blurry. Sometimes elements of M1 are not treated alike; for example, some businesses will not accept personal checks for large amounts, but will accept traveler’s checks or cash. Changes in banking practices and technology have made the savings accounts in M2 more similar to the checking accounts in M1. For example, some savings accounts will allow depositors to write checks, use automatic teller machines, and pay bills over the Internet, which has made it easier to access savings accounts. As with many other economic terms and statistics, the important point is to know the strengths and limitations of the various definitions of money, not to believe that such definitions are as clear-cut to economists as, say, the definition of nitrogen is to chemists.

::M1和M2之间的分界线可能会变得有点模糊。 有时M1的元素不会被同等对待;例如,有些企业不会接受个人大额支票,而是接受旅行者的支票或现金。 银行做法和技术的变化使得M2的储蓄账户更加类似于M1的支票账户。 比如,一些储蓄账户允许存款者在互联网上写支票、使用自动提款机和支付账单,这使得更容易存取储蓄账户。 与许多其他经济术语和统计数据一样,重要的一点是要了解各种货币定义的长处和局限性,而不是相信这些定义对经济学家来说是清楚的,比如说氮的定义对化学家来说就是清楚的。Where does “plastic money” like debit cards, credit cards, and smart money fit into this picture? A debit card, like a check, is an instruction to the user’s bank to transfer money directly and immediately from your bank account to the seller. It is important to note that in our definition of money, it is checkable deposits that are money, not the paper check or the debit card. Although you can make a purchase with a credit card, it is not considered money but rather a short term loan from the credit card company to you. When you make a purchase with a credit card, the credit card company immediately transfers money from its checking account to the seller, and at the end of the month, the credit card company sends you a bill for what you have charged that month. Until you pay the credit card bill, you have effectively borrowed money from the credit card company. With a smart card, you can store a certain value of money on the card and then use the card to make purchases. Some “smart cards” used for specific purposes, like long-distance phone calls, or making purchases at a campus bookstore and cafeteria, are not really all that smart, because they can only be used for certain purchases or in certain places.

::借记卡、信用卡和智能资金等“固定货币”是否适合这张图片中的“固定货币”?借记卡像支票一样,是给用户银行的指令,直接和立即从你的银行账户向卖方转移资金。必须指出,在我们对货币的定义中,这是可核实的存款,不是支票或借记卡。虽然你可以用信用卡进行购买,但它不是钱,而是信用卡公司对你的短期贷款。当你用信用卡进行购买时,信用卡公司立即将支票账户的钱转给卖方,在月底,信用卡公司就向您支付该月的帐单。在你支付信用卡账单之前,你有效地从信用卡公司借款。有了智能卡,你可以在信用卡上储存一定价值的钱,然后用信用卡进行购买。有些“智能卡”用于特定目的,如长途电话,或者在餐厅和餐厅购买,这些“智能卡”并不全是智能的,因为它们只能用于某些地方或某些地方的采购。In short, credit cards, debit cards, and smart cards are different ways to move money when a purchase is made. But having more credit cards or debit cards does not change the quantity of money in the economy, any more than having more checks printed increases the amount of money in your checking account.

::简言之,信用卡、借记卡和智能卡是购买时转移资金的不同方式。 但拥有更多的信用卡或借记卡并不改变经济中货币的数量,而只是打印更多的支票就可以增加支票账户中的钱。One key message underlying this discussion of M1 and M2 is that money in a modern economy is not just paper bills and coins; instead, money is closely linked to bank accounts. Indeed, the macroeconomic policies concerning money are largely conducted through the banking system. The next section explains how banks function and how a nation’s banking system has the power to create money.

::M1和M2讨论背后的一个关键信息是,现代经济中的货币不仅仅是纸币和硬币;相反,货币与银行账户密切相关。 事实上,有关货币的宏观经济政策在很大程度上是通过银行系统实施的。 下一节解释了银行的运作方式和国家银行系统是如何创造货币的。Money is measured with several definitions: M1 includes currency and money in checking accounts (demand deposits). Traveler’s checks are also a component of M1, but are declining in use. M2 includes all of M1, plus savings deposits, time deposits like certificates of deposit, and money market funds.

::M1包括支票账户中的货币和货币(活期存款 ) , 旅行者支票也是M1的组成部分,但正在减少使用。 M2包括所有M1,外加储蓄存款、定期存款(如存款单)和货币市场基金。The Problem of the Zero Percent Interest Rate Lower Bound

::零0%利率下下限的问题Most economists believe that monetary policy (the manipulation of interest rates and credit conditions by a nation’s central bank) has a powerful influence on a nation’s economy. Monetary policy works when the central bank reduces interest rates and makes credit more available. As a result, business investment and other types of spending increase, causing GDP and employment to grow.

::多数经济学家认为货币政策(一国央行操纵利率和信用条件)对国家经济具有强大的影响力。 当央行降低利率并增加信贷供应时,货币政策就会起作用。 结果,企业投资和其他类型的支出增长导致GDP和就业增长。But what if the interest rates banks pay are close to zero already? They cannot be made negative, can they? That would mean that lenders pay borrowers for the privilege of taking their money. Yet, this was the situation the U.S. Federal Reserve found itself in at the end of the 2008–2009 recession. The federal funds rate, which is the interest rate for banks that the Federal Reserve targets with its monetary policy, was slightly above 5% in 2007. By 2009, it had fallen to 0.16%.

::但是,如果利率银行已经接近零了呢? 利率银行支付利率已经接近零了呢? 它们不能变成负数吗? 这意味着放款人支付借款人拿到钱的特权。 然而,美国联邦储备基金在2008—2009年衰退结束时就陷入了这样的境地。 2007年,联邦储备基金利率(即联邦储备基金货币政策所针对银行的利率)略高于5 % 。 到2009年,该利率下降到0.16 % 。The Federal Reserve’s situation was further complicated because fiscal policy, the other major tool for managing the economy, was constrained by fears that the federal budget deficit and the public debt were already too high. What were the Federal Reserve’s options? How could monetary policy be used to stimulate the economy? The answer, as we will see in this chapter, was to change the rules of the game.

::美联储的情况变得更加复杂,因为财政政策 — — 管理经济的另一个主要工具 — — 受到了担心联邦预算赤字和公共债务已经过高的制约。 美联储的选择是什么? 如何利用货币政策刺激经济? 正如我们在本章中所看到的,答案是改变游戏规则。Money, loans, and banks are all tied together. Money is deposited in bank accounts, which is then loaned to businesses, individuals, and other banks. When the interlocking system of money, loans, and banks works well, economic transactions are made smoothly in goods and labor markets and savers are connected with borrowers. If the money and banking system does not operate smoothly, the economy can either fall into recession or suffer prolonged inflation.

::货币、贷款和银行都是捆绑在一起的。 货币存放在银行账户中,然后借给企业、个人和其他银行。 当货币、贷款和银行的互连系统运转良好时,经济交易在商品和劳动力市场上顺利进行,储蓄者与借款人有联系。 如果货币和银行系统运作不顺利,经济可能陷入衰退或长期通货膨胀。The government of every country has public policies that support the system of money, loans, and banking. But these policies do not always work perfectly. This chapter discusses how monetary policy works and what may prevent it from working perfectly.

::每个国家的政府都有支持货币、贷款和银行体系的公共政策。 但这些政策并不总是完美无缺的。 本章讨论了货币政策如何运作以及哪些因素可以阻止货币政策完美运作。How a Central Bank Executes Monetary Policy

::中央银行如何执行货币政策The most important function of the Federal Reserve is to conduct the nation’s monetary policy. Article I, Section 8 of the U.S. Constitution gives Congress the power “to coin money” and “to regulate the value thereof.” As part of the 1913 legislation that created the Federal Reserve, Congress delegated these powers to the Fed. Monetary policy involves managing interest rates and credit conditions, which influences the level of economic activity, as described in more detail below.

::美联储最重要的职能是实施国家货币政策。 美国《宪法》第8条第1款赋予国会“硬币”和“调节其价值”的权力。 作为1913年建立美联储的立法的一部分,国会将这些权力下放给美联储。 货币政策涉及利率和信用条件的管理,这影响到经济活动水平,详见下文。A central bank has three traditional tools to implement monetary policy in the economy:

::中央银行有三种在经济中执行货币政策的传统工具:Open market operations

::开放市场业务Changing reserve requirements

::变动准备金所需经费Changing the discount rate

::改变贴现率In discussing how these three tools work, it is useful to think of the central bank as a “bank for banks”—that is, each private-sector bank has its own account at the central bank. We will discuss each of these monetary policy tools in the sections below.

::在讨论这三个工具如何发挥作用时,将中央银行视为“银行银行”是有用的,也就是说,每个私营部门银行在中央银行有自己的账户。 我们将在下文各节讨论这些货币政策工具。Open Market Operations

::开放市场业务The most commonly used tool of monetary policy in the U.S. is open market operations . Open market operations take place when the central bank sells or buys U.S. Treasury bonds in order to influence the quantity of bank reserves and the level of interest rates. The specific interest rate targeted in open market operations is the federal funds rate. The name is a bit of a misnomer since the federal funds rate is the interest rate charged by commercial banks making overnight loans to other banks. As such, it is a very short term interest rate, but one that reflects credit conditions in financial markets very well.

::美国最常用的货币政策工具是开放市场业务。 当中央银行出售或购买美国国库债券以影响银行储备数量和利率水平时,公开市场业务就发生。 公开市场业务中的具体利率是联邦基金利率。 其名称有点错误,因为联邦基金利率是商业银行向其他银行提供过夜贷款的利率。 因此,它是一个非常短的利率,但能很好地反映金融市场的信用条件。The Federal Open Market Committee (FOMC) makes the decisions regarding these open market operations. The FOMC is made up of the seven members of the Federal Reserve’s Board of Governors. It also includes five voting members who are drawn, on a rotating basis, from the regional Federal Reserve Banks. The New York district president is a permanent voting member of the FOMC and the other four spots are filled on a rotating, annual basis, from the other 11 districts. The FOMC typically meets every six weeks, but it can meet more frequently if necessary. The FOMC tries to act by consensus; however, the chairman of the Federal Reserve has traditionally played a very powerful role in defining and shaping that consensus. For the Federal Reserve, and for most central banks, open market operations have, over the last few decades, been the most commonly used tool of monetary policy.

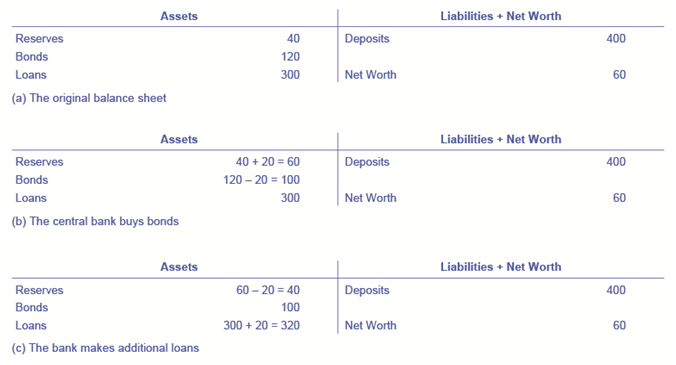

::联邦开放市场委员会(FOMC)负责决定这些公开市场运作。FOMC由联邦储备委员会的七位成员组成。它还包括五名投票成员,轮流从地区联邦储备银行中抽出。 纽约区主席是FOMC的永久投票成员,其他四个点每年轮流从其他11个区填补。 FOMC通常每六个星期开会一次,但必要时可以更频繁地开会。 FOMC试图以协商一致的方式行事;但是,联邦储备委员会主席传统上在确定和形成这一共识方面发挥了非常强大的作用。 对于联邦储备委员会和大多数央行来说,开放市场业务在过去几十年中一直是最常用的货币政策工具。To understand how open market operations affect the money supply, consider the balance sheet of Happy Bank, displayed in 3. 3 (a) shows that Happy Bank starts with $460 million in assets, divided among reserves, bonds and loans, and $400 million in liabilities in the form of deposits, with a net worth of $60 million. When the central bank purchases $20 million in bonds from Happy Bank, the bond holdings of Happy Bank fall by $20 million and the bank’s reserves rise by $20 million, as shown in 3 (b). However, Happy Bank only wants to hold $40 million in reserves (the quantity of reserves that it started with in 3) (a), so the bank decides to loan out the extra $20 million in reserves and its loans rise by $20 million, as shown in 3 (c). The open market operation by the central bank causes Happy Bank to make loans instead of holding its assets in the form of government bonds, which expands the money supply. As the new loans are deposited in banks throughout the economy, these banks will, in turn, loan out some of the deposits they receive, triggering the money multiplier.

::为了了解开放市场业务如何影响货币供应,请考虑《快乐银行》的资产负债表,如第3条第3款(a)项所示,“快乐银行”的资产负债表显示,“快乐银行”从4.6亿美元的资产开始,分为储备金、债券和贷款,以及4亿美元以存款形式负债开始,净值为6 000万美元。 当中央银行从“快乐银行”购买2 000万美元的债券时,“快乐银行”的债券持有量下降2 000万美元,银行的储备增加2 000万美元,如第3款(b)项所示。 然而,“快乐银行”只想要持有4 000万美元的准备金(其开始的准备金数量为3年)(a),因此银行决定从额外的2 000万美元准备金中贷款,其贷款增加2 000万美元,如第3款(c)项所示。 中央银行的“开放市场业务”导致“快乐银行”进行贷款,而不是以政府债券形式持有资产,政府债券扩大了货币供应。 随着新贷款被存入整个经济体的银行,这些银行将反过来借出它们收到的一些存款,触发货币的倍增。Balance Sheet of Happy Bank - Version 1

::幸福银行资产负债表 - 第1版Where did the Federal Reserve get the $20 million that it used to purchase the bonds? A central bank has the power to create money. In practical terms, the Federal Reserve would write a check to Happy Bank, so that Happy Bank can have that money credited to its bank account at the Federal Reserve. In truth, the Federal Reserve created the money to purchase the bonds out of thin air—or with a few clicks on some computer keys.

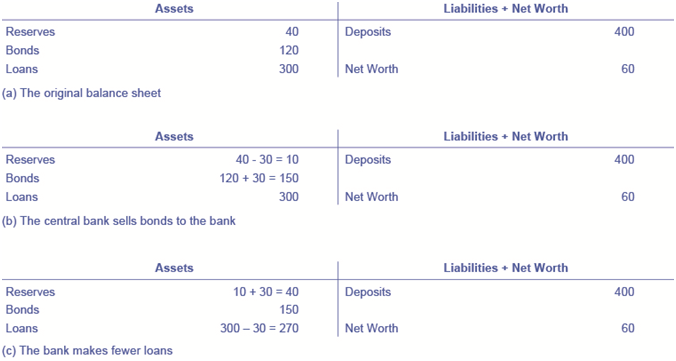

::美联储从哪得到用来购买这些债券的2 000万美元? 央行拥有创造资金的权力。 实际上,美联储会向幸福银行开支票,这样美联储就可以把这笔钱记入其在美联储的银行账户。 事实上,美联储创建了这笔钱,用空机购买这些债券 — — 或者点击电脑钥匙。Open market operations can also reduce the quantity of money and loans in an economy. 3 (a) shows the balance sheet of Happy Bank before the central bank sells bonds in the open market. When Happy Bank purchases $30 million in bonds, Happy Bank sends $30 million of its reserves to the central bank, but now holds an additional $30 million in bonds, as shown in 4 (b). However, Happy Bank wants to hold $40 million in reserves, as in 3 (a), so it will adjust down the quantity of its loans by $30 million, to bring its reserves back to the desired level, as shown in 4 (c). In practical terms, a bank can easily reduce its quantity of loans. At any given time, a bank is receiving payments on loans that it made previously and also making new loans. If the bank just slows down or briefly halts making new loans, and instead adds those funds to its reserves, then its overall quantity of loans will decrease. A decrease in the quantity of loans also means fewer deposits in other banks, and other banks reducing their lending as well, as the money multiplier takes effect. And what about all those bonds? How do they affect the money supply? Read the following for the answer.

::3 (a) 显示幸福银行在中央银行在公开市场出售债券之前的资产负债表。 当快乐银行在公开市场购买3 000万美元的债券时,快乐银行将3 000万美元的储备汇往中央银行,但现在持有额外的3 000万美元的债券,如4(b)所示。 但是,快乐银行希望持有4 000万美元的储备,如在3(a)中那样,这样它就可以将其贷款数量调低3 000万美元,使其储备恢复到4 (c)中所示的预期水平。实际上,银行可以很容易地减少贷款数量。 在任何特定时间内,银行接受其先前提供的贷款,并正在发放新的贷款。如果银行只是放慢或短暂停止发放新贷款,而是将这些资金加入其储备,那么其贷款总额就会减少。贷款数量减少也意味着其他银行的存款减少,其他银行的贷款也减少,货币增值效应也随之减少。所有这些债券会如何影响货币供应?Balance Sheet of Happy Bank - Version 2

::幸福银行资产负债表 -- -- 第2版Does Selling or Buying Bonds Increase the Money Supply?

::出售或购买债券会增加货币供应吗?Is it a sale of bonds by the central bank which increases bank reserves and lowers interest rates or is it a purchase of bonds by the central bank? The easy way to keep track of this is to treat the central bank as being outside the banking system. When a central bank buys bonds, money is flowing from the central bank to individual banks in the economy, increasing the supply of money in circulation. When a central bank sells bonds, then money from individual banks in the economy is flowing into the central bank—reducing the quantity of money in the economy.

::这是中央银行出售的债券,它增加银行储备,降低利率,还是中央银行购买债券? 追踪这一点的简单办法是将中央银行视为银行系统之外。 当中央银行购买债券时,钱就会从中央银行流向经济中的个别银行,从而增加流通资金的供应。 当中央银行出售债券时,经济中的个别银行的钱就会流入中央银行,从而减少经济中的资金数量。Changing Reserve Requirements

::变动准备金需求A second method of conducting monetary policy is for the central bank to raise or lower the reserve requirement , which, as noted earlier, is the percentage of each bank’s deposits that it is legally required to hold either as cash in their vault or on deposit with the central bank. If banks are required to hold a greater amount in reserves, they have less money available to lend out. If banks are allowed to hold a smaller amount in reserves, they will have a greater amount of money available to lend out.

::实施货币政策的第二种方法是央行提高或降低储备要求,如前所述,储备要求是每个银行依法必须持有的存款的百分比,这些存款要么作为现金存放在其保险库中,要么作为存款存入中央银行。 如果要求银行持有更多的储备,那么银行可以借出的资金就更少了。 如果允许银行持有较少的储备,它们将拥有更多的贷款资金。At the end of 2013, the Federal Reserve required banks to hold reserves equal to 0% of the first $13.3 million in deposits, then to hold reserves equal to 3% of the deposits up to $89.0 million in checking and savings accounts, and 10% of any amount above $89.0 million. Small changes in the reserve requirements are made almost every year. For example, the $89.0 million dividing line is sometimes bumped up or down by a few million dollars. In practice, large changes in reserve requirements are rarely used to execute monetary policy. A sudden demand that all banks increase their reserves would be extremely disruptive and difficult to comply with, while loosening requirements too much would create a danger of banks being unable to meet the demand for withdrawals.

::2013年底,美联储要求银行持有相当于头一笔1 330万美元的存款的0 % 的储备,然后持有相当于存款的3%的储备,在支票和储蓄账户中高达8 900万美元,以及超过8 900万美元的任何金额的10%。 准备金需求几乎每年都有小幅变化。 比如,8 900万美元的分界线有时会涨跌几百万美元。 实际上,储备需求的大幅变化很少用于实施货币政策。 突然要求所有银行增加其准备金将极具破坏性且难以遵守,而放松要求则会造成银行无法满足提款需求的风险。Changing the Discount Rate

::更改贴现率The Federal Reserve was founded in the aftermath of the Financial Panic of 1907 when many banks failed as a result of bank runs. As mentioned earlier, since banks make profits by lending out their deposits, no bank, even those that are not bankrupt, can withstand a bank run. As a result of the Panic, the Federal Reserve was founded to be the “lender of last resort.” In the event of a bank run, sound banks, (banks that were not bankrupt) could borrow as much cash as they needed from the Fed’s discount “window” to quell the bank run. The interest rate banks pay for such loans is called the discount rate . (They are so named because loans are made against the bank’s outstanding loans “at a discount” of their face value.) Once depositors became convinced that the bank would be able to honor their withdrawals, they no longer had a reason to make a run on the bank. In short, the Federal Reserve was originally intended to provide credit passively, but in the years since its founding, the Fed has taken on a more active role with monetary policy.

::美联储是在1907年金融恐慌之后成立的,当时许多银行都因银行破产而破产。 如前所述,由于银行通过放贷而获利,因此没有任何银行,甚至那些没有破产的银行,能够承受银行的运行。 由于恐慌,美联储是“最后的贷款人 ” 。 如果银行破产,美联储(没有破产的银行 ) 可以从美联储的贴现“窗口”中借出足够多的现金来压倒银行的运行。 利率银行为这类贷款支付的利率被称为贴现率。 (因为贷款是用银行的未偿贷款“贴现 ” , 银行的面值。 )一旦存款人确信银行能够兑现其提款,他们就没有理由再在银行里逃钱了。 简言之,美联储原本打算被动地提供信贷,但自其成立以来的几年里,美联储在货币政策中扮演了更加积极的作用。So, the third traditional method for conducting monetary policy is to raise or lower the discount rate. If the central bank raises the discount rate, then commercial banks will reduce their borrowing of reserves from the Fed, and instead call in loans to replace those reserves. Since fewer loans are available, the money supply falls and market interest rates rise. If the central bank lowers the discount rate it charges to banks, the process works in reverse.

::因此,实施货币政策的第三个传统方法就是提高或降低贴现率。 如果央行提高贴现率,那么商业银行就会减少向美联储的储备借款,而要求用贷款来取代这些储备。 由于可获得的贷款较少,货币供应下降,市场利率上升。 如果央行降低向银行收取的贴现率,这一过程就会倒转。In recent decades, the Federal Reserve has made relatively few discount loans. Before a bank borrows from the Federal Reserve to fill out its required reserves, the bank is expected to first borrow from other available sources, like other banks. This is encouraged by Fed’s charging a higher discount rate, than the federal funds rate. Given that most banks borrow little at the discount rate, changing the discount rate up or down has little impact on their behavior. More importantly, the Fed has found from experience that open market operations are a more precise and powerful means of executing any desired monetary policy.

::近几十年来,美联储提供了相对较少的贴现贷款。 在一家银行向美联储借款以补足其所需储备之前,预期该银行将首先从其他可用来源(如其他银行 ) 借款。 美联储的贴现率高于联邦基金利率,这令美联储感到鼓舞。 鉴于大多数银行的贴现率很低,改变贴现率或上下调对其行为影响不大。 更重要的是,美联储从经验中发现,开放市场业务是执行任何预期货币政策的更准确和有力手段。In the Federal Reserve Act, the phrase “...to afford means of rediscounting commercial paper” is contained in its long title. This tool was seen as the main tool for monetary policy when the Fed was initially created. This illustrates how monetary policy has evolved and how it continues to do so.

::在《联邦储备法》中,“买得起商业票据再贴现手段”的短语载于其长标题中。 这一工具在美联储最初成立时被视为货币政策的主要工具。 这说明了货币政策是如何演变的,以及它如何继续发展。A central bank has three traditional tools to conduct monetary policy: open market operations, which involves buying and selling government bonds with banks; reserve requirements, which determine what level of reserves a bank is legally required to hold; and discount rates, which is the interest rate charged by the central bank on the loans that it gives to other commercial banks. The most commonly used tool is open market operations.

::央行有三种实施货币政策的传统工具:公开市场业务,涉及与银行买卖政府债券;储备要求,确定银行依法必须持有的储备水平;以及贴现率,即中央银行对其给予其他商业银行的贷款收取的利率。 最常用的工具是开放市场业务。Monetary Policy and Economic Outcomes

::货币政策和经济结果A monetary policy that lowers interest rates and stimulates borrowing is known as an expansionary monetary policy or loose monetary policy. Conversely, a monetary policy that raises interest rates and reduces borrowing in the economy is a contractionary monetary policy or tight monetary policy. This module will discuss how expansionary and contractionary monetary policies affect interest rates and aggregate demand, and how such policies will affect macroeconomic goals like unemployment and inflation. We will conclude with a look at the Fed’s monetary policy practice in recent decades.

::降低利率和刺激借贷的货币政策被称为扩张货币政策或宽松货币政策。 相反,提高利率和减少经济借贷的货币政策是紧缩货币政策或紧缩货币政策。 本模块将讨论扩张和紧缩货币政策如何影响利率和总需求,以及这些政策如何影响失业和通胀等宏观经济目标。 我们最后将审视美联储近几十年来的货币政策实践。The Effect of Monetary Policy on Interest Rates

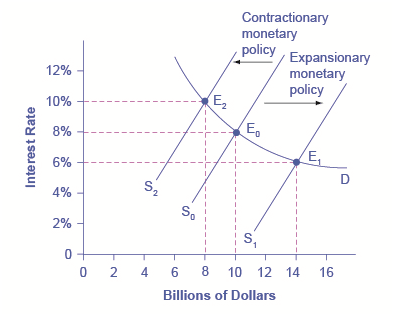

::货币政策对利率的影响Consider the market for loanable bank funds, shown in 5. The original equilibrium (E 0 ) occurs at an interest rate of 8% and a quantity of funds loaned and borrowed of $10 billion. An expansionary monetary policy will shift the supply of loanable funds to the right from the original supply curve (S 0 ) to S 1 , leading to an equilibrium (E 1 ) with a lower interest rate of 6% and a quantity of funds loaned of $14 billion. Conversely, a contractionary monetary policy will shift the supply of loanable funds to the left from the original supply curve (S 0 ) to S 2 , leading to an equilibrium (E 2 ) with a higher interest rate of 10% and a quantity of funds loaned of $8 billion.

::5. 原始平衡(E0)的利率为8%,贷款和借款额为100亿美元。 扩张性货币政策将把贷款资金的供应从原来的供应曲线(S0)向右转移至S1,导致平衡(E1),利率较低为6%,贷款额为140亿美元。 相反,紧缩货币政策将把贷款资金的供应从原来的供应曲线(S0)向左转移至S2,导致10%的较高利率和80亿美元贷款额的平衡(E2)。- Monetary Policy and Interest Rates

The original equilibrium occurs at E 0 . An expansionary monetary policy will shift the supply of loanable funds to the right from the original supply curve (S 0 ) to the new supply curve (S 1 ) and to a new equilibrium of E 1 , reducing the interest rate from 8% to 6%. A contractionary monetary policy will shift the supply of loanable funds to the left from the original supply curve (S 0 ) to the new supply (S 2 ), and raise the interest rate from 8% to 10%.

::最初的平衡发生在E0。 扩张性货币政策将把可贷款资金的供应从原来的供应曲线(S0)转向新的供应曲线(S1)和新的E1平衡,将利率从8%降至6%。 紧缩性货币政策将把可贷款资金的供应从原来的供应曲线(S0)转向新的供应曲线(S2),并将利率从8%提高到10%。So how does a central bank “raise” interest rates? When describing the monetary policy actions taken by a central bank, it is common to hear that the central bank “raised interest rates” or “lowered interest rates.” We need to be clear about this: more precisely, through open market operations the central bank changes bank reserves in a way which affects the supply curve of loanable funds. As a result, interest rates change, as shown in 5. If they do not meet the Fed’s target, the Fed can supply more or less reserves until interest rates do.

::央行如何“提高”利率呢? 在描述央行采取的货币政策行动时,人们通常会听到央行“提高利率”或“降低利率 ” 。 我们需要明确这一点:更准确地说,央行通过公开市场运作改变银行储备,从而影响可贷款资金的供应曲线。 结果,利率变化,如5所示:如果利率达不到美联储的目标,美联储可以提供多少准备金直到利率达到为止。Recall that the specific interest rate the Fed targets is the federal funds rate. The Federal Reserve has, since 1995, established its target federal funds rate in advance of any open market operations.

::回顾美联储目标的具体利率是联邦基金利率,1995年以来,美联储在任何公开市场运作之前就制定了联邦基金利率目标。Of course, financial markets display a wide range of interest rates, representing borrowers with different risk premiums and loans that are to be repaid over different periods of time. In general, when the federal funds rate drops substantially, other interest rates drop, too, and when the federal funds rate rises, other interest rates rise. However, a fall or rise of one percentage point in the federal funds rate—which remember is for borrowing overnight—will typically have an effect of less than one percentage point on a 30-year loan to purchase a house or a three-year loan to purchase a car. Monetary policy can push the entire spectrum of interest rates higher or lower, but the specific interest rates are set by the forces of supply and demand in those specific markets for lending and borrowing.

::当然,金融市场的利率范围很广,代表着不同风险溢价和贷款在不同时期偿还的借款人。 一般来说,当联邦基金利率大幅下降,其他利率也下降,而当联邦基金利率上升,其他利率也上升。 但是,联邦基金利率下降或上升一个百分点 — — 记得是一夜借款 — — 通常对购买房屋或购买汽车三年贷款的30年贷款的影响不到一个百分点。 货币政策可以推高或降低整个利率范围,但具体利率是由这些特定市场的供需力量确定的。The Effect of Monetary Policy on Aggregate Demand

::货币政策对总需求的影响Monetary policy affects interest rates and the available quantity of loanable funds, which in turn affects several components of aggregate demand. Tight or contractionary monetary policy that leads to higher interest rates and a reduced quantity of loanable funds will reduce two components of aggregate demand. Business investment will decline because it is less attractive for firms to borrow money, and even firms that have money will notice that, with higher interest rates, it is relatively more attractive to put those funds in a financial investment than to make an investment in physical capital. In addition, higher interest rates will discourage consumer borrowing for big-ticket items like houses and cars. Conversely, loose or expansionary monetary policy that leads to lower interest rates and a higher quantity of loanable funds will tend to increase business investment and consumer borrowing for big-ticket items.

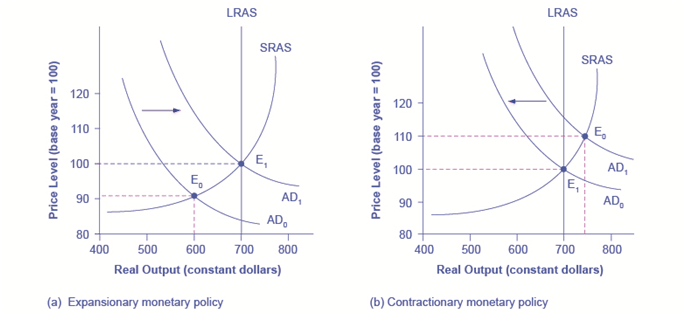

::货币政策会影响利率和可贷款资金的可用数量,而这反过来又会影响总需求的若干组成部分。 紧缩或收缩货币政策(导致利率提高和贷款资金数量减少)将减少总需求的两个组成部分。 商业投资将下降,因为企业借贷的吸引力较低,甚至那些有资金的公司也会注意到,随着利率的提高,将这些资金投入金融投资比投资于实物资本更具吸引力。 此外,更高的利率将阻止消费者为大票项目(如房屋和汽车)借贷。 相反,导致利率降低和贷款金额增加的宽松或扩张性货币政策将倾向于增加大票项目的商业投资和消费借贷。If the economy is suffering a recession and high unemployment, with output below potential GDP, expansionary monetary policy can help the economy return to potential GDP. 6 (a) illustrates this situation. This example uses a short-run upward-sloping Keynesian aggregate supply curve (SRAS). The original equilibrium during a recession of E 0 occurs at an output level of 600. An expansionary monetary policy will reduce interest rates and stimulate investment and consumption spending, causing the original aggregate demand curve (AD 0 ) to shift right to AD 1 , so that the new equilibrium (E 1 ) occurs at the potential GDP level of 700.

::如果经济正在经历衰退和高失业率,产出低于潜在国内生产总值,扩张性货币政策可以帮助经济恢复到潜在的国内生产总值。 6(a) 说明了这种情况。这个例子使用了短期的、向上倾斜的凯恩斯综合供应曲线(SRAS ) 。 E0衰退期间的最初平衡在600个产出水平上。 扩张性货币政策将降低利率,刺激投资和消费支出,导致原始总需求曲线(AD0)向AD1转移,从而新的平衡(E1)在700个潜在GDP水平上出现。Expansionary or Contractionary Monetary Policy

::扩张或收缩货币政策(a) The economy is originally in a recession with the equilibrium output and price level shown at E 0 . Expansionary monetary policy will reduce interest rates and shift aggregate demand to the right from AD 0 to AD 1 , leading to the new equilibrium (E 1 ) at the potential GDP level of output with a relatively small rise in the price level. (b) The economy is originally producing above the potential GDP level of output at the equilibrium E 0 and is experiencing pressures for an inflationary rise in the price level. Contractionary monetary policy will shift aggregate demand to the left from AD 0 to AD 1 , thus leading to a new equilibrium (E 1 ) at the potential GDP level of output.

::扩张性货币政策将降低利率,将总需求从AD0转向右转至AD1,从而在潜在国内生产总值产出水平上实现新的平衡(E1),价格水平上的增长相对较小。 (b) 经济最初的产值高于E0平衡下的潜在国内生产总值产出水平,并正承受着价格水平通胀上升的压力,常规货币政策将把总需求从AD0转向AD1,从而在潜在国内生产总值产出水平上实现新的平衡(E1)。Conversely, if an economy is producing at a quantity of output above its potential GDP, a contractionary monetary policy can reduce the inflationary pressures for a rising price level. In 6 (b), the original equilibrium (E 0 ) occurs at an output of 750, which is above potential GDP. A contractionary monetary policy will raise interest rates, discourage borrowing for investment and consumption spending, and cause the original demand curve (AD 0 ) to shift left to AD 1 , so that the new equilibrium (E 1 ) occurs at the potential GDP level of 700.

::相反,如果一个经济体的产量超过其潜在的GDP,那么紧缩货币政策可以降低通胀压力,导致物价上涨。 在6(b)中,最初的平衡(E0)以750的产值出现,高于潜在的GDP。 紧缩货币政策将提高利率,抑制投资和消费支出的借贷,并导致最初的需求曲线(AD0)向AD1转移,这样新的平衡(E1)就会在700的潜在GDP水平上出现。These examples suggest that monetary policy should be countercyclical; that is, it should act to counterbalance the business cycles of economic downturns and upswings. Monetary policy should be loosened when a recession has caused unemployment to increase and tightened when inflation threatens. Of course, countercyclical policy does pose a danger of overreaction. If loose monetary policy seeking to end a recession goes too far, it may push aggregate demand so far to the right that it triggers inflation. If tight monetary policy seeking to reduce inflation goes too far, it may push aggregate demand so far to the left that a recession begins. 7 (a) summarizes the chain of effects that connect loose and tight monetary policy to changes in output and the price level.

::这些例子表明货币政策应该是反周期的;也就是说,它应该采取行动来抵消经济下滑和上升的商务周期。 当经济衰退导致失业增加并在通货膨胀威胁下收紧时,货币政策应该放松。 当然,反周期政策确实有过度反应的危险。 如果试图结束衰退的宽松货币政策走得太远,它可能会将总需求推向触发通胀的右面。 如果试图降低通胀的紧缩货币政策走得太远,它可能会将总需求推向衰退开始的左面。 7(a)总结了将宽松和紧凑的货币政策与产出和价格水平变化联系起来的一系列影响。The Pathways of Monetary Policy

::货币政策途径(a) In expansionary monetary policy the central bank causes the supply of money and loanable funds to increase, which lowers the interest rate, stimulating additional borrowing for investment and consumption, and shifting aggregate demand right. The result is a higher price level and, at least in the short run, higher real GDP. (b) In contractionary monetary policy, the central bank causes the supply of money and credit in the economy to decrease, which raises the interest rate, discouraging borrowing for investment and consumption, and shifting aggregate demand left. The result is a lower price level and, at least in the short run, lower real GDP.

:a) 在扩张性货币政策中,中央银行导致货币和可贷款资金的供应增加,这降低了利率,刺激了投资和消费方面的额外借款,并改变了总需求权利,结果是价格水平较高,至少在短期内实际国内生产总值较高。 (b) 在紧缩性货币政策中,中央银行导致经济中的货币和信贷供应减少,这提高了利率,抑制了投资和消费方面的借款,并改变了总需求,结果是价格水平较低,至少在短期内实际国内生产总值较低。

Federal Reserve Actions Over Last Four Decades

::联邦储备基金过去四个十年的行动For the period from the mid-1970s up through the end of 2007, Federal Reserve monetary policy can largely be summed up by looking at how it targeted the federal funds interest rate using open market operations.

::从1970年代中期到2007年底,美联储货币政策在很大程度上可以通过研究它如何利用开放市场业务将联邦基金利率作为目标来加以总结。Of course, telling the story of the U.S. economy since 1975 in terms of Federal Reserve actions leaves out many other macroeconomic factors that were influencing unemployment, recession, economic growth, and inflation over this time. The nine episodes of Federal Reserve action outlined in the sections below also demonstrate that the central bank should be considered one of the leading actors influencing the macro economy. As noted earlier, the single person with the greatest power to influence the U.S. economy is probably the chairperson of the Federal Reserve.

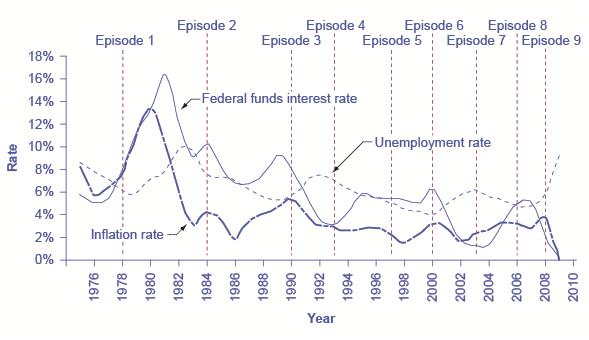

::当然,讲述1975年以来美国经济在美联储行动方面的情况,忽略了这一时期影响失业、衰退、经济增长和通货膨胀的许多其他宏观经济因素。 以下各节概述的美联储9次行动也表明央行应被视为影响宏观经济的主要行为方之一。 如前所述,唯一有权影响美国经济的人很可能是美联储主席。8 shows how the Federal Reserve has carried out monetary policy by targeting the federal funds interest rate in the last few decades. The graph shows the federal funds interest rate (remember, this interest rate is set through open market operations), the unemployment rate, and the inflation rate since 1975. Different episodes of monetary policy during this period are indicated in the figure.

::8个图表显示了美联储在过去几十年中如何以联邦基金利率为目标实施货币政策。 图表显示了联邦基金利率(记得,这一利率是通过开放市场运作确定的 ) 、 失业率和1975年以来的通货膨胀率。 图中显示了在此期间的货币政策的不同情况。Monetary Policy, Unemployment, and Inflation

::货币政策、失业和通货膨胀Through the episodes shown here, the Federal Reserve typically reacted to higher inflation with a contractionary monetary policy and a higher interest rate, and reacted to higher unemployment with an expansionary monetary policy and a lower interest rate.

::美联储通常采取紧缩货币政策和高利率来应对高通胀, 并采取扩张性货币政策和低利率来应对高失业率。Episode 1

::第1集Consider Episode 1 in the late 1970s. The rate of inflation was very high, exceeding 10% in 1979 and 1980, so the Federal Reserve used tight monetary policy to raise interest rates, with the federal funds rate rising from 5.5% in 1977 to 16.4% in 1981. By 1983, inflation was down to 3.2%, but aggregate demand contracted sharply enough that back-to-back recessions occurred in 1980 and in 1981–1982, and the unemployment rate rose from 5.8% in 1979 to 9.7% in 1982.

::20世纪70年代后期第1集考虑。 通货膨胀率非常高,1979年和1980年超过10 % 。 因此,美联储采用紧缩货币政策提高利率,联邦基金利率从1977年的5.5%上升到1981年的16.4 % 。 到1983年,通胀降至3.2%,但总需求大幅缩减,1980年和1981-1982年连续衰退发生,失业率从1979年的5.8 % 上升到1982年的9.7 % 。Episode 2

::第2集In Episode 2, in the early 1980s when the Federal Reserve was persuaded that inflation was declining, the Fed began slashing interest rates to reduce unemployment. The federal funds interest rate fell from 16.4% in 1981 to 6.8% in 1986. By 1986 or so, inflation had fallen to about 2% and the unemployment rate had come down to 7%, and was still falling.

::20世纪80年代初,美联储相信通胀正在下降,当时美联储开始削减利率以降低失业率。 联邦基金利率从1981年的16.4%下降到1986年的6.8%。 到1986年左右,通胀已经下降到约2%,失业率已经下降到7%,并且仍在下降。Episode 3

::第三集 第3集In Episode 3, however, in the late 1980s, inflation appeared to be creeping up again, rising from 2% in 1986 up toward 5% by 1989. In response, the Federal Reserve used contractionary monetary policy to raise the federal funds rates from 6.6% in 1987 to 9.2% in 1989. The tighter monetary policy stopped inflation, which fell from above 5% in 1990 to under 3% in 1992, but it also helped to cause the recession of 1990–1991, and the unemployment rate rose from 5.3% in 1989 to 7.5% by 1992.

::然而,在第三集中,在1980年代末期,通胀似乎再次呈上升趋势,从1986年的2%上升到1989年的5 % 。 对此,美联储采取紧缩货币政策将联邦资金利率从1987年的6.6%提高到1989年的9.2%。 紧缩货币政策阻止了通胀,从1990年的5 % 下降到1992年的3 % , 但也促成了1990-1991年的衰退,失业率从1989年的5.3 % 上升到1992年的7.5 % 。Episode 4

::第四集 第4集In Episode 4, in the early 1990s, when the Federal Reserve was confident that inflation was back under control, it reduced interest rates, with the federal funds interest rate falling from 8.1% in 1990 to 3.5% in 1992. As the economy expanded, the unemployment rate declined from 7.5% in 1992 to less than 5% by 1997.

::在1990年代初期的第四集中,当美联储确信通货膨胀重新受到控制时,它降低了利率,联邦基金的利率从1990年的8.1%下降到1992年的3.5%,随着经济的扩张,失业率从1992年的7.5%下降到1997年的5%以下。Episodes 5 and 6

::第5和第6集In Episodes 5 and 6, the Federal Reserve perceived a risk of inflation and raised the federal funds rate from 3% to 5.8% from 1993 to 1995. Inflation did not rise, and the period of economic growth during the 1990s continued. Then in 1999 and 2000, the Fed was concerned that inflation seemed to be creeping up so it raised the federal funds interest rate from 4.6% in December 1998 to 6.5% in June 2000. By early 2001, inflation was declining again, but a recession occurred in 2001. Between 2000 and 2002, the unemployment rate rose from 4.0% to 5.8%.

::在第五和第六集中,美联储意识到了通货膨胀的风险,并将联邦基金利率从1993年的3%提高到1995年的5.8%,从1993年的3%提高到1995年的5.8%。 通货膨胀没有上升,1990年代的经济增长时期仍在继续。 然后在1999年和2000年,美联储担心通货膨胀似乎在上升,因此将联邦基金的利率从1998年12月的4.6%提高到2000年6月的6.5%。 到2001年初,通货膨胀再次下降,但2001年出现衰退。 2000年和2002年,失业率从4.0%上升到5.8%。Episodes 7 and 8

::第7和第8集In Episodes 7 and 8, the Federal Reserve conducted a loose monetary policy and slashed the federal funds rate from 6.2% in 2000 to just 1.7% in 2002, and then again to 1% in 2003. They actually did this because of fear of Japan-style deflation; this persuaded them to lower the Fed funds further than they otherwise would have. The recession ended, but, unemployment rates were slow to decline in the early 2000s. Finally, in 2004, the unemployment rate declined and the Federal Reserve began to raise the federal funds rate until it reached 5% by 2007.

::在第七和第八集中,美联储采取了宽松的货币政策,削减了联邦基金利率,从2000年的6.2%降至2002年的1.7%,然后又再次降至2003年的1%。 他们之所以这样做,是因为担心日本式的通货紧缩;这说服他们进一步降低美联储基金。 衰退结束了,但失业率在2000年代初缓慢下降。 最后,2004年失业率下降,美联储开始提高联邦基金利率,直到2007年达到5%。Episode 9

::第9集In Episode 9, as the Great Recession took hold in 2008, the Federal Reserve was quick to slash interest rates, taking them down to 2% in 2008 and to nearly 0% in 2009. When the Fed had taken interest rates down to near-zero by December 2008, the economy was still deep in recession. Open market operations could not make the interest rate turn negative. The Federal Reserve had to think “outside the box.”

::在第九集中,随着2008年大衰退的到来,美联储迅速大幅降低利率,2008年将利率降至2%,2009年降至近零 % 。 当美联储在2008年12月将利率降至接近零时,经济仍然处于衰退的深渊。 开放市场运作无法让利率向负转变。 美联储不得不考虑“在箱外 ” 。Quantitative Easing

::量化宽松The most powerful and commonly used of the three traditional tools of monetary policy—open market operations—works by expanding or contracting the money supply in a way that influences the interest rate. In late 2008, as the U.S. economy struggled with recession, the Federal Reserve had already reduced the interest rate to near-zero. With the recession still ongoing, the Fed decided to adopt an innovative and nontraditional policy known as quantitative easing (QE). This is the purchase of long-term government and private mortgage-backed securities by central banks to make credit available so as to stimulate aggregate demand.

::最强大和最常用的货币政策三大传统工具 — — 开放市场业务 — — 通过扩大货币供应或以影响利率的方式签订货币供应合同来开展工作。 2008年底,随着美国经济陷入衰退,美联储已经将利率降至接近零。 随着衰退的持续,美联储决定采取创新和非传统的政策,即量化宽松(QE ) , 即由央行购买长期政府和私人抵押支持的证券,以提供信贷刺激总需求。Quantitative easing differed from traditional monetary policy in several key ways. First, it involved the Fed purchasing long term Treasury bonds, rather than short term Treasury bills. In 2008, however, it was impossible to stimulate the economy any further by lowering short term rates because they were already as low as they could get. (Read the closing Bring it Home feature for more on this.) Therefore, Bernanke sought to lower long-term rates utilizing quantitative easing.

::量化宽松在几个关键方面与传统货币政策不同。 首先,它涉及美联储购买长期国债,而不是短期国债。 但在2008年,不可能通过降低短期利率来进一步刺激经济,因为短期利率已经达到了他们所能达到的低水平。 (在关闭时,Bernanke试图利用量化宽松来降低长期利率。 )因此,伯南克试图利用量化宽松来降低长期利率。This leads to a second way QE is different from traditional monetary policy. Instead of purchasing Treasury securities, the Fed also began purchasing private mortgage-backed securities, something it had never done before. During the financial crisis, which precipitated the recession, mortgage-backed securities were termed “toxic assets,” because when the housing market collapsed, no one knew what these securities were worth, which put the financial institutions which were holding those securities on very shaky ground. By offering to purchase mortgage-backed securities, the Fed was both pushing long term interest rates down and also removing possibly “toxic assets” from the balance sheets of private financial firms, which would strengthen the financial system.

::这导致QE不同于传统货币政策的第二种方式。 美联储没有购买国库证券,而是开始购买私人按揭支持的证券,这是它以前从未做过的事情。 在引发衰退的金融危机期间,按揭支持的证券被称为“有毒资产 ” , 因为当住房市场崩溃时,没有人知道这些证券的价值,这使持有这些证券的金融机构陷入了非常不稳定的境地。 美联储通过提出购买按揭支持的证券,既降低了长期利率,又将可能“有毒资产”从私人金融公司的资产负债表中剔除,这将加强金融体系。Quantitative easing (QE) occurred in three episodes:

::量化宽松(QE)分为三集:-

During QE

1

, which began in November 2008, the Fed purchased $600 billion in mortgage-backed securities from government enterprises Fannie Mae and Freddie Mac.

::在2008年11月开始的QE1期间,美联储从政府企业Fannie Mae和Freddy Mac购买了6 000亿美元的抵押担保证券。 -

In November 2010, the Fed began QE

2

, in which it purchased $600 billion in U.S. Treasury bonds.

::2010年11月,美联储开始QE2, 购买了6000亿美元的美国国库债券。 -

QE

3

, began in September 2012 when the Fed commenced purchasing $40 billion of additional mortgage-backed securities per month. This amount was increased in December 2012 to $85 billion per month. The Fed has stated that, when economic conditions permit, it will begin tapering (or reducing the monthly purchases). This has not yet happened as of early 2014.

::QE3始于2012年9月,当时美联储开始每月购买400亿美元的额外按揭支持证券,2012年12月这一数额增加到每月850亿美元。 美联储表示,一旦经济条件允许,它将开始缩减(或减少每月购买量 ) 。 截至2014年初,这种情况尚未发生。

The quantitative easing policies adopted by the Federal Reserve (and by other central banks around the world) are usually thought of as temporary emergency measures. If these steps are, indeed, to be temporary, then the Federal Reserve will need to stop making these additional loans and sell off the financial securities it has accumulated. The concern is that the process of quantitative easing may prove more difficult to reverse than it was to enact. The evidence suggests that QE 1 was somewhat successful, but that QE 2 and QE 3 have been less so.

::美联储(以及全世界其他央行)采取的量化宽松政策通常被视为临时紧急措施。 如果这些步骤确实是临时性的,那么美联储就需要停止提供这些额外贷款,并出售所积累的金融证券。 担心量化宽松进程可能比颁布时更难以逆转。 证据表明量化宽松略为成功,但量化宽松和量化宽松却不那么成功。An expansionary (or loose) monetary policy raises the quantity of money and credit above what it otherwise would have been and reduces interest rates, boosting aggregate demand, and thus countering recession. A contractionary monetary policy, also called a tight monetary policy, reduces the quantity of money and credit below what it otherwise would have been and raises interest rates, seeking to hold down inflation. During the 2008–2009 recession, central banks around the world also used quantitative easing to expand the supply of credit.

::扩张(或宽松)货币政策提高了货币和信贷数量,使其高于原本的水平,并降低了利率,刺激了总需求,从而遏制了衰退。 紧缩货币政策 — — 也称为紧缩货币政策 — — 将货币和信贷数量降低到原本的水平以下,提高利率以抑制通胀。 2008—2009年衰退期间,世界各地的央行也利用量化宽松来扩大信贷供应。Pitfalls for Monetary Policy

::货币政策的缺陷In the real world, effective monetary policy faces a number of significant hurdles. Monetary policy affects the economy only after a time lag that is typically long and of variable length. Remember, monetary policy involves a chain of events: the central bank must perceive a situation in the economy, hold a meeting, and make a decision to react by tightening or loosening monetary policy. The change in monetary policy must percolate through the banking system, changing the quantity of loans and affecting interest rates. When interest rates change, businesses must change their investment levels and consumers must change their borrowing patterns when purchasing homes or cars. Then it takes time for these changes to filter through the rest of the economy.

::在现实世界中,有效的货币政策面临许多重大障碍。 货币政策只有在时间滞后通常很长且时间长度不一之后才会影响经济。 记住,货币政策涉及一系列事件:央行必须了解经济形势,召开会议,并通过紧缩或放松货币政策做出反应的决定。 货币政策的改变必须渗透到银行系统,改变贷款数量并影响利率。 当利率发生变化时,企业必须改变投资水平,消费者在购买房屋或汽车时必须改变借贷模式。 然后,这些变化需要时间才能渗透到经济的其余部分。As a result of this chain of events, monetary policy has little effect in the immediate future; instead, its primary effects are felt perhaps one to three years in the future. The reality of long and variable time lags does not mean that a central bank should refuse to make decisions. It does mean that central banks should be humble about taking action, because of the risk that their actions can create as much or more economic instability as they resolve.

::由于这一连串事件的结果,货币政策在最近的将来没有什么作用;相反,它的主要影响可能在未来一到三年才会感受到。 长期和可变的滞后现实并不意味着央行应该拒绝决策。 这并不意味着央行应该对采取行动感到谦虚,因为它们的行动可能会造成与其所解决的一样多或更多的经济不稳定。Excess Reserves

::准备金盈余Banks are legally required to hold a minimum level of reserves, but no rule prohibits them from holding additional excess reserves above the legally mandated limit. For example, during a recession banks may be hesitant to lend, because they fear that when the economy is contracting, a high proportion of loan applicants become less likely to repay their loans.

::法律要求银行持有最低水平的储备,但没有任何规则禁止银行持有超过法定上限的额外过剩储备。 比如,在衰退时期,银行可能不愿贷款,因为他们担心经济收缩时,高比例的贷款申请者更不可能偿还贷款。When many banks are choosing to hold excess reserves, expansionary monetary policy may not work well. This may occur because the banks are concerned about a deteriorating economy, while the central bank is trying to expand the money supply. If the banks prefer to hold excess reserves above the legally required level, the central bank cannot force individual banks to make loans. Similarly, sensible businesses and consumers may be reluctant to borrow substantial amounts of money in a recession, because they recognize that firms’ sales and employees’ jobs are more insecure in a recession, and they do not want to face the need to make interest payments. The result is that during an especially deep recession, an expansionary monetary policy may have little effect on either the price level or the real GDP.

::当许多银行选择持有过剩储备时,扩张性货币政策可能效果不妙。 这可能是因为银行担心经济恶化,而央行则试图扩大货币供应。 如果银行倾向于持有超过法定水平的过剩储备,央行就不能强迫个别银行贷款。 同样,明智的企业和消费者可能不愿在衰退中借大笔钱,因为他们认识到企业的销售和雇员工作在衰退中更加不安全,他们不想面对支付利息的需要。 结果,在特别严重的衰退中,扩张性货币政策可能不会对价格水平或实际GDP产生什么影响。Japan experienced this situation in the 1990s and early 2000s. Japan’s economy entered a period of very slow growth, dipping in and out of recession, in the early 1990s. By February 1999, the Bank of Japan had lowered the equivalent of its federal funds rate to 0%. It kept it there most of the time through 2003. Moreover, in the two years from March 2001 to March 2003, the Bank of Japan also expanded the money supply of the country by about 50%—an enormous increase. Even this highly expansionary monetary policy, however, had no substantial effect on stimulating aggregate demand. Japan’s economy continued to experience extremely slow growth into the mid-2000s.

::日本在1990年代和2000年代初经历了这种情况。 日本经济在1990年代初进入了非常缓慢的增长时期,衰退中和衰退中。 1999年2月,日本银行将相当于其联邦资金的利率降至0 % 。 日本银行在2003年的大部分时间里将其保持在了这一水平。 此外,在2001年3月至2003年3月的两年中,日本银行也把日本货币供应量增加了约50,大幅增加了。 但是,即使这种高度扩张的货币政策对刺激总需求也没有实质性影响。 日本经济在2000年代中期继续经历着极为缓慢的增长。Unpredictable Movements of Velocity

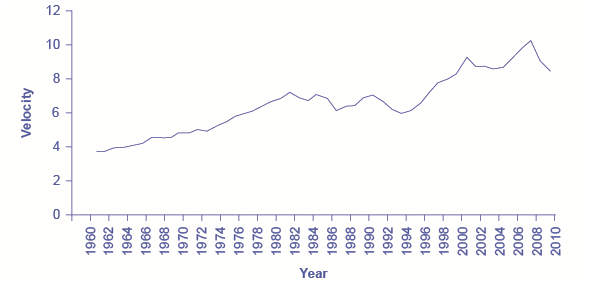

::难以预测的急速移动Velocity is a term that economists use to describe how quickly money circulates through the economy. The velocity of money in a year is defined as:

::速度是经济学家用来描述货币在经济中快速流通的术语。Velocity = nominal GDP

::速率=名义国内生产总值money supply

::货币资金供应Specific measurements of velocity depend on the definition of the money supply being used. Consider the velocity of M1, the total amount of currency in circulation and checking account balances. In 2009, for example, M1 was $1.7 trillion and nominal GDP was $14.3 trillion, so the velocity of M1 was 8.4 ($14.3 trillion/$1.7 trillion). A higher velocity of money means that the average dollar circulates more times in a year; a lower velocity means that the average dollar circulates fewer times in a year.

::具体速度测量取决于货币供应的定义。考虑M1的速度、流通货币和支票账户余额的总量。 比如,2009年M1是1.7万亿美元,名义GDP是14.3万亿美元,因此M1的速度是8.4(14.3万亿美元/1.7万亿美元 ) 。 更高的货币速度意味着平均美元在一年中流通的次数更多;更低的速度意味着平均美元在一年中流通的次数更少。Perhaps you heard the “d” word mentioned during our recent economic downturn. See the following Clear It Up feature for a discussion of how deflation could affect monetary policy.

::或许你听到我们最近经济衰退时提到的“d”字眼了。 在讨论通缩如何影响货币政策时,请看下面的“Clear It Up”特征。What Happens During Episodes of Deflation?

::通缩时发生什么了?Deflation occurs when the rate of inflation is negative; that is, instead of money having less purchasing power over time, as occurs with inflation, money is worth more. Deflation can make it very difficult for monetary policy to address a recession.

::当通货膨胀率为负时就会出现通缩;也就是说,货币不是像通货膨胀那样随着时间推移购买力下降,而是货币的价值更高。 通缩会使货币政策很难应对衰退。Remember that the real interest rate is the nominal interest rate minus the rate of inflation. If the nominal interest rate is 7% and the rate of inflation is 3%, then the borrower is effectively paying a 4% real interest rate. If the nominal interest rate is 7% and there is deflation of 2%, then the real interest rate is actually 9%. In this way, an unexpected deflation raises the real interest payments for borrowers. It can lead to a situation where an unexpectedly high number of loans are not repaid, and banks find that their net worth is decreasing or negative. When banks are suffering losses, they become less able and eager to make new loans. Aggregate demand declines, which can lead to recession.

::记住实际利率是名义利率减去通胀率。 如果名义利率为7 % , 通货膨胀率为3 % , 那么借款人实际上支付实际利率为4 % 。 如果名义利率为7 % , 实际利率为2 % , 那么实际利率实际上为9 % 。 这样,意外通缩提高了借款人的实际利率。 这可能导致出现出乎意料的高额贷款得不到偿还,而银行发现其净值在下降或负值。 当银行遭受损失时,它们就变得不那么有能力和急于提供新贷款。 总体需求下降可能导致衰退。Then the double-whammy: After causing a recession, deflation can make it difficult for monetary policy to work. Say that the central bank uses expansionary monetary policy to reduce the nominal interest rate all the way to zero—but the economy has 5% deflation. As a result, the real interest rate is 5%, and because a central bank cannot make the nominal interest rate negative, an expansionary policy cannot reduce the real interest rate further.

::然后是双重负担:在造成衰退之后,通缩可能使货币政策难以发挥作用。 说央行使用扩张货币政策将名义利率完全降至零 — — 但经济却有5%的通缩。 结果,实际利率为5 % , 由于央行无法使名义利率负值,扩张性政策无法进一步降低实际利率。In the U.S. economy during the early 1930s, deflation was 6.7% per year from 1930–1933, which caused many borrowers to default on their loans and many banks to end up bankrupt, which in turn contributed substantially to the Great Depression. Not all episodes of deflation, however, end in economic depression. Japan, for example, experienced deflation of slightly less than 1% per year from 1999–2002, which hurt the Japanese economy, but it still grew by about 0.9% per year over this period. Indeed, there is at least one historical example of deflation coexisting with rapid growth. The U.S. economy experienced deflation of about 1.1% per year over the quarter-century from 1876–1900, but real GDP also expanded at a rapid clip of 4% per year over this time, despite some occasional severe recessions.

::20世纪30年代初期,美国经济的通缩为每年6.7 % , 从1930—1933年以来,每年6.7 % , 导致许多借款人拖欠贷款,许多银行最终破产,这反过来又导致大萧条。 然而,并非所有通缩事件都以经济萧条告终。 比如,日本从1999—2002年经历了每年略低于1 % 的通缩,这伤害了日本经济,但这一时期它每年仍增长约0.9 % 。 事实上,至少有一个通缩与快速增长共存的历史例子。 美国经济在1876—1900年这一季度经历了每年1.1 % 的通缩,但实际GDP也在这一时期以每年4 % 的快速增长,尽管偶尔出现严重衰退。The central bank should be on guard against deflation and, if necessary, use expansionary monetary policy to prevent any long-lasting or extreme deflation from occurring. Except in severe cases like the Great Depression, deflation does not guarantee economic disaster.

::央行应该警惕通缩,并在必要时使用扩张性货币政策防止任何长期或极端通缩发生。 除大萧条等严重情形外,通缩并不能保证经济灾难。Changes in velocity can cause problems for monetary policy. To understand why, rewrite the definition of velocity so that the money supply is on the left-hand side of the equation. That is:

::速度变化可能会给货币政策带来问题。 为了理解原因,重写速度定义,以使货币供应处于等式的左侧。 也就是说:- Recall that

- Nominal GDP = Price Level (or GDP Deflator) x Real GDP .

- Therefore,

- Money Supply x velocity = Nominal GDP = Price Level x Real GDP .

This equation is sometimes called the basic quantity equation of money but, as you can see, it is just the definition of velocity written in a different form. This equation must hold true, by definition.

::这个方程式有时被称为货币的基本数量方程式,但正如你所看到的,这只是以不同形式书写的速度定义。根据定义,这个方程式必须正确。If velocity is constant over time, then a certain percentage rise in the money supply on the left-hand side of the basic quantity equation of money will inevitably lead to the same percentage rise in nominal GDP—although this change could happen through an increase in inflation, or an increase in real GDP, or some combination of the two. If velocity is changing over time but in a constant and predictable way, then changes in the money supply will continue to have a predictable effect on nominal GDP. If velocity changes unpredictably over time, however, then the effect of changes in the money supply on nominal GDP becomes unpredictable.

::如果速度随时间而变化,那么货币基本数量方程式左侧货币供应量的一定百分比增长将不可避免地导致名义GDP的同样百分比增长 — — 尽管这一变化可能通过通胀上升、实际GDP增长或两者的某种组合而发生。 如果速度随时间而变化,但以恒定和可预测的方式变化,那么货币供应的变化将继续对名义GDP产生可预见的影响。 但是,如果速度变化无法预测,那么货币供应变化对名义GDP的影响将变得无法预测。The actual velocity of money in the U.S. economy as measured by using M1, the most common definition of the money supply, is illustrated in 9. From 1960 up to about 1980, velocity appears fairly predictable; that is, it is increasing at a fairly constant rate. In the early 1980s, however, velocity, as calculated with M1, becomes more variable. The reasons for these sharp changes in velocity remain a puzzle. Economists suspect that the changes in velocity are related to innovations in banking and finance which have changed how money is used in making economic transactions: for example, the growth of electronic payments; a rise in personal borrowing and credit card usage; and accounts that make it easier for people to hold money in savings accounts, where it is counted as M2, right up to the moment that they want to write a check on the money and transfer it to M1. So far at least, it has proven difficult to draw clear links between these kinds of factors and the specific up-and-down fluctuations in M1. Given many changes in banking and the prevalence of electronic banking, M2 is now favored as a measure of money rather than the narrower M1.

::9. 从1960年到1980年左右,以货币供应的最常见定义M1衡量的美国经济中货币的实际速度从货币供应的最常见定义M1中可以看出,9 从1960年到1980年左右,速度似乎相当可以预测;也就是说,速度正在以相当稳定的速度增长;然而,1980年代初,用M1计算的速度变得比较多;速度变化的原因仍然令人费解。经济学家怀疑,速度变化与银行和金融的创新有关,这些创新改变了货币如何用于经济交易:例如,电子付款的增长;个人借款和信用卡使用率的上升;以及使人们更容易在储蓄账户中持有货币的账户,在储蓄账户中计为M2,直到他们想对货币进行检查并将其转入M1时为止。至少,事实证明难以清楚地将这些因素与M1中具体的上下调联系起来。 鉴于银行业的许多变化和电子银行业的普遍程度,M2现在倾向于作为一种货币计量,而不是狭窄的M1。- Velocity Calculated Using M1

Velocity is the nominal GDP divided by the money supply for a given year. Different measures of velocity can be calculated by using different measures of the money supply. Velocity, as calculated by using M1, has lacked a steady trend since the 1980s, instead bouncing up and down. (credit: Federal Reserve Bank of St. Louis)

::速度是特定年份名义GDP除以货币供应量。 使用货币供应量的不同计量方法可以计算出不同的速度。 使用M1计算出的速率自1980年代以来一直缺乏稳定趋势,而是向上和向下跳动。 (信贷:圣路易斯联邦储备银行)In the 1970s, when velocity as measured by M1 seemed predictable, a number of economists, led by Nobel laureate Milton Friedman (1912–2006), argued that the best monetary policy was for the central bank to increase the money supply at a constant growth rate. These economists argued that with the long and variable lags of monetary policy, and the political pressures on central bankers, central bank monetary policies were as likely to have undesirable as to have desirable effects. T his led these economists to believe that the monetary policy should seek steady growth in the money supply of 3% per year. They argued that a steady rate of monetary growth would be correct over longer time periods, since it would roughly match the growth of the real economy. In addition, they argued that giving the central bank less discretion to conduct monetary policy would prevent an overly activist central bank from becoming a source of economic instability and uncertainty. In this spirit, Friedman wrote in 1967: “The first and most important lesson that history teaches about what monetary policy can do—and it is a lesson of the most profound importance—is that monetary policy can prevent money itself from being a major source of economic disturbance.”

::20世纪70年代,当以M1衡量的速度似乎可以预测时,一些经济学家在诺贝尔奖获得者米尔顿·弗里德曼(Milton Friedman (1912 - 2006)的领导下认为,最好的货币政策是央行以恒定的增长率增加货币供应。 这些经济学家认为,随着货币政策的长期和可变的滞后以及央行行长的政治压力,央行货币政策很可能不可取,也会产生理想的效果。 这导致这些经济学家认为货币政策应该寻求每年3%的货币供应稳定增长。 他们认为,稳定的货币增长率在较长的时间内是正确的,因为它大致上可以与实体经济的增长相匹配。 此外,他们认为,给予央行实施货币政策的酌处权会让过度活跃的央行避免成为经济不稳定和不确定性的根源。 本着这一精神,弗里德曼在1967年写道 : “ 历史所揭示的关于货币政策可以做什么的最重要教训 — — 这是最重要的教训 — — 货币政策可以防止货币本身成为经济动荡的主要根源。 ”As the velocity of M1 began to fluctuate in the 1980s, having the money supply grow at a predetermined and unchanging rate seemed less desirable, because as the quantity theory of money shows, the combination of constant growth in the money supply and fluctuating velocity would cause nominal GDP to rise and fall in unpredictable ways. The jumpiness of velocity in the 1980s caused many central banks to focus less on the rate at which the quantity of money in the economy was increasing, and instead to set monetary policy by reacting to whether the economy was experiencing or in danger of higher inflation or unemployment.

::随着M1的速度在1980年代开始波动,货币供应以预先确定和不变的速度增长似乎不太理想,因为货币数量理论表明,货币供应的持续增长和波动速度的结合将导致名义GDP以无法预测的方式上升和下降。 1980年代的速度突飞猛进导致许多央行不那么关注经济中货币数量增长的速度,而是制定货币政策,对经济是否正在经历或面临更高通胀或失业风险作出反应。Unemployment and Inflation

::失业和通货膨胀If you were to survey central bankers around the world and ask them what they believe should be the primary task of monetary policy, the most popular answer by far would be fighting inflation. Most central bankers believe that the neoclassical model of economics accurately represents the economy over the medium to long term. Remember that in the neoclassical model of the economy, the aggregate supply curve is drawn as a vertical line at the level of potential GDP, as shown in 10. In the neoclassical model, the level of potential GDP (and the natural rate of unemployment that exists when the economy is producing at potential GDP) is determined by real economic factors. If the original level of aggregate demand is AD 0 , then an expansionary monetary policy that shifts aggregate demand to AD 1 only creates an inflationary increase in the price level, but it does not alter GDP or unemployment. From this perspective, all that monetary policy can do is to lead to low inflation or high inflation—and low inflation provides a better climate for a healthy and growing economy. After all, low inflation means that businesses making investments can focus on real economic issues, not on figuring out ways to protect themselves from the costs and risks of inflation. In this way, a consistent pattern of low inflation can contribute to long-term growth.

::如果你对全世界的央行行长进行调查,并问他们,他们认为什么应该是货币政策的首要任务,最受欢迎的答案是遏制通货膨胀。大多数央行行长都认为新古典经济学模式准确地代表了中长期经济。记住,在新古典经济模式中,总体供应曲线是按潜在GDP水平纵向线划的,如10所示。 在新古典模式中,潜在的GDP水平(以及当经济以潜在GDP生产时存在的自然失业率)是由实际经济因素决定的。如果最初的总需求水平是AD0,那么将总需求转向AD1的扩张性货币政策只会造成价格水平的通胀性增长,但不会改变GDP或失业。 从这个角度看,货币政策所能做的就是导致低通胀或高通胀水平 — — 低通胀为健康和增长经济提供了更好的气候。 毕竟,低通胀意味着企业可以专注于真正的经济问题,而不是找出保护自己免受通胀成本和风险的方法。 从这个角度看,长期的通胀模式可以导致长期的低通胀。- Monetary Policy in a Neoclassical Model

In a neoclassical view, monetary policy affects only the price level, not the level of output in the economy. For example, an expansionary monetary policy causes aggregate demand to shift from the original AD 0 to AD 1 . However, the adjustment of the economy from the original equilibrium (E 0 ) to the new equilibrium (E 1 ) represents an inflationary increase in the price level from P 0 to P 1 , but has no effect in the long run on output or the unemployment rate. In fact, no shift in AD will affect the equilibrium quantity of output in this model.

::新古典观点认为,货币政策只影响价格水平,而不是经济产出水平。 比如,扩张性货币政策导致总需求从原AD0转向AD1。 然而,经济从原平衡(E0)调整到新平衡(E1)意味着价格水平从P0向P1的通胀性上升,但从长远看对产出或失业率没有影响。 事实上,反倾销的任何变化都不会影响这一模式产出的均衡数量。This vision of focusing monetary policy on a low rate of inflation is so attractive that many countries have rewritten their central banking laws since in the 1990s to have their bank practice inflation targeting, which means that the central bank is legally required to focus primarily on keeping inflation low. By 2010, central banks in 26 countries, including Austria, Brazil, Canada, Israel, Korea, Mexico, New Zealand, Spain, Sweden, Thailand, and the United Kingdom faced a legal requirement to target the inflation rate. A notable exception is the Federal Reserve in the United States, which does not practice inflation-targeting. Instead, the law governing the Federal Reserve requires it to take both unemployment and inflation into account.

::将货币政策集中于低通胀率的愿景是如此具有吸引力,以至于许多国家自1990年代以来就重新制定其中央银行法,使其银行对通货膨胀采取有针对性的做法,这意味着中央银行在法律上必须主要侧重于保持低通胀。 到2010年,包括奥地利、巴西、加拿大、以色列、韩国、墨西哥、新西兰、西班牙、瑞典、泰国和联合王国在内的26个国家的中央银行都面临着以通胀率为目标的法律规定。 一个显著的例外是美国联邦储备银行,它不实行通胀目标。 相反,联邦储备银行的法律要求它同时考虑失业和通胀问题。Economists have no final consensus on whether a central bank should be required to focus only on inflation or should have greater discretion. For those who subscribe to the inflation targeting philosophy, the fear is that politicians who are worried about slow economic growth and unemployment will constantly pressure the central bank to conduct a loose monetary policy—even if the economy is already producing at potential GDP. In some countries, the central bank may lack the political power to resist such pressures, with the result of higher inflation, but no long-term reduction in unemployment. The U.S. Federal Reserve has a tradition of independence, but central banks in other countries may be under greater political pressure. For all of these reasons—long and variable lags, excess reserves, unstable velocity, and controversy over economic goals—monetary policy in the real world is often difficult. The basic message remains, however, that central banks can affect aggregate demand through the conduct of monetary policy and in that way influence macroeconomic outcomes.

::经济学家们对于央行是否应该只关注通货膨胀或者应该拥有更大的自由裁量权没有最终的共识。 对于那些赞同通胀目标哲学的人来说,担心的是那些担心经济增长缓慢和失业的政客会不断迫使央行采取宽松的货币政策 — — 即使经济已经以潜在的GDP为生。 在一些国家,央行可能缺乏抵制这种压力的政治力量,因为通货膨胀升高,但失业率并没有长期下降。 美国联邦储备银行有独立的传统,但其他国家的央行可能面临更大的政治压力。 由于所有这些原因 — — 长期和变数的滞后、过剩的储备、不稳定的速度和对经济目标的争议 — — 现实世界的货币政策往往十分困难。 但是,基本的信息仍然是,央行可以通过货币政策影响总需求,从而影响宏观经济结果。Asset Bubbles and Leverage Cycles

::资产泡沫和杠杆循环One long-standing concern about having the central bank focus on inflation and unemployment is that it may be overlooking certain other economic problems that are coming in the future. For example, from 1994 to 2000 during what was known as the “dot-com” boom, the U.S. stock market, which is measured by the Dow Jones Industrial Index (which includes 30 very large companies from across the U.S. economy), nearly tripled in value. The Nasdaq Index, which includes many smaller technology companies, increased in value by a multiple of five from 1994 to 2000. These rates of increase were clearly not sustainable. Indeed, stock values as measured by the Dow Jones were almost 20% lower in 2009 than they had been in 2000. Stock values in the Nasdaq index were 50% lower in 2009 than they had been in 2000. The drop-off in stock market values contributed to the recession of 2001 and the higher unemployment that followed.

::对中央银行注重通货膨胀和失业的长期关注之一是,它可能忽略了未来出现的某些其他经济问题。 例如,1994-2000年,在所谓的“Dot-com”繁荣期,美国股票市场以道琼斯工业指数(包括来自美国经济的30家大公司)衡量,其价值几乎增加了两倍。 包括许多小型技术公司在内的纳斯达克指数,其价值从1994年至2000年增长了五倍以上,这些增长率显然无法持续。 事实上,道琼斯公司所测得的2009年股票价值比2000年低近20%,2009年纳斯达克指数的股票价值比2000年低50%。 股票市场价值的下跌导致了2001年的衰退和随后的更高失业率。A similar story can be told about housing prices in the mid-2000s. During the 1970s, 1980s, and 1990s, housing prices increased at about 6% per year on average. During what came to be known as the “housing bubble” from 2003 to 2005, housing prices increased at almost double this annual rate. These rates of increase were clearly not sustainable. When the price of housing fell in 2007 and 2008, many banks and households found that their assets were worth less than they expected, which contributed to the recession that started in 2007.

::关于2000年代中期的房价,也可以说类似的故事。 在1970年代、1980年代和1990年代,房价平均每年上涨约6%。 在2003年至2005年所谓的“住房泡沫 ” 期间,房价几乎是年增长率的两倍。 这些上涨率显然是不可持续的。 当2007年和2008年房价下跌时,许多银行和家庭发现他们的资产价值低于预期值,这导致了2007年开始的衰退。At a broader level, some economists worry about a leverage cycle, where “leverage” is a term used by financial economists to mean “borrowing.” When economic times are good, banks and the financial sector are eager to lend, and people and firms are eager to borrow. Remember that the amount of money and credit in an economy is determined by a money multiplier—a process of loans being made, money being deposited, and more loans being made. In good economic times, this surge of lending exaggerates the episode of economic growth. It can even be part of what lead prices of certain assets—like stock prices or housing prices—to rise at unsustainably high annual rates. At some point, when economic times turn bad, banks and the financial sector become much less willing to lend, and credit becomes expensive or unavailable to many potential borrowers. The sharp reduction in credit, perhaps combined with the deflating prices of a dot-com stock price bubble or a housing bubble, makes the economic downturn worse than it would otherwise be.

::在更广的层面上,一些经济学家担心的是杠杆周期,即“杠杆”是金融经济学家用来指“借款”的术语。 当经济时期良好时,银行和金融部门急于贷款,而人们和公司急于借款。 记住,一个经济体的货币和信贷数额是由货币倍增效应决定的 — — 一个贷款、存款和更多贷款的过程。 在良好的经济时期,这种贷款的激增夸大了经济增长的插曲。 这甚至可能是某些资产 — — 如股票价格或住房价格 — — 导致价格以无法维持的高年利率上涨的部分原因。 在某个时候,当经济时期变坏时,银行和金融部门更不愿意贷款,信贷对许多潜在借款人来说变得昂贵或无钱。 信贷的急剧减少,也许与点com股票价格泡沫或住房泡沫的降价相结合,使得经济衰退比其他情况更糟。Thus, some economists have suggested that the central bank should not only just look at economic growth, inflation, and unemployment rates, but should also keep an eye on asset prices and leverage cycles. Such proposals are quite controversial. If a central bank had announced in 1997 that stock prices were rising “too fast” or in 2004 that housing prices were rising “too fast,” and then taken action to hold down price increases, many people and their elected political representatives would have been outraged. Neither the Federal Reserve nor any other central banks want to take the responsibility of deciding when stock prices and housing prices are too high, too low, or just right. As further research explores how asset price bubbles and leverage cycles can affect an economy, central banks may need to think about whether they should conduct monetary policy in a way that would seek to moderate these effects.

::因此,一些经济学家认为央行不仅应该关注经济增长、通胀和失业率,还应该关注资产价格和杠杆周期。 此类建议颇具争议性。 如果央行在1997年宣布股价“过快 ” , 或者在2004年宣布房价“过快 ” , 并随后采取行动压低物价上涨,许多人及其当选政治代表都会感到愤慨。 无论是美联储还是其他央行都不愿承担决定股价和房价何时过高、过低或是否正确的责任。 随着进一步的研究探索资产价格泡沫和杠杆周期如何影响经济,央行可能需要考虑它们是否应该采取货币政策来缓解这些影响。Let’s end this section with how the Fed—or any central bank—would stir up the economy by increasing the money supply.

::让我们以美联储(或任何中央银行)如何通过增加货币供应来刺激经济来结束这一节。Calculating the Effects of Monetary Stimulus

::计算货币刺激的影响Suppose that the central bank wants to stimulate the economy by increasing the money supply. The bankers estimate that the velocity of money is 3, and that the price level will increase from 100 to 110 due to the stimulus. Using the quantity equation of money, what will be the impact of an $800 billion dollar increase in the money supply on the quantity of goods and services in the economy given an initial money supply of $4 trillion?

::假设央行希望通过增加货币供应刺激经济。 银行家估计货币的速度是3,并且由于刺激,价格水平将从100美元上升到110美元。 使用货币数量方程式,货币供应增加8000亿美元对经济中货物和服务数量的影响将是什么,因为最初的货币供应量为4万亿美元?Step 1. We begin by writing the quantity equation of money: MV = PQ. We know that initially V = 3, M = 4,000 (billion) and P = 100. Substituting these numbers in, we can solve for Q:

::1. 我们首先写出货币的数量方程式:MV = PQ。 我们知道最初V = 3, M = 4,000(十亿), P = 100。MV = PQ

::MV = PQ4,000 × 3 = 100 × Q

::4000×3 = 100 × QQ = 120

::Q=120Step 2. Now we want to find the effect of the addition $800 billion in the money supply, together with the increase in the price level. The new equation is:

::步骤2. 现在,我们想找出货币供应增加8 000亿美元以及物价上涨的影响。MV= PQ

::MV = PQ4,800 × 3 = 110 × Q

::4800×3 = 110×QQ = 130.9

::Q=130.9Step 3 . If we take the difference between the two quantities, we find that the monetary stimulus increased the quantity of goods and services in the economy by 10.9 billion.

::步骤3. 如果我们采取这两个数量之间的差额,我们发现货币刺激使经济中的货物和服务数量增加了109亿。The discussion in this chapter has focused on domestic monetary policy; that is, the view of monetary policy within an economy.

::本章的讨论侧重于国内货币政策,即经济体内的货币政策观点。The Problem of the Zero Percent Interest Rate Lower Bound

::零0%利率下下限的问题In 2008, the U.S. Federal Reserve found itself in a difficult position. The federal funds rate was on its way to near zero, which meant that traditional open market operations by which the Fed purchases U.S. Treasury Bills to lower short term interest rates, was no longer viable. This so called “zero bound problem,” prompted the Fed, under then Chair Ben Bernanke, to attempt some unconventional policies, collectively called quantitative easing. By early 2014, quantitative easing nearly quintupled the amount of bank reserves. This likely contributed to the U.S. economy’s recovery, but the impact was muted. This was probably due to some of the hurdles mentioned in the last section of this module. The unprecedented increase in bank reserves also led to fears of inflation. Whether or not the Fed will be able to suck this liquidity out of the system to avoid an inflationary boom as the economy recovers remain to be seen.

::2008年,美联储发现自己处于困难境地。 2008年,美联储发现自己处于困难境地。 联邦基金利率正接近于零,这意味着美联储购买美国短期国库债券以降低短期利率的传统开放市场运作不再可行。 这所谓的“零约束问题 ” 促使美联储(当时的主席本·伯南克)尝试一些非常规政策(统称为量化宽松 ) 。 到2014年初,量化宽松几乎使银行储备量增加了五倍。 这很可能有助于美国经济复苏,但影响却平息了。 这很可能是由于本模块最后一部分提到的一些障碍。 银行储备的空前增长也导致对通胀的担忧。 美联储能否在经济复苏时将这一流动性吸出系统以避免通胀繁荣。Monetary policy is inevitably imprecise, for a number of reasons: (a) the effects occur only after long and variable lags; (b) if banks decide to hold excess reserves, monetary policy cannot force them to lend; and (c) velocity may shift in unpredictable ways. The basic quantity equation of money is MV = PQ, where M is the money supply, V is the velocity of money, P is the price level, and Q is the real output of the economy. Some central banks, like the European Central Bank, practice inflation targeting, which means that the only goal of the central bank is to keep inflation within a low target range. Other central banks, such as the U.S. Federal Reserve, are free to focus on either reducing inflation or stimulating an economy that is in recession, whichever goal seems most important at the time.

::货币政策不可避免地不准确,原因如下Video: Finance Tips: Prime Interest Rate Tips

::视频: 金融提示: 初级利率提示Answer the self check questions below to monitor your understanding of the concepts in this section.

::回答下面的自我核对问题,以监测你对本节概念的理解。Self Check Questions

::自查问题1. What does the monetary policy impact in the short run? In the long run?

::1. 货币政策在短期内会产生什么影响?长期影响?2. How long does it take for the monetary policy to work?

::2. 货币政策运作需要多长时间?3. Define the term "prime rate."

::3. 界定 " 利率 " 一词的定义。4. Research online the current interest rates for: (a) a small business loan, (b) a new car, (c) a used car, (d) a small personal loan, and (e) a mortgage for an existing home.

::4. 在网上研究以下方面的当前利率5. What does it mean to "monetize the debt"? Why would the government do this?

::5. " 将债务货币化 " 意味着什么?6. What should the Federal Reserve do if forced to choose between inflation or high interest rates?

::6. 如果联邦储备局被迫在通货膨胀或高利率之间作出选择,应该怎么办?7. When the Federal Reserve conducts monetary policy, what are two things it cannot control? Explain.

::7. 当美联储执行货币政策时,它无法控制的两件事是什么?8. What is the impact on the economy of an easy money policy?

::8. 简单货币政策对经济有何影响?9. What is the impact on the economy of a tight money policy?

::9. 紧缩货币政策对经济有何影响?10. How do politics influence interest rates?

::10. 政治如何影响利率? -

Changes in the money supply affect the interest rate, the availability of credit, and the price level.