2.6 贸易赤字和汇率

章节大纲

-

Trade Deficits & Exchange Rates

::贸易赤字和汇率Since GDP is measured in a country’s currency, in order to compare different countries’ GDPs, we need to convert them to a common currency. One way to do that is with the exchange rate, which is the price of one country’s currency in terms of another. Once GDPs are expressed in a common currency, we can compare each country’s GDP per capita by dividing GDP by population. Countries with large populations often have large GDPs, but GDP alone can be a misleading indicator of the wealth of a nation. A better measure is GDP per capita.

::由于GDP是以一个国家的货币衡量的,为了比较不同国家的GDP,我们需要把它们转换成一种共同货币。 一种方法就是汇率,即一国货币以另一个货币计算的价格。 一旦GDP以共同货币表示,我们就能用人口来将每个国家的人均GDP除以人口来比较。 人口众多的国家往往拥有大量的GDP,但单是GDP就有可能误导一个国家的财富。 更好的衡量标准是人均GDP。The trade balance measures the gap between a country’s exports and its imports. In most high-income economies, goods make up less than half of a country’s total production, while services compose more than half. The last two decades have seen a surge in international trade in services; however, the most global trade still takes the form of goods rather than services. The current account balance includes the trade in goods, services, and money flowing into and out of a country from investments and unilateral transfers.

::贸易平衡衡量一国出口与进口之间的差距。 在大多数高收入经济体中,商品占国家总产量的不到一半,而服务业则占一半以上。 在过去二十年中,国际服务贸易激增;然而,最全球贸易仍然以商品而不是服务的形式出现。 经常账户平衡包括货物、服务贸易以及投资和单边转移流入和流出一个国家的资金。Universal Generalizations

::普遍化-

A long lasting trade deficit affects the value of a nation's currency.

::长期的贸易赤字影响到一国货币的价值。 -

All countries engage in some kind of trade with other nations.

::所有国家都与其他国家进行某种贸易。

Guiding Questions

::问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问-

How is foreign exchange used in trade?

::外汇如何用于贸易? -

How does a weak American dollar affect you the consumer? A strong dollar?

::疲软的美元对消费者有什么影响?

Comparing GDP among Countries

::国与国之间的国内生产总值比较It is common to use GDP as a measure of economic welfare or standard of living in a nation. When comparing the GDP of different nations for this purpose, two issues immediately arise. First, the GDP of a country is measured in its own currency: the United States uses the U.S. dollar; Canada, the Canadian dollar; most countries of Western Europe, the euro; Japan, the yen; Mexico, the peso; and so on. Since countries use their own currencies , comparing GDP between two countries requires converting to a common currency. A second issue is that countries have very different numbers of people. For instance, the United States has a much larger economy than Mexico or Canada, but it also has roughly three times as many people as Mexico and nine times as many people as Canada. So, if we are trying to compare standards of living across countries, we need to divide GDP by population.

::将国内生产总值作为衡量一国经济福利或生活水平的尺度是常见的。 当为此目的比较不同国家的GDP时,立即出现两个问题。 首先,一个国家的GDP以本国货币衡量:美国使用美元;加拿大使用加拿大美元;西欧大多数国家使用欧元;日本使用日元;墨西哥使用比索等。 由于各国使用自己的货币,将两个国家的GDP进行比较需要转换为共同货币。 第二个问题是,国家的人口数量非常不同。 比如,美国的经济规模比墨西哥或加拿大大得多,但它也有大约三倍的墨西哥人和九倍的加拿大人。 因此,如果我们试图将各国的生活水平作比较,我们需要按人口来区分GDP。Converting Currencies with Exchange Rates

::以汇率转换货币To compare the GDP of countries with different currencies, it is necessary to convert to a “common denominator” using an exchange rate, which is the value of one currency in terms of another currency. Exchange rates are expressed either as the units of country A’s currency that needs to be traded for a single unit of country B’s currency (for example, Japanese yen per British pound), or as the inverse (for example, British pounds per Japanese yen). Two types of exchange rates can be used for this purpose, market exchange rates and purchasing power parity (PPP) equivalent exchange rates. Market exchange rates vary on a day-to-day basis depending on supply and demand in foreign exchange markets. PPP-equivalent exchange rates provide a longer run measure of the exchange rate. For this reason, PPP-equivalent exchange rates are typically used for cross-country comparisons of GDP.

::为了比较使用不同货币的国家的国内生产总值,有必要使用一种汇率(即一种货币以另一种货币计算的价值)转换成一种“共同分母 ” 。 汇率的表示方式要么是A国的货币单位,需要用B国的单一货币单位进行交易(例如,每英磅日元),要么是反之(例如,每日日元英镑 ) 。 为此目的,可以使用两种汇率,即市场汇率和购买力平价等值的汇率。 市场汇率根据外汇市场的供求情况而依日不同而异。 购买力平价等值汇率是衡量汇率的长期尺度。 因此,购买力平价等值汇率通常用于对国内生产总值进行跨国比较。Converting GDP to a Common Currency

::将国内生产总值转换成共同货币Using the exchange rate to convert GDP from one currency to another is straightforward. Say that the task is to compare Brazil’s GDP in 2012 of 4,403 billion reals with the U.S. GDP of $16,245 trillion for the same year.

::使用汇率将GDP从一种货币转换为另一种货币是直截了当的。 这么说,我们的任务是将2012年巴西4,403亿实际GDP与美国当年的16,245万亿美元GDP相比较。Step 1 . Determine the exchange rate for the specified year. In 2012, the exchange rate was 1.869 reals = $1. (These numbers are realistic, but rounded off to simplify the calculations.)

::步骤1. 确定指定年份的汇率:2012年的汇率为1.869实值=1美元。 (这些数字切合实际,但四舍五入,以简化计算。 )Step 2. Convert Brazil’s GDP into U.S. dollars:

::步骤2. 将巴西国内生产总值换算成美元:Brazil's GDP in $ U.S. = Brazil's GDP in reals

::巴西以美元计算的国内生产总值 = 巴西以实值计算的国内生产总值Exchange rate (reals/$ U.S.) = 4,403 billion reals

::汇率(实际/美元)=4 403亿实际1.869 reals per $ U.S. = $2,355.8 billion

::1.869美元/美国1 869美元=23 558亿美元Step 3. Compare this value to the GDP in the United States in the same year. The U.S. GDP was $16,245 in 2012 which is nearly seven times that of GDP in Brazil in 2012.

::步骤3. 与同年美国国内生产总值相比,2012年美国国内生产总值为16 245美元,是2012年巴西国内生产总值的近七倍。Step 4 . View which shows the size of and variety of GDPs of different countries in 2012, all expressed in U.S. dollars. Each is calculated using the process explained above.

::4. 显示2012年不同国家国内生产总值规模和种类的视角,全部以美元表示,每个单位使用上述流程计算。Country

::国家GDP in Billions of Domestic Currency

::国内生产总值(GDP) 10亿国内货币Domestic Currency/U.S. Dollars(PPP Equivalent)

::国内货币/美元(购买力平价等值)GDP (in billions of U.S. dollars)

:单位:10亿美元)

Brazil

::巴西 巴西4,403

reals

::实际数1.869

2,356

Canada

::加拿大 加拿大 加拿大1,818

dollars

::美元1.221

1,488

China

::中国 中国 中国 中国 中国 中国 中国51,932

yuan

::人民币4.186

12,406

Egypt

::埃及 埃及 埃及 埃及 埃及1,542

pounds

::磅2.856

540

Germany

::德国 德国2,644

euros

::欧元0.827

3,197

India

::印度 印度 印度97,514

rupees

::卢比20.817

4,684

Japan

::日本 日本 日本 日本 日本 日本 日本 日本475,868

yen

::日圆102.826

4,628

Mexico

::墨西哥 墨西哥 墨西哥 墨西哥 墨西哥15,502

pesos

::比索8.813

1,759

South Korea

::南韩1,302,128

won

::韩 元数806.81

1,614

United Kingdom

::联合王国 联合王国 联合王国 联合王国 联合王国1,539

pounds

::磅0.659

2,336

United States

::美国 美国 美国 美国16,245

dollars

::美元1.000

16,245

Comparing GDPs Across Countries, 2012(Source: )

GDP Per Capita

::人均国内生产总值The U.S. economy has the largest GDP in the world, by a considerable amount. The United States is also a populous country; in fact, it is the third largest country by population in the world, although well behind China and India. So is the U.S. economy larger than other countries just because the United States has more people than most other countries, or because the U.S. economy is actually larger on a per-person basis? This question can be answered by calculating a country’s GDP per capita; that is, the GDP divided by the population.

::美国经济拥有世界上最大的GDP,其数量相当可观。 美国也是一个人口众多的国家;事实上,它是世界上人口第三大的国家,尽管远远落后于中国和印度。 美国经济也比其他国家大,仅仅因为美国比大多数其他国家人口多,或者因为美国经济实际人均规模较大? 这个问题可以通过计算一个国家的人均GDP来解答,也就是说,GDP除以人口。GDP per capita = GDP/population

::人均国内总产值=国内总产值/人口The second column of lists the GDP of the same selection of countries that appeared in the previous and , showing their GDP as converted into U.S. dollars (which is the same as the last column of the previous table). The third column gives the population for each country. The fourth column lists the GDP per capita. GDP per capita is obtained in two steps: First, by dividing column two (GDP, in billions of dollars) by 1000 so it has the same units as column three (Population, in millions). Then dividing the result (GDP in millions of dollars) by column three (Population, in millions).

::第二栏列出上列所列相同选定国家的国内总产值,并显示其国内总产值换算成美元(与上表最后一栏相同)第三栏列出每个国家的人口。第四栏列出人均国内总产值。人均国内总产值分两步获得:第一,将第二栏(国内总产值,以10亿美元计)除以1 000,因此其单位与第三栏(人口,以百万计)相同。然后将结果(国内总产值,以百万美元计)除以第三栏(人口,以百万计)。Country

::国家GDP (in billions of U.S. dollars)

:Population (in millions)

::人口(百万)Per Capita GDP (in U.S. dollars)

::人均国内生产总值(单位:美元)Brazil

::巴西 巴西2,356

198.36

11,875

Canada

::加拿大 加拿大 加拿大1,488

34.83

42,734

China

::中国 中国 中国 中国 中国 中国 中国12,406

1354.04

9,162

Egypt

::埃及 埃及 埃及 埃及 埃及540

82.50

6,545

Germany

::德国 德国3,197

81.90

39,028

India

::印度 印度 印度4,684

1223.17

3,830

Japan

::日本 日本 日本 日本 日本 日本 日本 日本4,628

127.61

36,266

Mexico

::墨西哥 墨西哥 墨西哥 墨西哥 墨西哥1,614

50.01

32,272

South Korea

::南韩1,759

114.87

15,312

United Kingdom

::联合王国 联合王国 联合王国 联合王国 联合王国2,336

63.24

36,941

United States

::美国 美国 美国 美国16,245

314.18

51,706

GDP Per Capita, 2012 (Source: )

::2012年人均国内总产值(资料来源: )Notice that the ranking by GDP is different from the ranking by GDP per capita. India has a somewhat larger GDP than Germany, but on a per capita basis, Germany has more than 10 times India’s standard of living. Will China soon have a better standard of living than the U.S.? Read the following Clear It Up feature to find out.

::注意GDP的排名与人均GDP的排名不同。 印度的GDP比德国大一些,但按人均计算,德国的生活水平是印度的10倍以上。 中国的生活水平是否会很快比美国更好? 阅读下面的 Clear It Up 特征以了解。Since GDP is measured in a country’s currency, in order to compare different countries’ GDPs, we need to convert them to a common currency. One way to do that is with the exchange rate, which is the price of one country’s currency in terms of another. Once GDPs are expressed in a common currency, we can compare each country’s GDP per capita by dividing GDP by population. Countries with large populations often have large GDPs, but GDP alone can be a misleading indicator of the wealth of a nation. A better measure is GDP per capita.

::由于GDP是以一个国家的货币衡量的,为了比较不同国家的GDP,我们需要把它们转换成一种共同货币。 一种方法就是汇率,即一国货币以另一个货币计算的价格。 一旦GDP以共同货币表示,我们就能用人口来将每个国家的人均GDP除以人口来比较。 人口众多的国家往往拥有大量的GDP,但单是GDP就有可能误导一个国家的财富。 更好的衡量标准是人均GDP。International Trade and Capital Flows

::国际贸易和资本流动A World of Money

::货币世界

More than Meets the Eye in the Congo

::比在刚果遇到的眼还多How much do you interact with the global financial system? If you think that you personally don't interact much with the global financial system, t hink again. Suppose you take out a student loan, or you deposit money into your bank account. You just affected domestic savings and borrowing. Now say you are at the mall and buy two T-shirts “made in China,” and later contribute to a charity that helps refugees. What is the impact? You affected how much money flows into and out of the United States. If you open an IRA savings account and put money in an international mutual fund, you are involved in the flow of money overseas. While your involvement may not seem as influential as someone like the president, who can increase or decrease foreign aid and, thereby, have a huge impact on money flows in and out of the country, you do interact with the global financial system on a daily basis.

::如何与全球金融体系互动?如果你认为自己与全球金融体系没有多少互动,你再想一想。如果你拿学生贷款,或把钱存入银行帐户。你只是影响了国内储蓄和借款。现在说你在商场,购买了两件“在中国制造的”T恤衫,后来又为帮助难民的慈善机构捐款。有什么影响?你影响了进出美国的资金流量。如果你开了一个IRA储蓄账户,并将资金放入国际共同基金,你就会参与海外资金流动。虽然你的参与似乎不像总统这样的人有影响力,他可以增加或减少外援,从而对进出中国的货币流动产生巨大影响,但你却每天与全球金融体系互动。The balance of payments—a term you will meet soon—seems like a huge topic, but once you learn the specific components of trade and money, it all makes sense. Along the way, you may have to give up some common misunderstandings about trade and answer some questions: If a country is running a trade deficit, is that bad? Is a trade surplus good? For example, look at the Democratic Republic of Congo (often referred to as “Congo”), a large country in Central Africa. In 2012, it ran a trade surplus of $688 million, so it must be doing well, right? In contrast, the trade deficit in the United States was $540 billion in 2012. Do these figures suggest that the economy in the United States is doing worse than the Congolese economy? Not necessarily. The U.S. trade deficit tends to worsen as the economy strengthens. In contrast, high poverty rates in the Congo persist, and these rates are not going down even with the positive trade balance. Clearly, it is more complicated than simply asserting that running a trade deficit is bad for the economy.

::国际收支 — — 你很快会遇到 — — 看上去就像一个巨大的话题,但一旦你了解贸易和货币的具体组成部分,这一切都是有道理的。 顺便提一下,你可能不得不放弃对贸易的一些常见误解,并回答一些问题:如果一个国家存在贸易赤字,那么情况是坏的吗?贸易盈余是否很好?例如,看看刚果民主共和国(通常被称为“刚果 ” ) , 中非的一个大国。 2012年,它的贸易盈余为6.88亿美元,因此它必须做得好。 相反,美国的贸易赤字在2012年是5400亿美元。 这些数字是否表明美国经济比刚果经济要差? 不一定。 相比之下,随着经济的加强,美国的贸易赤字往往会恶化。 相反,刚果的高贫困率(通常被称为“刚果 ” ) , 即使贸易顺差也不会下降。 显然,比简单地说出现贸易赤字对经济不利要复杂得多。In 2012, it ran a trade surplus of $688 million, so it must be doing well, right? In contrast, the trade deficit in the United States was $540 billion in 2012. Do these figures suggest that the economy in the United States is doing worse than the Congolese economy? Not necessarily. The U.S. trade deficit tends to worsen as the economy strengthens. In contrast, high poverty rates in the Congo persist, and these rates are not going down even with the positive trade balance. Clearly, it is more complicated than simply asserting that running a trade deficit is bad for the economy.

::2012年,它的贸易盈余为6.88亿美元,因此它必须做得好。 相反,美国2012年的贸易赤字为5400亿美元。 这些数字是否表明美国经济比刚果经济还差? 不一定。 随着经济的加强,美国的贸易赤字往往会恶化。 相反,刚果的高贫困率持续存在,即使贸易平衡呈正增长趋势,这些比率也不会下降。 显然,比简单地宣称贸易赤字对经济不利要复杂得多。The balance of trade (or trade balance) is any gap between a nation’s dollar value of its exports, or what its producers sell abroad, and a nation’s dollar worth of imports, or the foreign-made products and services that households and businesses purchase. If exports exceed imports, the economy is said to have a trade surplus. If imports exceed exports, the economy is said to have a trade deficit. If exports and imports are equal, then trade is balanced. But what happens when trade is out of balance and large trade surpluses or deficits exist?

::贸易平衡(或贸易平衡)是指一国出口品的美元价值、其生产者在国外销售的商品、一国进口品的美元价值、或家庭和企业购买的外国产品和服务之间的任何差额。 如果出口超过进口,那么经济据说就有贸易顺差。 如果进口超过出口,那么经济就会有贸易逆差。 如果进出口是平等的,那么贸易就会是平衡的。 但是,当贸易失衡、贸易顺差或赤字巨大时会怎样呢?Germany, for example, has had substantial trade surpluses in recent decades, in which exports have greatly exceeded imports. According to the Central Intelligence Agency’s The World Factbook , in 2012, Germany ran a trade surplus of $240 billion. In contrast, the U.S. economy in recent decades has experienced large trade deficits, in which imports have considerably exceeded exports. In 2012, for example, U.S. imports exceeded exports by $540 billion.

::比如,近几十年来,德国的贸易顺差很大,出口大大超过进口。 根据中央情报局的《世界概况介绍 》 ( The World Factbook),2012年,德国的贸易顺差为2400亿美元。 相反,近几十年来,美国经济经历了巨大的贸易逆差,进口大大超过出口。 比如,2012年,美国进口超过出口5400亿美元。A series of financial crises triggered by unbalanced trade can lead economies into deep recessions. These crises begin with large trade deficits. At some point, foreign investors become pessimistic about the economy and move their money to other countries. The economy then drops into deep recession, with real GDP often falling up to 10% or more in a single year. This happened to Mexico in 1995 when their GDP fell 8.1%. A number of countries in East Asia—Thailand, South Korea, Malaysia, and Indonesia—came down with the same economic illness in 1997–1998 (called the Asian Financial Crisis). In the late 1990s and into the early 2000s, Russia and Argentina had the identical experience. What are the connections between imbalances of trade in goods and services and the flows of international financial capital that set off these economic avalanches?

::由不平衡贸易引发的一系列金融危机可能导致经济体陷入深度衰退。 这些危机始于巨大的贸易赤字。 在某一时刻,外国投资者对经济持悲观态度,然后将其资金转移到其他国家。 随后,经济陷入深度衰退,实际GDP在一年之内往往跌至10 % 。 1995年墨西哥发生这种情况,当时其GDP下降了8.1 % 。 1997-1998年,东亚一些国家 — — 泰国、韩国、马来西亚和印度尼西亚 — — 都患有同样的经济疾病(称为亚洲金融危机 ) 。 在1990年代末和2000年代初,俄罗斯和阿根廷有着相同的经验。 商品和服务贸易不平衡与导致这些经济雪崩的国际金融资本流动之间有什么联系?We will start by examining the balance of trade in more detail, by looking at some patterns of trade balances in the United States and around the world. Then we will examine the intimate connection between international flows of goods and services and international flows of financial capital, which to economists are really just two sides of the same coin. It is often assumed that trade surpluses like those in Germany must be a positive sign for an economy, while trade deficits like those in the United States must be harmful. As it turns out, both trade surpluses and deficits can be either good or bad.

::首先,我们将更详细地研究贸易平衡,研究美国和全世界贸易平衡的某些模式。 然后,我们将研究国际货物和服务流动与国际金融资本流动之间的密切关系,这对经济学家来说其实只是同一枚硬币的两面。 人们常常认为,像德国这样的贸易顺差必须是一个经济的积极迹象,而像美国这样的贸易逆差必须是有害的。 事实证明,贸易顺差和逆差可以是好的,也可以是坏的。Measuring Trade Balances

::衡量贸易平衡A few decades ago, it was common to track the solid or physical items that were transported by planes, trains, and trucks between countries as a way of measuring the balance of trade. This measurement is called the merchandise trade balance. In most high-income economies, including the United States, goods make up less than half of a country’s total production, while services compose more than half. The last two decades have seen a surge in international trade in services, powered by technological advances in telecommunications and computers that have made it possible to export or import customer services, finance, law, advertising, management consulting, software, construction engineering, and product design. Most global trade still takes the form of goods rather than services, and the merchandise trade balance is still announced by the government and reported prominently in the newspapers. Old habits are hard to break. Economists, however, typically rely on broader measures such as the balance of trade or the current account balance which includes other international flows of income and foreign aid.

::几十年前,追踪由飞机、火车和卡车在国家间运输的固体或实物物品,以此作为衡量贸易平衡的一种方法,这是常见的。 这一衡量方法被称为商品贸易平衡。 在大多数高收入经济体,包括美国,商品占国家总产量的不到一半,而服务业占一半以上。 过去20年,国际服务贸易激增,由电信和计算机技术进步推动,使进出口客户服务、金融、法律、广告、管理咨询、软件、建筑工程和产品设计成为可能。 大多数全球贸易仍然以货物而不是服务的形式出现,商品贸易平衡仍然由政府宣布并在报纸上显著报告。 旧习惯很难打破。 然而,经济学家通常依赖更广泛的措施,比如贸易平衡或包括其他国际收入和外援流动在内的经常账户平衡。Components of the U.S. Current Account Balance

::美国经常账户余额的组成部分3 breaks down the four main components of the U.S. current account balance for 2013. The first line shows the merchandise trade balance; that is, exports and imports of goods. Because imports exceed exports, the trade balance in the final column is negative, showing a merchandise trade deficit.

::2013年美国经常账户余额的四大部分分为3个部分:2013年美国经常账户余额的4个主要部分:第一行显示商品贸易余额,即货物的进出口。 由于进口超过出口,最后一栏的贸易余额为负数,显示商品贸易赤字。Components of the U.S. Current Account Balance for 2013 (in billions)

::2013年美国经常账户余额的组成部分(10亿美元)Value of Exports

::出口价值Value of Imports

::进口价值Balance

::余额余额余额余额余额Goods

::货物货物货物$391.0

$570.1

–$179.1

Services

::服务服务服务处$168.0

$112.6

$55.4

Income payments

::收入收入付款$191.3

$137.4

$53.9

Unilateral transfers

::单方面转让-

$34.5

–$34.5

Current account balance

::经常账户结余$750.3

$854.6

–$104.3

How does the U.S. government collect trade statistics?

::美国政府如何收集贸易统计数据?Do not confuse the balance of trade (which tracks imports and exports), with the current account balance, which includes not just exports and imports, but also income from investment and transfers.

::贸易平衡(追踪进出口)不应与经常账户平衡混淆,经常账户平衡不仅包括进出口,还包括投资和转移收入。Statistics on the balance of trade are compiled by the Bureau of Economic Analysis (BEA) within the U.S. Department of Commerce, using a variety of different sources. Importers and exporters of merchandise must file monthly documents with the Census Bureau, which provides the basic data for tracking trade. To measure international trade in services—which can happen over a telephone line or computer network without any physical goods being shipped—the BEA carries out a set of surveys. Another set of BEA surveys track investment flows, and there are even specific surveys to collect travel information from U.S. residents visiting Canada and Mexico. For measuring unilateral transfers, the BEA has access to official U.S. government spending on aid, and then also carries out a survey of charitable organizations that make foreign donations.

::美国商务部经济分析局(BEA)利用各种不同来源汇编了贸易平衡统计数据,商品进出口商必须每月向人口普查局提交文件,普查局为跟踪贸易提供基本数据,为了衡量国际服务贸易——可以通过电话线或计算机网络进行,而不运送任何有形货物——BEA进行一系列调查,另一套BEA调查跟踪投资流动情况,甚至还进行具体调查,从访问加拿大和墨西哥的美国居民那里收集旅行信息,为了衡量单方面转移,BEA获得美国政府官方的援助支出,然后对提供外国捐助的慈善组织进行调查。This information on international flows of goods and capital is then cross-checked against other available data. For example, the Census Bureau also collects data from the shipping industry, which can be used to check the data on trade in goods. All companies involved in international flows of capital—including banks and companies making financial investments like stocks—must file reports, which are ultimately compiled by the U.S. Department of the Treasury. Information on foreign trade can also be cross-checked by looking at data collected by other countries on their foreign trade with the United States, and also at the data collected by various international organizations. Take these data sources, stir carefully, and you have the U.S. balance of trade statistics. Much of the statistics cited in this chapter come from these sources.

::有关国际货物和资本流动的这一信息随后与其他现有数据进行交叉核对,例如,人口普查局还收集航运业的数据,这些数据可用于核对货物贸易数据,所有参与国际资本流动的公司——包括银行和像股票一样进行金融投资的公司——都必须提交最终由美国财政部汇编的报告,关于外贸的信息也可以通过查看其他国家收集的关于它们与美国对外贸易的数据以及各国际组织收集的数据加以交叉核对,仔细利用这些数据来源,仔细地搅动,并掌握美国贸易统计平衡,本章引用的大部分统计数据来自这些来源。The second row of 3 provides data on trade in services. Here, the U.S. economy is running a surplus. Although the level of trade in services is still relatively small compared to trade in goods, the importance of services has expanded substantially over the last few decades. For example, U.S. exports of services were equal to about one-half of U.S. exports of goods in 2013, compared to one-fifth in 1980.

::第二行3提供了服务贸易数据。这里,美国经济正在出现顺差。 虽然服务贸易水平与货物贸易相比仍然相对较低,但服务业的重要性在过去几十年中大幅提高。 比如,美国2013年的服务出口相当于美国货物出口的一半左右,而1980年是五分之一。The third component of the current account balance, labeled “income payments,” refers to money received by U.S. financial investors on their foreign investments (money flowing into the United States) and payments to foreign investors who had invested their funds here (money flowing out of the United States). The reason for including this money on foreign investment in the overall measure of trade, along with goods and services, is that, from an economic perspective, income is just as much an economic transaction as shipments of cars or wheat or oil: it is just trade that is happening in the financial capital market.

::经常账户余额的第三部分被贴上“收入支付 ” 的标签,指的是美国金融投资者从外国投资(流入美国的资金)和向投资到国外的外国投资者(流出美国的资金)的付款(流出美国的资金 ) 。 将这笔外国投资资金纳入贸易总体计量以及商品和服务的原因在于,从经济角度看,收入与汽车或小麦或石油运输一样是经济交易:金融资本市场正在发生的只是贸易。The final category of the current account balance is unilateral transfers, which are payments made by government, private charities, or individuals in which money is sent abroad without any direct good or service being received. Economic or military assistance from the U.S. government to other countries fits into this category, as does spending abroad by charities to address poverty or social inequalities. When an individual in the United States sends money overseas, it is also counted in this category. The current account balance treats these unilateral payments like imports, because they also involve a stream of payments leaving the country. For the U.S. economy, unilateral transfers are almost always negative. This pattern, however, does not always hold. In 1991, for example, when the United States led an international coalition against Saddam Hussein’s Iraq in the Gulf War, many other nations agreed that they would make payments to the United States to offset the U.S. war expenses. These payments were large enough that, in 1991, the overall U.S. balance on unilateral transfers was a positive $10 billion.

::经常账户余额的最后一类是单方面转移,即由政府、私人慈善机构或个人支付款项,将资金直接汇往国外而没有任何直接好处或得到服务。美国政府向其他国家提供的经济或军事援助也属于这一类别,慈善机构在国外的支出也是如此,用于解决贫困或社会不平等问题。当美国境内的个人向海外汇款时,也计入这一类别。经常账户余额将这些单方面支付款与进口款一样对待,因为它们也涉及离开美国的一系列付款。对于美国经济来说,单方面转移款几乎总是负面的。然而,这种模式并不总能维持下去。 例如,1991年,当美国在海湾战争中率领国际联盟反对萨达姆·侯赛因的伊拉克时,其他许多国家都同意向美国支付款项,以抵消美国战争费用。这些付款数额足够大,1991年,美国单方面转移款的总余额为100亿美元。The trade balance measures the gap between a country’s exports and its imports. In most high-income economies, goods make up less than half of a country’s total production, while services compose more than half. The last two decades have seen a surge in international trade in services; however, most global trade still takes the form of goods rather than services. The current account balance includes the trade in goods, services, and money flowing into and out of a country from investments and unilateral transfers.

::贸易平衡衡量一国出口与进口之间的差距。 在大多数高收入经济体中,商品占国家总产量的不到一半,而服务业则占一半以上。 在过去二十年中,国际服务贸易激增;然而,大多数全球贸易仍然以商品而不是服务的形式出现。 经常账户平衡包括货物、服务贸易以及投资和单边转移流入和流出一个国家的资金。Trade Balances in Historical and International Context

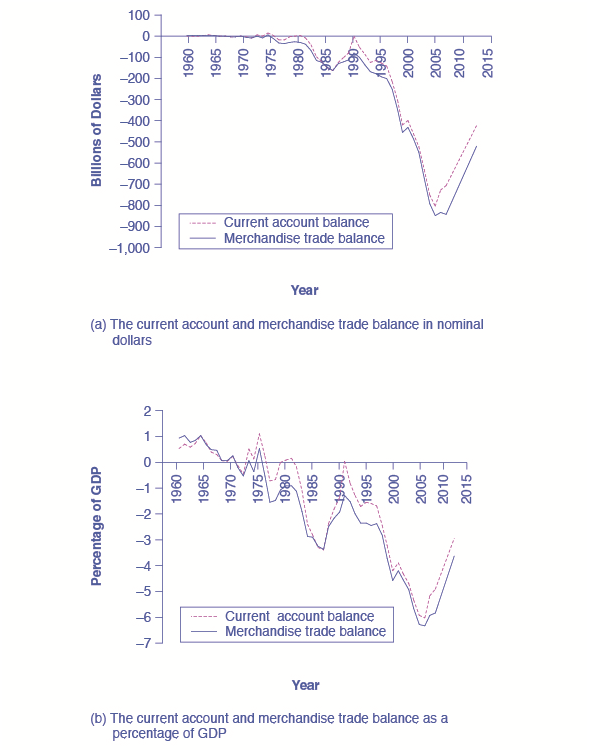

::历史和国际背景下的贸易平衡The history of the U.S. current account balance in recent decades is presented in several different ways. 1 (a) shows the current account balance and the merchandise trade balance in dollar terms. 1 (b) shows the current account balance and merchandise account balance yet again, this time presented as a share of the GDP for that year. By dividing the trade deficit in each year by GDP in that year, 1 (b) factors out both inflation and growth in the real economy.

::美国近几十年来的经常账户余额历史以不同方式呈现。 1(a) 以美元表示经常账户余额和商品贸易余额。 1(b) 以美元表示经常账户余额和商品账户余额,这次以当年国内生产总值的比例表示。 通过将当年每年的贸易赤字除以GDP,1(b) 将实体经济的通胀和增长都推向了现实经济。Current Account Balance and Merchandise Trade Balance, 1960–2012

::1960-2012年经常账户收支平衡和商品贸易平衡(a) The current account balance and the merchandise trade balance in billions of dollars from 1960 to 2012. If the lines are above zero dollars, the United States was running a positive trade balance and current account balance. If the lines fall below zero dollars, the United States is running a trade deficit and a deficit in its current account balance. (b) These same items—trade balance and current account balance—are shown in relationship to the size of the U.S. economy, or GDP, from 1960 to 2012.

::从1960年至2012年,经常账户余额和商品贸易余额为数十亿美元,如果项目超过零美元,美国的贸易余额和经常账户余额为正数,如果项目低于零美元,美国的贸易赤字和经常账户余额为逆数。 (b)1960年至2012年,这些相同的项目----贸易余额和经常账户余额----与美国经济规模或国内生产总值(GDP)的关系显示为1960年至2012年。By either measure, the general pattern of the U.S. balance of trade is clear. From the 1960s into the 1970s, the U.S. economy had mostly small trade surpluses—that is, the graphs of 2 show positive numbers. However, starting in the 1980s, the trade deficit increased rapidly, and after a tiny surplus in 1991, the current account trade deficit got even larger in the late 1990s and into the mid-2000s. However, the trade deficit declined in 2009 after the recession had taken hold.

::无论以哪种衡量方法衡量,美国贸易平衡的总体格局是显而易见的。 从1960年代到1970年代,美国经济的贸易顺差大多很小 — — 也就是说,2的图表显示了正数。 但是,从1980年代开始,贸易逆差迅速增加,在1991年出现微小顺差之后,经常账户贸易逆差在1990年代末和2000年代中期甚至更大。 然而,在衰退持续之后,2009年贸易逆差下降。4 shows the U.S. trade picture in 2013 compared with some other economies from around the world. While the U.S. economy has consistently run trade deficits in recent years, Japan and many European nations, among them France and Germany, have consistently run trade surpluses. Some of the other countries listed include Brazil, the largest economy in Latin America; Nigeria, the largest economy in Africa; and China, India, and Korea. The first column offers one measure of the globalization of an economy: exports of goods and services as a percentage of GDP. The second column shows the trade balance. Most of the time, most countries have trade surpluses or deficits that are less than 5% of GDP. As you can see, the U.S. current account is negative 3.1%, while Germany’s is positive 6.2%.

::4 显示了美国2013年与世界其他经济体相比的贸易情况。 虽然美国经济近年来一直存在贸易赤字,但日本和许多欧洲国家,包括法国和德国,也一直存在贸易盈余。 所列其他国家包括巴西(拉丁美洲最大经济体 ) 、 尼日利亚(非洲最大经济体 ) 、 中国、印度和韩国。 第一栏提供了衡量经济全球化的一个尺度:商品和服务出口占GDP的百分比。 第二栏显示了贸易平衡。 大多数时候,大多数国家的贸易盈余或赤字不到GDP的5 % 。 如你所见,美国经常账户为负3.1 % , 德国为正6.2 % 。Level and Balance of Trade in 2012 (figures as a percentage of GDP)

::2012年贸易水平和贸易平衡情况(数字占国内生产总值的百分比)Exports of Goods and Services

::商品和服务出口品及 服务出口品及服务出口品出口品Current Account Balance

::往来账户结余United States

::美国 美国 美国 美国14%

–3.1%

Japan

::日本 日本 日本 日本 日本 日本 日本 日本15%

2.0%

Germany

::德国 德国50%

6.2%

United Kingdom

::联合王国 联合王国 联合王国 联合王国 联合王国32%

–1.3%

Canada

::加拿大 加拿大 加拿大30%

–3.0%

Sweden

::瑞典 瑞典 瑞典 瑞典50%

7.0%

Korea

::韩国56%

2.3%

Mexico

::墨西哥 墨西哥 墨西哥 墨西哥 墨西哥32%

–0.8%

Brazil

::巴西 巴西12%

–2.1%

China

::中国 中国 中国 中国 中国 中国 中国31%

1.9%

India

::印度 印度 印度24%

–3.2%

Nigeria

::尼日利亚 尼日利亚 尼日利亚40%

3.6%

World

::世界世界世界-

0.0%

The United States developed large trade surpluses in the early 1980s, swung back to a tiny trade surplus in 1991, and then had even larger trade deficits in the late 1990s and early 2000s. As we will see below, a trade deficit necessarily means a net inflow of financial capital from abroad, while a trade surplus necessarily means a net outflow of financial capital from an economy to other countries.

::美国在1980年代初发展了巨大的贸易顺差,在1991年回落到微小的贸易顺差,然后在1990年代末和2000年代初贸易逆差甚至更大。 如下文所示,贸易逆差必然意味着金融资本从国外净流入,而贸易顺差则必然意味着金融资本从一个经济体向其他国家的净流出。Trade Balances and Flows of Financial Capital

::贸易平衡和金融资本流动As economists see it, trade surpluses can be either good or bad, depending on circumstances, and trade deficits can be good or bad, too. The challenge is to understand how the international flows of goods and services are connected with international flows of financial capital. In this module we will illustrate the intimate connection between trade balances and flows of financial capital in two ways: a parable of trade between Robinson Crusoe and Friday, and a circular flow diagram representing flows of trade and payments.

::正如经济学家所看到的,贸易顺差可能好或坏,取决于环境,贸易逆差也可能好或坏。 挑战在于理解国际货物和服务流动如何与国际金融资本流动相联系。 在本模块中,我们将以两种方式说明贸易平衡和金融资本流动之间的密切关系:鲁滨逊·克鲁索和星期五之间的贸易比喻,以及代表贸易和支付流动的循环流动图。A Two-Person Economy: Robinson Crusoe and Friday

::双人经济:鲁滨逊·克鲁索和星期五To understand how economists view trade deficits and surpluses, consider a parable based on the story of Robinson Crusoe. Crusoe, as you may remember from the classic novel by Daniel Defoe first published in 1719, was shipwrecked on a desert island. After living alone for some time, he is joined by a second person, whom he names Friday. Think about the balance of trade in a two-person economy like that of Robinson and Friday.

::为了理解经济学家如何看待贸易赤字和盈余,请根据鲁滨逊·克鲁索的故事来思考一个比喻。 正如你可能从1719年首次出版的丹尼尔·德福(Daniel Defoe)的经典小说中所记得的那样,克鲁索在沙漠岛上沉船。 在独居一段时间后,他与第二个人一起度过了星期五。 想想像罗宾逊(Robinson)和星期五那样的双人经济的贸易平衡。Robinson and Friday trade goods and services. Perhaps Robinson catches fish and trades them to Friday for coconuts, or Friday weaves a hat out of tree fronds and trades it to Robinson for help in carrying water. For a period of time, each individual trade is self-contained and complete. Because each trade is voluntary, both Robinson and Friday must feel that they are receiving fair value for what they are giving. As a result, each person’s exports are always equal to his imports, and trade is always in balance between the two. Neither person experiences either a trade deficit or a trade surplus.

::鲁滨逊和星期五的商品和服务贸易。 也许鲁滨逊在捕捉鱼并将鱼交换成星期五的椰子,或者在星期五用树叶帽编织成一顶帽子,然后与鲁滨逊进行交易,以助运水。 在一段时间里,每个个体贸易都是自足和完整的。 由于每种贸易都是自愿的,鲁滨逊和星期五都必须感到它们所提供的产品得到了公平的价值。 因此,每个人的出口总是与进口品一样,贸易总是平衡的。 无论是贸易赤字还是贸易顺差都不是。However, one day Robinson approaches Friday with a proposition. Robinson wants to dig ditches for an irrigation system for his garden, but he knows that if he starts this project, he will not have much time left to fish and gather coconuts to feed himself each day. He proposes that Friday supply him with a certain number of fish and coconuts for several months, and then after that time, he promises to repay Friday out of the extra produce that he will be able to grow in his irrigated garden. If Friday accepts this offer, then a trade imbalance comes into being. For several months, Friday will have a trade surplus: that is, he is exporting to Robinson more than he is importing. More precisely, he is giving Robinson fish and coconuts, and at least for the moment, he is receiving nothing in return. Conversely, Robinson will have a trade deficit, because he is importing more from Friday than he is exporting.

::然而,有一天,鲁滨逊在星期五到来时提出一个提议。鲁滨逊想为花园的灌溉系统挖沟沟,但他知道,如果他开始这个项目,他将没有多少时间去捕鱼和收集椰子,每天养活自己。他提议星期五给他提供一定数量的鱼和椰子,为期数月,然后在那个时候之后,他承诺用他能在灌溉的花园里种植的额外产品偿还星期五。如果星期五接受这个提议,那么贸易不平衡就会出现。在几个月里,星期五将有一个贸易盈余:也就是说,他向鲁滨逊出口的比他进口的多。更确切地说,他给鲁滨逊鱼和椰子,而且至少在目前,他没有得到回报。相反,鲁滨逊将有一个贸易赤字,因为他从星期五进口的比出口的要多。This parable raises several useful issues in thinking about what a trade deficit and a trade surplus really mean in economic terms. The first issue raised by this story of Robinson and Friday is this: Is it better to have a trade surplus or a trade deficit? The answer, as in any voluntary market interaction, is that if both parties agree to the transaction, then they may both be better off. Over time, if Robinson’s irrigated garden is a success, it is certainly possible that both Robinson and Friday can benefit from this agreement.

::这一比喻在思考贸易赤字和贸易顺差在经济方面究竟意味着什么时,提出了几个有用的问题。 鲁滨逊和星期五这个故事所提出的第一个问题是:贸易顺差或贸易逆差是否更好? 在任何自愿的市场互动中,答案是,如果双方同意交易,那么双方都会更好。 随着时间的推移,如果鲁滨逊的灌溉园落成,罗宾逊和星期五都有可能从这一协议中受益。A second issue raised by the parable: What can go wrong? Robinson’s proposal to Friday introduces an element of uncertainty. Friday is, in effect, making a loan of fish and coconuts to Robinson, and Friday’s happiness with this arrangement will depend on whether that loan is repaid as planned, in full and on time. Perhaps Robinson spends several months loafing and never builds the irrigation system, or perhaps Robinson has been too optimistic about how much he will be able to grow with the new irrigation system, which turns out not to be very productive. Perhaps, after building the irrigation system, Robinson decides that he does not want to repay Friday as much as previously agreed. Any of these developments will prompt a new round of negotiations between Friday and Robinson. Friday’s attitude toward these renegotiations is likely to be shaped by why the repayment failed. If Robinson worked very hard and the irrigation system just did not increase production as intended, Friday may have some sympathy. If Robinson loafed or if he just refuses to pay, Friday may become irritated.

::第二个问题是由这个比喻提出的第二个问题:什么会出错?鲁滨逊的星期五提案引入了一个不确定因素。 事实上,星期五是向鲁滨逊提供鱼和椰子贷款,而星期五对这一安排的幸福度将取决于这笔贷款是否按计划、全额和按时偿还。 也许鲁滨逊花费了几个月的时间,并且从未建造灌溉系统,或者也许鲁滨逊对于他能够用新的灌溉系统来种植多少粮食过于乐观,而新的灌溉系统最终证明效果不佳。 也许,在建立灌溉系统之后,鲁滨逊决定他不想像以前约定的那样偿还星期五。 任何这些事态发展都会促使星期五和罗宾逊之间的新一轮谈判。 星期五对这些重新谈判的态度可能受偿还失败原因的影响。 如果鲁滨逊工作非常艰苦,灌溉系统也没有像预期的那样增加产量,那么周五可能有些同情。 如果鲁滨逊不努力,或者他只是拒绝支付,星期五可能会变得不耐烦。A third issue raised by the parable of Robinson and Friday is that an intimate relationship exists between a trade deficit and international borrowing, and between a trade surplus and international lending. The size of Friday’s trade surplus is exactly how much he is lending to Robinson. The size of Robinson’s trade deficit is exactly how much he is borrowing from Friday. Indeed, to economists, a trade surplus literally means the same thing as an outflow of financial capital, and a trade deficit literally means the same thing as an inflow of financial capital.

::罗宾逊和星期五的比喻提出的第三个问题是贸易赤字与国际借贷之间以及贸易盈余与国际借贷之间存在亲密关系。 星期五的贸易盈余规模正是他向罗宾逊贷款的数额。 鲁滨逊的贸易赤字规模正是他从星期五借款的数额。 事实上,对经济学家来说,贸易盈余实际上意味着金融资本外流,而贸易赤字也意味着金融资本流入。The story of Robinson and Friday also provides a good opportunity to consider the law of comparative advantage.

::鲁滨逊和星期五的故事也为审议相对优势法提供了一个很好的机会。The Balance of Trade as the Balance of Payments

::贸易平衡作为国际收支平衡The connection between trade balances and international flows of financial capital is so close that the balance of trade is sometimes described as the balance of payments. Each category of the current account balance involves a corresponding flow of payments between a given country and the rest of the world economy.

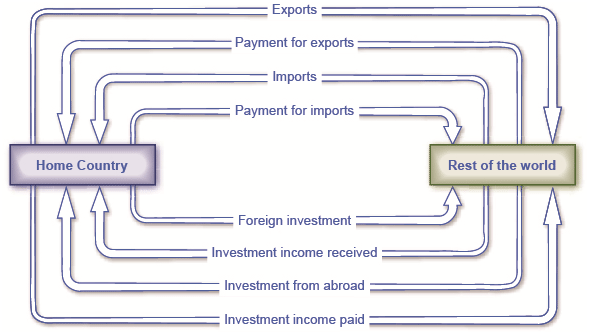

::贸易平衡与国际金融资本的国际流动之间的联系如此密切,以致贸易平衡有时被称为国际收支,经常账户的每类余额都涉及某一国家与世界经济其他部分之间的相应支付流量。3 shows the flow of goods and services and payments between one country—the United States in this example—and the rest of the world. The top line shows U.S. exports of goods and services, while the second line shows financial payments from purchasers in other countries back to the U.S. economy. The third line then shows U.S. imports of goods, services, and investment, and the fourth line shows payments from the home economy to the rest of the world. Flow of goods and services (lines one and three) show up in the current account, while flow of funds (lines two and four) are found in the financial account.

::第三行显示了货物和服务的流动以及一国——美国在此例中——和世界其他地区之间的支付情况。 上行显示了美国货物和服务的出口情况,第二行显示了其他国家购买者向美国经济的金融支付情况。 第三行则显示了美国商品、服务和投资的进口情况,第四行显示了从本国经济向世界其他地区的支付情况。 商品和服务的流动情况(第一和第二行)出现在经常账户中,而资金流动情况(第二和第三行)则出现在金融账户中。The bottom four lines of the 3 show the flow of investment income. In the first of the bottom lines, we see investments made abroad with funds flowing from the home country to rest of the world. Investment income stemming from an investment abroad then runs in the other direction from the rest of the world to the home country. Similarly, we see on the bottom third line, an investment from rest of the world into the home country and investment income (bottom fourth line) flowing from the home country to the rest of the world. The investment income (bottom lines two and four) are found in the current account, while investment to the rest of the world or into the home country (lines one and three) are found in the financial account. Unilateral transfers, the fourth item in the current account, are not shown in this figure.

::投资收入的底线是投资收入的流向。在底线的第1行,我们看到投资从母国流向世界其他地方。来自国外的投资收入随后从世界其他地区流向母国。同样,我们从底线第3行看到来自世界其他地区的投资流向母国,投资收入(底线第四行)从母国流向世界其他地方。投资收入(底线第二和四行)在经常账户中找到,而对世界其他地区或母国的投资(第1和第3行)则在金融账户中找到。经常账户中的第4项单方面转移(第4项)没有显示于本图中。Flow of Investment Goods and Capital

::投资、货物和资本流动Each element of the current account balance involves a flow of financial payments between countries. The top line shows exports of goods and services leaving the home country; the second line shows the money received by the home country for those exports. The third line shows imports received by the home country; the fourth line shows the payments sent abroad by the home country in exchange for these imports.

::经常账户余额的每个部分都涉及国家间的金融支付流动,头一栏显示离开母国的货物和服务出口;第二栏显示母国为这些出口收到的资金;第三栏显示母国收到的进口;第四栏显示母国为交换这些进口而汇往国外的付款。A current account deficit means that the country is a net borrower from abroad. Conversely, a positive current account balance means a country is a net lender to the rest of the world. Just like the parable of Robinson and Friday, the lesson is that a trade surplus means an overall outflow of financial investment capital, as domestic investors put their funds abroad, while the deficit in the current account balance is exactly equal to the overall or net inflow of foreign investment capital from abroad.

::经常账户赤字意味着该国是国外净借款国。 相反,正对经常账户余额意味着一个国家是世界其他地区的净贷款国。 正如鲁滨逊和星期五的比喻一样,教训是贸易顺差意味着金融投资资本的全面外流,因为国内投资者将其资金投向国外,而经常账户余额的逆差与国外外国投资资本的总体或净流入量完全相等。It is important to recognize that an inflow and outflow of foreign capital does not necessarily refer to a debt that governments owe to other governments, although government debt may be part of the picture. Instead, these international flows of financial capital refer to all of the ways in which private investors in one country may invest in another country—by buying real estate, companies, and financial investments like stocks and bonds.

::必须认识到,外国资本的流入和流出并不一定是指政府欠其他国家政府的债务,尽管政府债务可能也是其中的一部分。 相反,这些国际金融资本流动指的是一国私人投资者通过购买房地产、公司和股票和债券等金融投资在另一国投资的所有方式。International flows of goods and services are closely connected to the international flows of financial capital. A current account deficit means that, after taking all the flows of payments from goods, services, and income together, the country is a net borrower from the rest of the world. A current account surplus is the opposite and means the country is a net lender to the rest of the world.

::国际货物和服务流动与国际金融资本流动密切相关,经常账户赤字意味着,在综合了所有来自货物、服务和收入的支付流量之后,该国成为世界其他地区的净借款国,经常账户顺差正好相反,这意味着该国是世界其他地区的净贷款国。The National Saving and Investment Identity

::国家储蓄和投资身份The close connection between trade balances and international flows of savings and investments leads to a macroeconomic analysis. This approach views trade balances—and their associated flows of financial capital—in the context of the overall levels of savings and financial investment in the economy.

::贸易平衡与储蓄和投资的国际流动之间的密切联系导致进行宏观经济分析,从经济储蓄和金融投资的总体水平来看贸易平衡及其相关的金融资本流动。Understanding the Determinants of the Trade and Current Account Balance

::了解贸易和经常账户余额的决定因素The national saving and investment identity provides a useful way to understand the determinants of the trade and current account balance. In a nation’s financial capital market, the quantity of financial capital supplied at any given time must equal the quantity of financial capital demanded for purposes of making investments. What is on the supply and demand sides of financial capital? See the following Clear It Up feature for the answer to this question .

::国民储蓄和投资身份为理解贸易和经常账户平衡的决定因素提供了有用的方法。 在一个国家的金融资本市场上,任何特定时间提供的金融资本数量必须等于投资所需的金融资本数量。 金融资本的供需方面有什么问题? 这个问题的答案见下面的Clear It Up特征。What comprises the supply and demand of financial capital?

::什么是金融资本的供求?A country’s national savings is the total of its domestic savings by household and companies (private savings) as well as the government (public savings). If a country is running a trade deficit, it means money from abroad is entering the country and is considered part of the supply of financial capital.

::一个国家的国民储蓄是家庭和公司(私人储蓄)以及政府(公共储蓄)的国内储蓄总量。 如果一个国家贸易赤字,这意味着国外资金进入该国,并被视为金融资本供应的一部分。The demand for financial capital (money) represents groups that are borrowing the money. Businesses need to borrow to finance their investments in factories, materials, and personnel. When the federal government runs a budget deficit, it is also borrowing money from investors by selling Treasury bonds. So both business investment and the federal government can demand (or borrow) the supply of savings.

::金融资本(金钱)需求代表着正在借钱的集团。 企业需要借款来为工厂、材料和人员投资提供资金。 当联邦政府出现预算赤字时,它也通过出售国库债券向投资者借款。 因此,企业投资和联邦政府都可以要求(或借用)储蓄供应。There are two main sources for the supply of financial capital in the U.S. economy: saving by individuals and firms, called S, and the inflow of financial capital from foreign investors, which is equal to the trade deficit (M – X), or imports minus exports. There are also two main sources of demand for financial capital in the U.S. economy: private sector investment, I, and government borrowing, where the government needs to borrow when government spending, G, is higher than the taxes collected, T. This national savings and investment identity can be expressed in algebraic terms:

::美国经济的金融资本供应有两大主要来源:个人和公司储蓄(称为S ) , 外国投资者的金融资本流入(相当于贸易赤字(M-X ) ) , 或进口减出口 ) 。 美国经济的金融资本需求还有两大主要来源:私营部门投资(I)和政府借贷(政府支出(G)高于税收时政府需要借款 ) , T。 这一国家储蓄和投资特征可以用代数表达:Supply of financial capital = Demand for financial capital

::提供金融资本=对金融资本的需求S + (M – X) = I + (G – T)

::S+ (M - X) = I + (G - T)Again, in this equation, S is private savings, T is taxes, G is government spending, M is imports, X is exports, and I is investment. This relationship is true as a matter of definition because, for the macro economy, the quantity supplied of financial capital must be equal to the quantity demanded.

::同样,在这个等式中,S是私人储蓄,T是税收,G是政府支出,M是进口,X是出口,而I是投资。 这种关系在定义上是正确的,因为对于宏观经济来说,金融资本的供应量必须等于要求的数量。However, certain components of the national savings and investment identity can switch between the supply side and the demand side. Some countries, like the United States in most years since the 1970s, have budget deficits, which mean the government is spending more than it collects in taxes, and so the government needs to borrow funds. In this case, the government term would be G – T > 0, showing that spending is larger than taxes, and the government would be a demander of financial capital on the right-hand side of the equation (that is, a borrower), not a supplier of financial capital on the right-hand side. However, if the government runs a budget surplus so that the taxes exceed spending, as the U.S. government did from 1998 to 2001, then the government in that year was contributing to the supply of financial capital (T – G > 0), and would appear on the left (saving) side of the national savings and investment identity.

::然而,国民储蓄和投资身份的某些组成部分可以在供应方和需求方之间发生转变。 有些国家,如美国(1970年代以来的多数年份 ) , 有预算赤字,这意味着政府支出超过税收,因此政府需要借款。 在这种情况下,政府任期为G - T > 0,表明支出大于税收,而政府则是对金融资本的需求方(即借款方 ) , 而不是右翼金融资本的供应方。 但是,如果政府预算盈余导致税收超过支出,就像美国政府1998-2001年所做的那样,那么当年,政府将为金融资本(T - G > 0)的供应做出贡献,并出现在国家储蓄和投资身份的左(储蓄)一边。Similarly, if a national economy runs a trade surplus, the trade sector will involve an outflow of financial capital to other countries. A trade surplus means that the domestic financial capital is in surplus within a country and can be invested in other countries.

::同样,如果国民经济出现贸易顺差,贸易部门将涉及金融资本外流到其他国家,贸易顺差意味着国内金融资本在一国国内出现顺差,可以投资到其他国家。The fundamental notion that total quantity of financial capital demanded equals total quantity of financial capital supplied must always remain true. Domestic savings will always appear as part of the supply of financial capital and domestic investment will always appear as part of the demand for financial capital. However, the government and trade balance elements of the equation can move back and forth as either suppliers or demanders of financial capital, depending on whether government budgets and the trade balance are in surplus or deficit.

::金融资本总量要求等于所提供金融资本总量的基本概念必须始终是真实的。 国内储蓄总是作为金融资本供应的一部分出现,国内投资也总是作为金融资本需求的一部分出现。 但是,政府和贸易平衡因素可以作为金融资本的供货方或需求方来回移动,这取决于政府预算和贸易平衡是盈余还是赤字。Domestic Saving and Investment Determine the Trade Balance

::确定贸易平衡One insight from the national saving and investment identity is that a nation’s balance of trade is determined by that nation’s own levels of domestic saving and domestic investment. To understand this point, rearrange the identity to put the balance of trade all by itself on one side of the equation. Consider first the situation with a trade deficit, and then the situation with a trade surplus.

::国民储蓄和投资身份的一个深刻观点是,一个国家的贸易平衡取决于该国自身的国内储蓄和国内投资水平。 为了理解这一点,重新排列身份,将贸易平衡本身置于等式的一边。 首先考虑贸易赤字,然后考虑贸易顺差。In the case of a trade deficit, the national saving and investment identity can be rewritten as:

::在出现贸易赤字的情况下,可以将国民储蓄和投资特性改写为:Trade deficit= Domestic investment – Private domestic saving – Government (or public) savings

::贸易赤字=国内投资-私人国内储蓄-政府(或公共)储蓄(M – X) = I – S – (T – G)

:In this case, domestic investment is higher than domestic saving, including both private and government saving. The only way that domestic investment can exceed domestic saving is if capital is flowing into a country from abroad. After all, that extra financial capital for investment has to come from someplace.

::在这种情况下,国内投资高于国内储蓄,包括私人和政府储蓄。 国内投资能够超过国内储蓄的唯一途径是资本从国外流入一个国家。 毕竟,投资的额外金融资本必须来自某个地方。Now consider a trade surplus from the standpoint of the national saving and investment identity:

::现在从国民储蓄和投资身份的角度考虑贸易顺差:Trade surplus= Private domestic saving + Public saving – Domestic investment

::贸易盈余=私人国内储蓄+公共储蓄-国内投资(X – M) = S + (T – G) – I

:In this case, domestic savings (both private and public) is higher than domestic investment. That extra financial capital will be invested abroad.

::在这种情况下,国内储蓄(包括私人和公共储蓄)高于国内投资,额外金融资本将在国外投资。This connection of domestic saving and investment to the trade balance explains why economists view the balance of trade as a fundamentally macroeconomic phenomenon. As the national saving and investment identity shows, the trade balance is not determined by the performance of certain sectors of an economy, like cars or steel. Nor is the trade balance determined by whether the nation’s trade laws and regulations encourage free trade or protectionism.

::国内储蓄和投资与贸易平衡的这种联系解释了经济学家为什么将贸易平衡视为根本的宏观经济现象。 正如国民储蓄和投资身份所显示的那样,贸易平衡不是由汽车或钢铁等经济的某些部门的表现决定的。 贸易平衡也不是由国家贸易法律和法规是否鼓励自由贸易或保护主义决定的。Exploring Trade Balances One Factor at a Time

::一次探讨贸易平衡的一个因素The national saving and investment identity also provides a framework for thinking about what will cause trade deficits to rise or fall. Begin with the version of the identity that has domestic savings and investment on the left and the trade deficit on the right:

::国民储蓄和投资身份也为思考导致贸易赤字上升或下降的原因提供了一个框架。Domestic investment – Private domestic savings – Public domestic savings= Trade deficit

::国内投资-私人国内储蓄-公共国内储蓄=贸易赤字I – S – (T – G) = (M – X)

::我 - (T - G) = (M - X)Now, consider the factors on the left-hand side of the equation one at a time, while holding the other factors constant.

::现在,考虑方程左侧的一个时段因素,同时保持其他因素不变。As a first example, assume that the level of domestic investment in a country rises, while the level of private and public saving remains unchanged. The result is shown in the first row of under the equation. Since the equality of the national savings and investment identity must continue to hold—it is, after all, an identity that must be true by definition—the rise in domestic investment will mean a higher trade deficit. This situation occurred in the U.S. economy in the late 1990s. Because of the surge of new information and communications technologies that became available, business investment increased substantially. A fall in private saving during this time and a rise in government saving more or less offset each other. As a result, the financial capital to fund that business investment came from abroad, which is one reason for the very high U.S. trade deficits of the late 1990s and early 2000s.

::首先,假设一国的国内投资水平上升,而私人和公共储蓄水平保持不变,结果在等式第一行中显示出来。由于国民储蓄和投资身份的平等必须继续维持下去,毕竟,从定义上来说,这是一个必须真实的特征,国内投资的增加将意味着贸易赤字增加。这种情况发生在1990年代末期美国经济中。由于新信息和通信技术的激增,商业投资大幅度增加。这一时期私人储蓄的下降和政府储蓄的上升或多或少地抵消了两者。结果,为这种商业投资提供资金的金融资本来自国外,这是1990年代末和2000年代初期美国贸易赤字极高的原因之一。Causes of a Changing Trade Balance

::贸易平衡变化的原因Domestic Investment

::国内投资–

Private Domestic Savings

::私人国内储蓄–

Public Domestic Savings

::公共国内储蓄=

Trade Deficit

::贸易赤字I

::一一–

S

::S S 级–

(T – G)

:=

(M – X)

:Up

::上上No change

::无改动No change

::无改动Then M – X must rise

::然后M - X必须升起No change

::无改动Up

::上上No change

::无改动Then M – X must fall

::然后M -X必须坠落No change

::无改动No change

::无改动Down

::下下下Then M – X must rise

::然后M - X必须升起As a second scenario, assume that the level of domestic savings rises, while the level of domestic investment and public savings remain unchanged. In this case, the trade deficit would decline. As domestic savings rises, there would be less need for foreign financial capital to meet investment needs. For this reason, a policy proposal often made for reducing the U.S. trade deficit is to increase private saving—although exactly how to increase the overall rate of saving has proven controversial.

::作为第二种设想,假设国内储蓄水平上升,而国内投资和公共储蓄水平保持不变;在这种情况下,贸易赤字将下降;随着国内储蓄的增加,对外国金融资本满足投资需求的需求将减少。 因此,经常提出的减少美国贸易赤字的政策建议是增加私人储蓄 — — 尽管如何提高总储蓄率确实有争议。As a third scenario, imagine that the government budget deficit increased dramatically, while domestic investment and private savings remained unchanged. This scenario occurred in the U.S. economy in the mid-1980s. The federal budget deficit increased from $79 billion in 1981 to $221 billion in 1986—an increase in the demand for financial capital of $142 billion. The current account balance collapsed from a surplus of $5 billion in 1981 to a deficit of $147 million in 1986—an increase in the supply of financial capital from abroad of $152 billion. The two numbers do not match exactly, since in the real world, private savings and investment did not remain fixed. The connection at that time is clear: a sharp increase in government borrowing increased the U.S. economy’s demand for financial capital, and that increase was primarily supplied by foreign investors through the trade deficit. The following Work It Out feature walks you through a scenario in which domestic savings has to rise by a certain amount to reduce a trade deficit.

::第三种设想是,想象一下政府预算赤字急剧增加,而国内投资和私人储蓄却保持不变。这种情形发生在1980年代中期的美国经济。联邦预算赤字从1981年的790亿美元增加到1986年的2,210亿美元,对金融资本的需求增加了1,420亿美元。 经常账户余额从1981年的50亿美元盈余下降到1986年的1.47亿美元赤字 — — 国外金融资本供应增加了1,520亿美元。 这个数字并不完全吻合,因为在现实世界中,私人储蓄和投资没有固定下来。 当时的关联是显而易见的:政府借贷的急剧增长增加了美国对金融资本的需求,而这一增长主要是由外国投资者通过贸易赤字提供的。 随后的工作表现在一种情景中,即国内储蓄必须增加一定数额才能减少贸易赤字。Short-Term Movements in the Business Cycle and the Trade Balance

::商业周期和贸易平衡的短期流动In the short run, trade imbalances can be affected by whether an economy is in a recession or on the upswing. A recession tends to make a trade deficit smaller, or a trade surplus larger, while a period of strong economic growth tends to make a trade deficit larger, or a trade surplus smaller.

::短期而言,贸易失衡可能受经济处于衰退还是上升趋势的影响。 衰退往往使贸易赤字减少,贸易盈余增加,而经济强劲增长的时期则使贸易赤字增加,贸易盈余减少。As an example, note that the U.S. trade deficit declined by almost half from 2006 to 2009. One primary reason for this change is that during the recession, as the U.S. economy slowed down, it purchased fewer of all goods, including fewer imports from abroad. However, buying power abroad fell less, and so U.S. exports did not fall by as much.

::举例来说,请注意美国贸易赤字从2006年到2009年下降了近一半。 这一变化的主要原因之一是,在经济衰退期间,随着美国经济放缓,美国购买的商品减少了,包括从国外进口的商品也减少了。 然而,国外购买力的下降减少了,因此美国的出口并没有减少多少。Conversely, in the mid-2000s, when the U.S. trade deficit became very large, a contributing short-term reason is that the U.S. economy was growing. As a result, there was lots of aggressive buying in the U.S. economy, including the buying of imports. Thus, a rapidly growing domestic economy is often accompanied by a trade deficit (or a much lower trade surplus), while a slowing or recessionary domestic economy is accompanied by a trade surplus (or a much lower trade deficit).

::相反,在20世纪20年代中期,当美国贸易赤字变得非常巨大时,造成短期原因的一个原因就是美国经济正在增长。 结果,美国经济中出现了大量激进的购买,包括进口品的购买。 因此,国内经济的快速增长往往伴随着贸易赤字(或贸易顺差要低得多 ) , 而国内经济的放缓或衰退则伴随着贸易顺差(或贸易逆差要低得多 ) 。When the trade deficit rises, it necessarily means a greater net inflow of foreign financial capital. The national saving and investment identity teaches that the rest of the economy can absorb this inflow of foreign financial capital in several different ways. For example, the additional inflow of financial capital from abroad could be offset by reduced private savings, leaving domestic investment and public saving unchanged. Alternatively, the inflow of foreign financial capital could result in higher domestic investment, leaving private and public saving unchanged. Yet another possibility is that the inflow of foreign financial capital could be absorbed by greater government borrowing, leaving domestic saving and investment unchanged. The national saving and investment identity does not specify which of these scenarios, alone or in combination, will occur—only that one of them must occur.

::当贸易赤字上升时,它必然意味着外国金融资本的净流入量增加。 国民储蓄和投资身份表明,其他经济体可以通过几种不同的方式吸收外国金融资本的流入量。 例如,国外金融资本的流入量的增加可以由私人储蓄的减少来抵消,使国内投资和公共储蓄保持不变。 或者,外国金融资本的流入可能导致国内投资增加,使私人和公共储蓄保持不变。 另一种可能性是,外国金融资本的流入量可以通过政府借贷的增加来吸收,使国内储蓄和投资保持不变。 国民储蓄和投资身份没有说明这些情形中的哪一种将单独或合并发生 — — 只有其中一种情况必须发生。The national saving and investment identity is based on the relationship that the total quantity of financial capital supplied from all sources must equal the total quantity of financial capital demanded from all sources. If S is private saving, T is taxes, G is government spending, M is imports, X is exports, and I is investment, then for an economy with a current account deficit and a budget deficit:

::国民储蓄和投资的特征是基于一种关系,即从所有来源提供的金融资本总量必须等于所有来源所需的金融资本总量。 如果S是私人储蓄,T是税收,G是政府支出,M是进口,X是出口,而I是投资,那么对于经常账户赤字和预算赤字的经济体来说:Supply of financial capital = Demand for financial capital

::提供金融资本=对金融资本的需求S + (M – X) = I + (G – T)

::S+ (M - X) = I + (G - T)A recession tends to increase the trade balance (meaning a higher trade surplus or lower trade deficit), while economic boom will tend to decrease the trade balance (meaning a lower trade surplus or a larger trade deficit).

::衰退倾向于增加贸易平衡(意味着贸易顺差增加或贸易逆差减少),而经济繁荣则倾向于减少贸易平衡(意味着贸易顺差减少或贸易逆差增加)。The Pros and Cons of Trade Deficits and Surpluses

::贸易赤字和盈余的利弊Because flows of trade always involve flows of financial payments, flows of international trade are actually the same as flows of international financial capital. The question of whether trade deficits or surpluses are good or bad for an economy is, in economic terms, exactly the same question as whether it is a good idea for an economy to rely on net inflows of financial capital from abroad or to make net investments of financial capital abroad. Conventional wisdom often holds that borrowing money is foolhardy, and that a prudent country, like a prudent person, should always rely on its own resources. While it is certainly possible to borrow too much—as anyone with an overloaded credit card can testify—borrowing at certain times can also make sound economic sense. For both individuals and countries, there is no economic merit in a policy of abstaining from participation in financial capital markets.

::由于贸易流动总是涉及金融支付流动,国际贸易流动实际上与国际金融资本流动相同,就经济而言,贸易赤字或顺差对一个经济体是好还是坏的问题与一个经济体依赖国外资金净流入或对国外资金进行净投资是否是一个好主意的问题完全相同,传统智慧往往认为,借款是愚蠢的,谨慎的国家像谨慎的人一样,应该始终依赖自己的资源,当然,借款过多是可能的,因为持有过量信用卡的人可以证明,在一定时间借款也具有良好的经济意义,对个人和国家来说,不参与金融资本市场的政策都没有经济价值。It makes economic sense to borrow when you are buying something with a long-run payoff; that is, when you are making an investment. For this reason, it can make economic sense to borrow for a college education, because the education will typically allow you to earn higher wages, and so to repay the loan and still come out ahead. It can also make sense for a business to borrow in order to purchase a machine that will last 10 years, as long as the machine will increase output and profits by more than enough to repay the loan. Similarly, it can make economic sense for a national economy to borrow from abroad, as long as the money is wisely invested in ways that will tend to raise the nation’s economic growth over time. Then, it will be possible for the national economy to repay the borrowed money over time and still end up better off than before.

::在购买具有长期回报的东西时,借款在经济上是有道理的;也就是说,在投资时。 因此,为大学教育借款在经济上是有道理的,因为教育通常允许你赚取更高的工资,从而偿还贷款,然后继续走下去。 企业借钱以购买机器也是合理的,只要机器能增加产出和利润,超过偿还贷款的足够数量。 同样,国民经济从国外借钱也可以在经济上是有道理的,只要资金投资明智,能够逐渐提高国家经济增长。 之后,国民经济有可能在一段时间内偿还借来的钱,最终仍然比以前更好。One vivid example of a country that borrowed heavily from abroad, invested wisely, and did perfectly well is the United States during the nineteenth century. The United States ran a trade deficit in 40 of the 45 years from 1831 to 1875, which meant that it was importing capital from abroad over that time. However, that financial capital was, by and large, invested in projects like railroads that brought a substantial economic payoff.

::一个从国外大量借款、明智地投资并且做得非常好的国家的生动例子就是19世纪的美国。 美国从1831年到1875年的45年中40年出现贸易赤字,这意味着美国在1831年到1875年的45年中40年从国外进口资本。 然而,金融资本基本上投资于铁路等项目,从而带来巨大的经济回报。A more recent example along these lines is the experience of South Korea, which had trade deficits during much of the 1970s—and so was an importer of capital over that time. However, South Korea also had high rates of investment in physical plant and equipment, and its economy grew rapidly. From the mid-1980s into the mid-1990s, South Korea often had trade surpluses—that is, it was repaying its past borrowing by sending capital abroad.

::这方面最近的一个例子是南朝鲜的经验,南朝鲜在1970年代的大部分时间里存在贸易逆差,而当时的资本进口国也是如此,然而,南朝鲜在工厂和设备方面的投资率也很高,其经济也迅速增长。 从1980年代中期到1990年代中期,南朝鲜经常有贸易顺差 — — 也就是说,南朝鲜通过向国外输出资本来偿还过去的借款。In contrast, some countries have run large trade deficits, borrowed heavily in global capital markets, and ended up in all kinds of trouble. Two specific sorts of trouble are worth examining. First, a borrower nation can find itself in a bind if the incoming funds from abroad are not invested in a way that leads to increased productivity. Several of the large economies of Latin America, including Mexico and Brazil, ran large trade deficits and borrowed heavily from abroad in the 1970s, but the inflow of financial capital did not boost productivity sufficiently, which meant that these countries faced enormous troubles repaying the money borrowed when economic conditions shifted during the 1980s. Similarly, it appears that a number of African nations that borrowed foreign funds in the 1970s and 1980s did not invest in productive economic assets. As a result, several of those countries later faced large interest payments, with no economic growth to show for the borrowed funds.

::相比之下,一些国家贸易赤字巨大,大量借入全球资本市场,最终陷入了各种麻烦。 有两个具体的麻烦值得研究。 首先,如果来自国外的资金没有以提高生产力的方式投资国外资金,借款国就会陷入困境。 包括墨西哥和巴西在内的拉丁美洲一些大型经济体在1970年代出现巨额贸易赤字,从国外大量借入,但金融资本的流入并未充分提高生产力,这意味着这些国家在1980年代经济条件发生变化时,在偿还借款方面面临巨大困难。 同样,一些在1970年代和1980年代借入外国资金的非洲国家似乎没有投资于生产性经济资产。 结果,其中一些国家后来面临巨额利息支付,而没有经济增长来证明借出资金。Are trade deficits always harmful?

::贸易赤字是否总是有害的?For most years of the nineteenth century, U.S. imports exceeded exports and the U.S. economy had a trade deficit. Yet the string of trade deficits did not hold back the economy at all; instead, the trade deficits contributed to the strong economic growth that gave the U.S. economy the highest per capita GDP in the world by around 1900.

::在十九世纪的大部分几年里,美国进口超过了出口,美国经济也出现了贸易赤字。 然而,一系列贸易赤字并没有抑制经济;相反,贸易赤字促成了强劲的经济增长,使美国经济在1900年左右成为世界人均GDP最高的国家。The U.S. trade deficits meant that the U.S. economy was receiving a net inflow of foreign capital from abroad. Much of that foreign capital flowed into two areas of investment—railroads and public infrastructure like roads, water systems, and schools—which were important to helping the growth of the U.S. economy.

::美国的贸易赤字意味着美国经济正从国外净流入外国资本。 大部分外国资本流入两个领域 — — 铁路和公路、供水系统和学校等公共基础设施 — — 对帮助美国经济增长非常重要。The effect of foreign investment capital on U.S. economic growth should not be overstated. In most years the foreign financial capital represented no more than 6–10% of the funds used for overall physical investment in the economy. Nonetheless, the trade deficit and the accompanying investment funds from abroad were clearly a help, not a hindrance, to the U.S. economy in the nineteenth century.

::外国投资资本对美国经济增长的影响不应该被夸大。 在大多数年份,外国金融资本只占用于经济整体实物投资的资金的不到6-10%。 尽管如此,贸易赤字和国外投资资金显然对十九世纪的美国经济是一种帮助,而不是障碍。A second “trouble” is: What happens if the foreign money flows in, and then suddenly flows out again? This scenario was raised at the start of the chapter. In the mid-1990s, a number of countries in East Asia—Thailand, Indonesia, Malaysia, and South Korea—ran large trade deficits and imported capital from abroad. However, in 1997 and 1998 many foreign investors became concerned about the health of these economies and quickly pulled their money out of stock and bond markets, real estate, and banks. The extremely rapid departure of that foreign capital staggered the banking systems and economies of these countries, plunging them into a deep recession.

::第二个“麻烦”是:如果外国资金流入,然后突然再次流出,会发生什么情况?这一假设是在这一章的开头提出来的。 在1990年代中期,东亚的一些国家 — — 泰国、印度尼西亚、马来西亚和韩国 — — 出现了巨大的贸易赤字和国外进口资本。 然而,在1997年和1998年,许多外国投资者开始关注这些经济体的健康状况,并迅速将其资金从股票和债券市场、房地产和银行中抽出。 外国资本极快地冲破了这些国家的银行体系和经济,使它们陷入了深度衰退。While a trade deficit is not always harmful, there is no guarantee that running a trade surplus will bring robust economic health. For example, Germany and Japan ran substantial trade surpluses for most of the last three decades. Regardless of their persistent trade surpluses, both countries have experienced occasional recessions and neither country has had especially robust annual growth in recent years

::尽管贸易赤字并不总是有害于贸易赤字,但不能保证贸易顺差会带来强劲的经济健康。 比如,在过去三十年的大部分时间里,德国和日本都拥有巨大的贸易顺差。 尽管两国贸易顺差持续不减,但两国都偶尔经历衰退,而且两国都没有近年来特别强劲的年增长率。The sheer size and persistence of the U.S. trade deficits and inflows of foreign capital since the 1980s are a legitimate cause for concern. The huge U.S. economy will not be destabilized by an outflow of international capital as easily as, say, the comparatively tiny economies of Thailand and Indonesia were in 1997–1998. Even an economy that is not knocked down, however, can still be shaken. American policymakers should certainly be paying attention to those cases where a pattern of extensive and sustained current account deficits and foreign borrowing has gone badly—if only as a cautionary tale.

::20世纪80年代以来,美国贸易赤字和外国资本流入的庞大规模和持久性是引起关注的合理原因。 美国巨大的经济不会像1997-1998年泰国和印度尼西亚相对较小的经济体那样容易地因为国际资本外流而动荡不安。 但是,即使是一个没有被击倒的经济,也仍然可以动摇。 美国决策者当然应该关注那些经常账户大量持续赤字和外国借款模式已经严重恶化的案例 — — 哪怕只是作为一个警告性的故事。Are trade surpluses always beneficial? Considering Japan since the 1990s.

::贸易顺差是否总是有利可图?Perhaps no economy around the world is better known for its trade surpluses than Japan. Since 1990, the size of these surpluses has often been near $100 billion per year. When Japan’s economy was growing vigorously in the 1960s and 1970s, its large trade surpluses were often described, especially by non-economists, as either a cause or a result of its robust economic health. But from a standpoint of economic growth, Japan’s economy has been teetering in and out of recession since 1990, with real GDP growth averaging only about 1% per year, and an unemployment rate that has been creeping higher. Clearly, a whopping trade surplus is no guarantee of economic good health.

::也许全世界没有哪个经济体比日本更能以贸易顺差闻名于世。 自1990年以来,这些顺差的规模往往每年近1 000亿美元。 当日本经济在1960年代和1970年代强劲增长时,其巨大的贸易顺差常常被描述为其强劲经济健康的原因或结果 — — 特别是非经济主义者。 但从经济增长的角度来看,日本经济自1990年以来一直处于衰退中和衰退之外,实际GDP增长率每年平均只有约1 % , 失业率不断攀升。 显然,巨额贸易顺差并不能保证经济健康。Instead, Japan’s trade surplus reflects that Japan has a very high rate of domestic savings, more than the Japanese economy can invest domestically, and so the extra funds are invested abroad. In Japan’s slow economy, the growth of consumption is relatively low, which also means that consumption of imports is relatively low. Thus, Japan’s exports continually exceed its imports, leaving the trade surplus continually high. Recently, Japan’s trade surpluses began to deteriorate. In 2013, Japan ran a trade deficit due to the high cost of imported oil.

::相反,日本的贸易顺差反映出日本国内储蓄率非常高,比日本经济能在国内投资的还多,因此额外资金可以在国外投资。 在日本经济缓慢的情况下,消费增长相对较低,这也意味着进口消费相对较低。 因此,日本的出口持续超过进口,贸易顺差持续居高不下。 最近,日本的贸易顺差开始恶化。 2013年,日本由于进口石油成本高而出现贸易逆差。Trade surpluses are no guarantee of economic health, and trade deficits are no guarantee of economic weakness. Either trade deficits or trade surpluses can work out well or poorly, depending on whether the corresponding flows of financial capital are wisely invested.

::贸易顺差不是经济健康保障,贸易逆差也不是经济疲软的保障。 贸易逆差或贸易顺差要么可以顺利解决,要么只能解决,取决于相应的金融资本流动是否明智地投资。The Difference between Level of Trade and the Trade Balance

::贸易水平与贸易平衡之间的差别A nation’s level of trade may at first sound like much the same issue as the balance of trade, but these two are actually quite separate. It is perfectly possible for a country to have a very high level of trade—measured by its exports of goods and services as a share of its GDP—while it also has a near-balance between exports and imports. A high level of trade indicates that a good portion of the nation’s production is exported. It is also possible for a country’s trade to be a relatively low share of GDP, relative to global averages, but for the imbalance between its exports and its imports to be quite large.

::一个国家的贸易水平最初可能听起来与贸易平衡问题大致相同,但两者实际上是完全分开的。 一个国家完全有可能拥有极高的贸易水平 — — 以其商品和服务出口占GDP的比例来衡量 — — 而其出口和进口之间也接近平衡。 高水平的贸易表明该国生产中有很大一部分是出口的。 相对于全球平均水平而言,一个国家的贸易在GDP中的比例也相对较低,但出口与进口之间的不平衡却相当大。A country’s level of trade tells how much of its production it exports. This is measured by the percent of exports out of GDP. It indicates how globalized an economy is. Some countries, such as Germany, have a high level of trade—they export 50% of their total production. The balance of trade tells us if the country is running a trade surplus or trade deficit. A country can have a low level of trade but a high trade deficit. (For example, the United States only exports 14% of GDP, but it has a trade deficit of $560 billion.)

::一个国家的贸易水平能说明它出口的产量的多少。这是以出口占GDP的百分比来衡量的。它能说明一个经济是如何全球化的。德国等一些国家的贸易水平很高 — — 它们出口了总产量的50 % 。 贸易平衡能告诉我们这个国家是否出现贸易盈余或贸易赤字。 一个国家的贸易水平很低,但贸易赤字却很高。 (例如,美国只出口GDP的14 % , 但贸易赤字为5600亿美元。 )Three factors strongly influence a nation’s level of trade: the size of its economy, its geographic location, and its history of trade. Large economies like the United States can do much of their trading internally, while small economies like Sweden have less ability to provide what they want internally and tend to have higher ratios of exports and imports to GDP. Nations that are neighbors tend to trade more, since costs of transportation and communication are lower. Moreover, some nations have long and established patterns of international trade, while others do not.

::三大因素强烈地影响了一个国家的贸易水平:其经济规模、地理位置和贸易历史。 美国等大型经济体可以在内部做大部分贸易,而瑞典等小型经济体在内部提供自己想要的东西的能力较低,而且往往进出口与GDP的比率较高。 作为邻国的国家往往贸易量更多,因为运输和通信成本较低。 此外,一些国家有着长期既定的国际贸易模式,而其他国家则没有。Consequently, a relatively small economy like Sweden, with many nearby trading partners across Europe and a long history of foreign trade, has a high level of trade. Brazil and India, which are fairly large economies that have often sought to inhibit trade in recent decades, have lower levels of trade. Whereas, the United States and Japan are extremely large economies that have comparatively few nearby trading partners. Both countries actually have quite low levels of trade by world standards. The ratio of exports to GDP in either the United States or in Japan is about half of the world average.

::因此,像瑞典这样的相对较小的经济体,其贸易水平很高,其贸易伙伴遍布欧洲,贸易伙伴众多,对外贸易历史悠久。 巴西和印度是近几十年来经常试图抑制贸易的相当大经济体,它们的贸易水平较低。 而美国和日本则是极为庞大的经济体,其贸易伙伴相对较少。这两个国家按照世界标准的贸易水平实际上都相当低。 美国或日本的出口与GDP的比率都相当于世界平均水平的一半左右。The balance of trade is a separate issue from the level of trade. The United States has a low level of trade but had enormous trade deficits for most years from the mid-1980s into the 2000s. Japan has a low level of trade by world standards but has typically shown large trade surpluses in recent decades. Nations like Germany and the United Kingdom have medium to high levels of trade by world standards, but Germany had a moderate trade surplus in 2008, while the United Kingdom had a moderate trade deficit. Their trade picture was roughly in balance in the late 1990s. Sweden had a high level of trade and a large trade surplus in 2007, while Mexico had a high level of trade and a moderate trade deficit that same year.

::贸易平衡是与贸易水平分开的单独问题:美国的贸易水平较低,但从1980年代中期到2000年代的多数年份都存在巨大的贸易逆差;日本按世界标准的贸易水平较低,但近几十年来通常表现出巨大的贸易顺差;德国和联合王国等国家按世界标准的贸易水平中等到高,但2008年德国的贸易顺差不大,而联合王国的贸易逆差则不大;1990年代后期,它们的贸易情况大致保持平衡;2007年瑞典的贸易水平较高,贸易顺差很大;2007年墨西哥的贸易水平较高,贸易逆差也不大。In short, it is quite possible for nations with a relatively low level of trade, expressed as a percentage of GDP, to have relatively large trade deficits. It is also quite possible for nations with a near balance between exports and imports to worry about the consequences of high levels of trade for the economy. It is not inconsistent to believe that a high level of trade is potentially beneficial to an economy, because of the way it allows nations to play to their comparative advantages, and to also be concerned about any macroeconomic instability caused by a long-term pattern of large trade deficits. The following Clear It Up feature discusses how this sort of dynamic played out in Colonial India.

::简言之,贸易水平相对较低的国家,以国内生产总值的百分比表示,很可能出现相对较高的贸易赤字;出口和进口接近平衡的国家,也很有可能担心贸易水平高对经济的影响;认为高水平的贸易可能有利于经济,因为高水平的贸易使各国能够发挥比较优势,也有可能对长期贸易赤字造成的宏观经济不稳定表示关切;随后的《清一色》特征讨论了这种动态在印度殖民地是如何产生的。Are trade surpluses always beneficial? Considering Colonial India

::贸易顺差是否总是有利可图?India was formally under British rule from 1858 to 1947. During that time, India consistently had trade surpluses with Great Britain. Anyone who believes that trade surpluses are a sign of economic strength and dominance while trade deficits are a sign of economic weakness must find this pattern odd, since it would mean that colonial India was successfully dominating and exploiting Great Britain for almost a century—which was not true.

::印度从1858年到1947年正式由英国统治。 在那段时期,印度一直拥有与英国的贸易顺差。 任何认为贸易顺差是经济实力和支配地位的标志而贸易逆差是经济疲软的标志的人都必须发现这种模式很奇怪,因为这将意味着殖民的印度在几乎一个世纪的时间里成功地统治和剥削了英国,而事实并非如此。Instead, India’s trade surpluses with Great Britain meant that each year there was an overall flow of financial capital from India to Great Britain. In India, this flow of financial capital was heavily criticized as the “drain,” and eliminating the drain of financial capital was viewed as one of the many reasons why India would benefit from achieving independence.

::相反,印度与英国的贸易顺差意味着每年都有从印度流向英国的金融资本总流量。 在印度,这种金融资本流量被严厉批评为“人才外流 ” , 消除金融资本外流被视为印度从独立中受益的许多原因之一。Trade deficits can be a good or a bad sign for an economy, and trade surpluses can be a good or a bad sign. Even a trade balance of zero—which just means that a nation is neither a net borrower nor lender in the international economy—can be either a good or bad sign. The fundamental economic question is not whether a nation’s economy is borrowing or lending at all, but whether the particular borrowing or lending in the particular economic conditions of that country makes sense.

::贸易赤字可以是经济的好迹象或坏迹象,贸易盈余也可以是好迹象或坏迹象。 即使是零贸易平衡 — — 这仅仅意味着一国既不是国际经济的净借款人或贷款人 — — 也可能是好迹象或坏迹象。 基本经济问题不在于一国经济是借还是借,而在于该国特定经济状况的特定借款或贷款是否合理。It is interesting to reflect on how public attitudes toward trade deficits and surpluses might change if we could somehow change the labels that people and the news media affix to them. If a trade deficit was called “attracting foreign financial capital”—which accurately describes what a trade deficit means—then trade deficits might look more attractive. Conversely, if a trade surplus were called “shipping financial capital abroad”—which accurately captures what a trade surplus does—then trade surpluses might look less attractive. Either way, the key to understanding trade balances is to understand the relationships between flows of trade and flows of international payments, and what these relationships imply about the causes, benefits, and risks of different kinds of trade balances. The first step along this journey of understanding is to move beyond knee-jerk reactions to terms like “trade surplus,” “trade balance,” and “trade deficit.”

::思考一下公众对于贸易赤字和顺差的态度会如何改变,如果我们能够以某种方式改变人们和新闻媒体对他们的标签。 如果贸易赤字被称作“吸引外国金融资本 ” — —准确地描述了贸易赤字的含义 — — 那么贸易赤字可能显得更具吸引力。 相反,如果贸易顺差被称作“输送国外金融资本 ” — —准确地记录了贸易顺差的作用 — — 那么贸易顺差可能显得不那么有吸引力。 无论是哪种方式,理解贸易平衡与国际支付流动之间的关系的关键是理解贸易流动和国际支付流动之间的关系,以及这些关系对不同贸易平衡的成因、利益和风险意味着什么。 这一理解之旅的第一步是超越“贸易顺差 ” 、 “贸易平衡 ” 和“贸易逆差 ” 等术语。More than Meets the Eye in the Congo

::比在刚果遇到的眼还多Now that you see the big picture, you undoubtedly realize that all of the economic choices you make, such as depositing savings or investing in an international mutual fund, do influence the flow of goods and services as well as the flows of money around the world.

::既然你看到了大局,你无疑意识到 你所做的所有经济选择,例如存款储蓄或投资国际共同基金, 确实影响着货物和服务的流动 以及世界各地的资金的流动。You now know that a trade surplus does not necessarily tell us whether an economy is doing well or not. The Democratic Republic of Congo ran a trade surplus in 2012, as we learned in the beginning of the chapter. Yet its current account balance was –$2.2 billion. However, the return of political stability and the rebuilding in the aftermath of the civil war there has meant a flow of investment and financial capital into the country. In this case, a negative current account balance means the country is being rebuilt—and that is a good thing.

::现在,贸易顺差不一定能告诉我们一个经济体是否运行良好。 正如我们在本章开头所了解的那样,刚果民主共和国在2012年出现了贸易顺差。然而,其经常账户余额为22亿美元。 然而,政治稳定的恢复和内战后重建意味着投资和资金流入该国。 在这种情况下,负经常账户余额意味着该国正在重建 — — 这是好事。There is a difference between the level of a country’s trade and the balance of trade. The level of trade is measured by the percentage of exports out of GDP, or the size of the economy. Small economies that have nearby trading partners and a history of international trade will tend to have higher levels of trade. Larger economies with few nearby trading partners and a limited history of international trade will tend to have lower levels of trade. The level of trade is different from the trade balance. The level of trade depends on a country’s history of trade, its geography, and the size of its economy. A country’s balance of trade is the dollar difference between its exports and imports.

::一国的贸易水平与贸易平衡之间存在差异,贸易水平以出口占GDP的百分比或经济规模来衡量,拥有近邻贸易伙伴和国际贸易历史的小经济体的贸易水平往往较高,贸易水平较低,贸易水平与贸易平衡不同,贸易水平取决于一国的贸易历史、地理和经济规模,贸易平衡是一国进出口之间的美元差额。Trade deficits and trade surpluses are not necessarily good or bad—it depends on the circumstances. Even if a country is borrowing, if that money is invested in productivity-boosting investments it can lead to an improvement in long-term economic growth.

::贸易赤字和贸易顺差不一定是好的或坏的,这取决于情况。 即使一国是借款国,如果这笔钱投资于提高生产力的投资,它也会导致长期经济增长的改善。Introduction to Exchange Rates and International Capital Flows

::介绍汇率和国际资本流动Trade Around the World

::环世界贸易

Is a trade deficit between the United States and the European Union good or bad for the U.S. economy? (Credit: modification of work by Milad Mosapoor/Wikimedia Commons)Is a Stronger Dollar Good for the U.S. Economy?

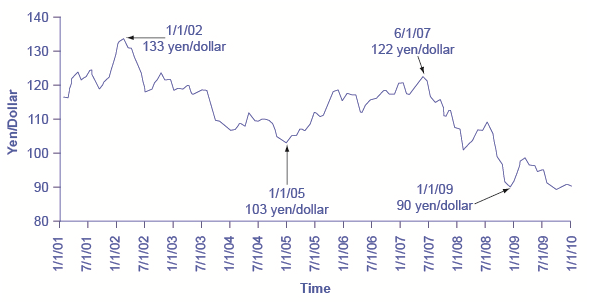

::美元坚挺对美国经济有利吗?From 2002 to 2008, the U.S. dollar lost more than a quarter of its value in foreign currency markets. On January 1, 2002, one dollar was worth 1.11 euros. On April 24, 2008 it hit its lowest point with a dollar being worth 0.64 euros. During this period, the trade deficit between the United States and the European Union grew from a yearly total of approximately –85.7 billion dollars in 2002 to 95.8 billion dollars in 2008. Was this a good thing or a bad thing for the U.S. economy?

::从2002年到2008年,美元在外币市场上损失了超过四分之一的美元价值。 2002年1月1日,一美元值1.11欧元。 2008年4月24日,美元值0.64欧元,创下最低点。 在此期间,美国与欧洲联盟的贸易赤字从2002年的每年总额约857亿美元增长到2008年的958亿美元。 这对美国经济是好事还是坏事?We live in a global world. U.S. consumers buy trillions of dollars worth of imported goods and services each year, not just from the European Union, but from all over the world. U.S. businesses sell trillions of dollars’ worth of exports. U.S. citizens, businesses, and governments invest trillions of dollars abroad every year. Foreign investors, businesses, and governments invest trillions of dollars in the United States each year. Indeed, foreigners are a major buyer of U.S. federal debt. Many people feel that a weaker dollar is bad for America, that it’s an indication of a weak economy. But is it?