4.9 联邦税收制度

章节大纲

-

The Federal Tax System

::联邦税收制度Taxes will always need to be collected so they should meet certain requirements: they should be equitable, simple, and efficient. If these criteria are met, people will generally understand why they are being taxed and may be more receptive to the idea of the tax. There are, however, two principles that revolve around taxes. The first is that the benefit principle of taxation , which is that those who benefit from taxes should pay in proportion to the number of benefits that they receive. The second concept is the ability to pay principle , in which those that can bear the burden of taxes should pay more than those who cannot pay taxes.

::税收总是需要征收,这样它们就应该达到某些要求:它们应该是公平、简单和高效的。 如果达到这些标准,人们一般会理解为什么要征税,并且可能更愿意接受税收概念。 但是,有两个原则围绕着税收,第一个原则是税收的好处原则,即那些从税收中受益的人应该按他们得到的收益数量来支付。 第二个概念是支付能力原则,在这一原则中,那些能够承担税收负担的人应该比那些不能纳税的人支付更多的税。Taxes are proportional, progressive, or regressive depending on the way in which the tax burden changes as income changes. The main source of revenue for the federal government is the individual income tax, while the second largest source is the FICA tax used to pay for Social Security and Medicare. Additional government revenues include excises taxes, gift taxes, customs duties, and user fees.

::税收是按比例、累进或递减的,取决于税收负担随收入变化而变化的方式。 联邦政府的主要收入来源是个人所得税,而第二大来源是用于社会保障和医疗保险的FICA税。 额外的政府收入包括消费税、礼品税、关税和使用费。Universal Generalizations

::普遍化-

Taxes influence the economy by affecting resource allocation, consumer behavior, and the nation’s productivity and growth.

::税收影响经济,影响资源分配、消费者行为和国家生产力和增长。 -

The federal government raises revenue from a variety of taxes.

::联邦政府从各种税收中获取收入。 -

Government economic policies at all levels influence levels of employment, output, and price levels.

::各级政府的经济政策影响就业、产出和价格水平。

Guiding Questions

::问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问-

How do government policies of taxing and spending affect the economy at the national level?

::政府的课税和开支政策在国家一级对经济有何影响? -

What are the positive and negative aspects of taxation?

::税收的积极和消极方面是什么? -

How do taxes contribute to government spending?

::税收如何促进政府开支?

Video: Tax Day 2016

::视频:2016年税务日Source: National Priorities.

Figure 1: 1040 EZ Easy Tax Form

::资料来源:国家优先事项,图1:1040 EZ轻松税表Every year, in the middle of April, U.S. citizens and residents are required to file an income tax form. The preceding f igure shows the 1040EZ tax form, which is the simplest of all these tax forms. For the majority of us, this is one of the most direct pieces of contact that we have with the government. Based on the declarations we file, we are required to pay taxes on the income we have earned over the year. These tax revenues are used to finance a wide variety of government purchases of goods and services and transfers to households and firms. Of course, income taxes are not unique to the United States; most other countries require their residents to complete a similar kind of form.

::每年4月中旬,美国公民和居民都必须提交所得税表。上图显示的是1040EZ税表,这是所有这些税表中最简单的表格。对大多数人来说,这是我们与政府最直接的接触之一。根据我们申报的申报,我们被要求对一年来我们所得收入纳税。这些税收收入被用来资助政府购买各种商品和服务,以及向家庭和公司转移资金。 当然,所得税并非美国独有的;其他大多数国家要求其居民填写类似表格。From the perspective of a household or a firm, the tax form is a statement of financial responsibility. From the viewpoint of the government, the 1040 tax form is an instrument of fiscal policy. The 1040 form is based on the U.S. tax code. Changes in that code can have profound effects on the economy—both in the short-run and in the long-run.

::从家庭或公司的角度来看,税收形式是一份财务责任声明。从政府的角度来看,1040税收形式是财政政策的一种工具。 1040税收形式以美国税法为基础。 该税法的改变可能对经济产生深远影响,无论是短期还是长期影响。In this chapter, we study the various ways in which income taxes affect the economy. An understanding of taxes is critical for policymakers who devise tax policies and for voters who elect them. Tax policies are often controversial, in large part because they affect the economy in several different ways. For example, in the 2004 and 2008 U.S. presidential campaigns, one of the most contentious economic policy issues was an income tax cut that President George W. Bush had initiated in his first term and that the Republican Party wished to make permanent. That issue returned to the forefront of political discussion in 2010, when these tax cuts were renewed.

::在本章中,我们研究了所得税影响经济的各种方式。对税收的理解对于制定税收政策的决策者和选举这些政策的选民来说至关重要。 税收政策往往具有争议性,这在很大程度上是因为它们以不同的方式影响经济。 比如,在2004年和2008年美国总统竞选中,最有争议的经济政策问题之一是乔治·W·布什总统在首任任期内启动的所得税削减,以及共和党希望永久化。 2010年,当这些减税重新生效时,这一问题又回到了政治讨论的前沿。Politicians have argued about such matters since the country was founded. Should the government ensure it has enough tax revenue to balance its budget? How should we raise the revenues to pay for our government programs? What is the appropriate tax on the income received by individuals and corporations? Fiscal policy questions like these are debated in the United States and other countries throughout the world. They are tough questions for politicians and economists alike.

::政治家们自国家成立以来就一直在争论这些问题。 政府是否应该确保有足够的税收来平衡预算? 我们应该如何提高收入来支付政府方案? 个人和公司收到的收入的适当税是什么? 此类财政政策问题在美国和全世界其他国家都有争议。 政治家和经济学家都面临棘手的问题。Politicians focus largely on who wins and loses—which groups will bear the burden of taxes and receive the benefits of government spending and transfers? They do so for political reasons and because one goal of a tax system is to redistribute income. Economists emphasize something rather different. Economists know that taxes are necessary to finance government expenditures. At the same time, they know that taxes can have the negative effect of distorting people’s decisions and lead to inefficiency. Hence economists focus on designing a tax system that achieves its goals of raising revenue and redistributing income, without distorting the decisions of individuals and firms too much.

::政客们主要关注谁赢谁输谁输 — — 哪些群体将承担税收负担,并从政府支出和转移中获益?他们这样做是出于政治原因,因为税收制度的目标之一是重新分配收入。 经济学家们强调了相当不同的东西。 经济学家们知道税收是资助政府支出所必须的。 与此同时,他们知道税收可能会产生扭曲人民决策并导致效率低下的负面影响。 因此经济学家们侧重于设计一个能够实现增加收入和重新分配收入目标的税收体系,而不会扭曲个人和企业的决定。In addition, macroeconomists have observed that taxes significantly affect overall economic performance, as measured by variables such as real gross domestic product (real GDP) growth or the unemployment rate. The government can use changes in taxes as a means of influencing aggregate spending in the economy. In the United States, the federal government has often changed income taxes to affect overall economic performance. In this chapter, we examine two examples: the tax policies of the Kennedy administration of 1960–63 and the Reagan administration of 1980–88.

::此外,宏观经济学家也观察到,税收对总体经济表现有重大影响,以实际国内生产总值(GDP)实际增长或失业率等变量来衡量。 政府可以将税收变化作为影响经济总开支的一种手段。 在美国,联邦政府经常改变所得税以影响总体经济表现。 在本章中,我们考察了两个例子:1960-1963年肯尼迪政府的税收政策和1980-88年里根政府的税收政策。Our discussion of the Kennedy tax cut experience highlights the way in which variations in income taxes are used to help stabilize the macroeconomy. We use the Reagan tax cuts of the early 1980s to explore the growth implications of income taxes, which are often called “supply-side effects.”

::我们关于肯尼迪减税经验的讨论凸显了使用所得税差异帮助稳定宏观经济的方式。 我们利用1980年代初的里根减税来探索所得税对增长的影响,这通常被称为“供应方效应 ” 。Road Map

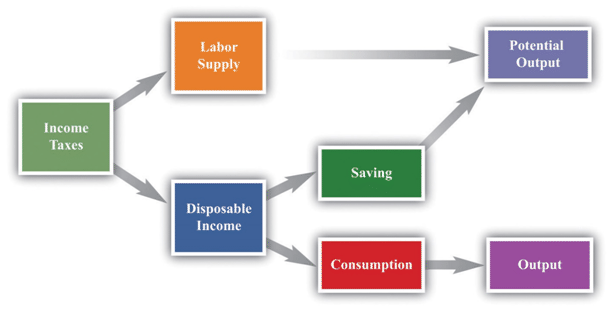

::路线图路线图Our approach to understanding the effects of income taxes on the economy is summarized in Figure 2 "Macroeconomic Effects of Tax Policy":

::图2“税收政策对宏观经济的影响”概述了我们了解所得税对经济影响的方法:• Taxes affect consumption and hence aggregate expenditure and output.

::• 税收影响消费,从而影响总支出和产出。• Taxes affect saving and hence the capital stock and output.

::• 税收影响储蓄,从而影响资本存量和产出。• Taxes affect labor supply and hence output.

::• 税收影响劳动力供应,从而影响产出。Figure 2: Macroeconomic Effects of Tax Policy

::图2 税收政策的宏观经济影响Any change in the income tax regime affects both the spending and the supply sides of the economy. Our reason for thinking separately about the Kennedy and Reagan tax experiments is to isolate the spending effects and the supply effects. Once you understand these different channels, you will be equipped to evaluate other tax policies, such as those adopted later by President George W. Bush. Finally, the figure reveals that the choice between consumption and saving and the choice between work and leisure are at the heart of our analysis.

::所得税制度的任何变化都会影响经济的支出和经济的供应方。 我们对肯尼迪和里根的税务实验分别进行思考的理由,是孤立支出效应和供应效应。 一旦你了解这些不同的渠道,你将有能力评估其他税收政策,比如乔治·布什总统后来通过的政策。 最后,这个数字表明消费和储蓄的选择以及工作和休闲的选择是我们分析的核心。Basic Concepts of Taxation

::税收基本概念Before delving into the details of President Kennedy’s tax policy, we review the basics of personal income taxation. This review is not only helpful for your study of economics, but also may be useful when you have to fill out your own income tax form. Even a quick glance at the 1040EZ form in suggests that taxes are a very complex topic. Indeed, the US federal tax code governing income taxes alone runs to thousands of pages. The taxes that you pay depend on your adjusted gross income (line 4), which is the income you receive from a variety of sources (the main components noted on the return are wages, interest income, and unemployment compensation). There is also a “standard deduction” and an “exemption” (line 5)—for a single person in 2010, these totaled $9,350. For the EZ form, your taxable income is given as the following:

::在详细研究肯尼迪总统的税收政策之前,我们先审视个人所得税的基本内容。 本次审查不仅有助于您对经济学的研究,而且在您填写自己的所得税表格时也会有所帮助。 即使简单看一下1040EZ表格,也表明税收是一个非常复杂的话题。 事实上,美国联邦所得税税法只有数千页。 您缴纳的税收取决于您调整后的毛收入(第4行 ) , 也就是您从各种来源获得的收入(回报的主要部分是工资、利息收入和失业补偿 ) 。 还有一个“标准扣减”和“豁免 ” ( 第5行 ) — — 2010年对一个人来说,总计为 9 350美元。 对于经济区,您应纳税的收入如下:- t axable income = adjusted gross income − (deduction + exemption).

If your financial situation is very simple, you can file this EZ form. However, if you receive income from other sources (such as dividends on stocks), or if you wish to “itemize” your deductions (for payments of interest on home mortgages, dependent children, property taxes, and so forth), you have to file a more complicated form, often with several other forms containing supplementary information. Thus the calculation of adjusted gross income and deductions can be quite complex. For all individuals, however, the basic relationship still holds:

::如果您的财政状况非常简单,您可以填入此 EZ 表格。但是,如果您从其他来源(如股票股息)获得收入,或者如果您希望“逐项”扣除(对于住房抵押贷款、受抚养子女、财产税等的利息支付),您必须填入一个更为复杂的表格,通常用其他几种表格提供补充信息。因此,调整后的毛收入和扣减的计算可能相当复杂。然而,对于所有个人来说,基本关系仍然存在:- t axable income = adjusted gross income − (deductions and exemptions).

Once you know your taxable income, there are then different tax rates for different income levels. Even this is not quite the whole story. There are various tax credits for which some individuals are eligible, and there is also something called the alternative minimum tax, which must be calculated.

::一旦您知道自己的应纳税收入,那么不同收入水平的税率就会不同。即使这并非全部情况。 有一些个人有资格享受各种税收抵免,还有一种叫作替代性最低税的办法,必须计算。Marginal and Average Tax Rates

::边际税率和平均税率From the perspective of macroeconomics, this complexity is daunting, particularly when we remember that the details of the tax system vary from country to country and year to year. The income tax is evidently not a simple thing that can be incorporated in a straightforward way into our frameworks. We cannot hope to incorporate all these features of the tax code into our theory without getting completely bogged down in the details. If we are going to make sense of how taxes affect consumption behavior, we must leave out most of these complicating elements. The challenge for economists is to decide which features of the tax system are critical for our analysis and which are peripheral and can be safely ignored.

::从宏观经济的角度来看,这种复杂性是令人生畏的,特别是当我们记得税收制度的细节因国而异,年年而异时更是如此。所得税显然不是一件简单的事情,可以直接纳入我们的框架。我们不能指望把税法的所有这些特点都纳入我们的理论,而不在细节中完全被淡化。如果我们要了解税收如何影响消费行为,我们必须把这些复杂因素中的大多数都排除在外。经济学家面临的挑战是决定税收制度的哪些特征对我们的分析至关重要,哪些是外围的,可以安全地忽略。

One noteworthy feature of the income tax system is that not everyone pays the same amount of tax. shows the income tax schedule for the year 2010 for a single taxpayer. There are other schedules for members of a household filing jointly. These and related tables are available from “Forms and Publications,” Internal Revenue Service, accessed September 20, 2011, . It indicates how much tax a must be paid for a given level of taxable income.

::所得税制度的一个值得注意的特征是,并非每个人都缴纳相同数额的税。 它显示的是2010年单一纳税人的所得税表。 还有一些关于家庭成员共同申报的其他时间表。 这些表格和相关表格可从2011年9月20日查阅的“表格和出版物 ” 国内税收服务处查阅 。 它表明一定水平的应纳税收入必须缴纳多少税。-

Table 1 Revised 2010 Tax Rate Schedules

::表1 2010年订正税率表

If Taxable Income

::如果应征税收入The Tax Is Then

::税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税 税Is Over (in US$)

::超过(以美元计)But Not Over (in US$)

::而不是超过(以美元计)This Amount (in US$)

::这一数额(美元)Plus This (%)

::加上这个(%)Of the Excess Over (in US$)

::超过部分(以美元计)0

8,375

0

10

0

8,375

34,000

837.50

15

8,375

34,000

82.400

4,681.25

25

34,000

82.400

171,850

16,781.25

28

82.400

171,850

373,650

41,827.25

33

171,850

373,650

—

108,421.25

35

373,650

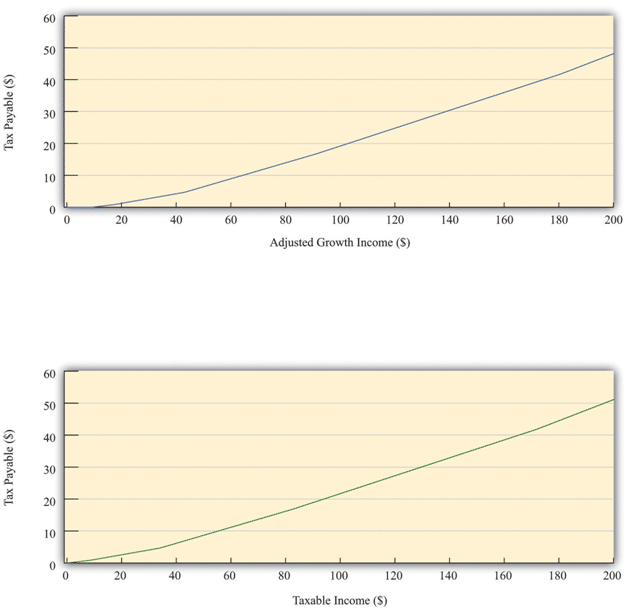

To use this table, you must first find your taxable income. Suppose it is $20,000. Your tax is then determined from the second row of the table. You would owe 837.50 + 0.15 × (20,000 − 8,375), which is $2,581.25. Figure 3 shows the relationship between taxes and income implicit in the tax schedule summarized in Table 1 "Revised 2010 Tax Rate Schedules".

::要使用这个表格,您必须首先找到您的应纳税收入。假设是20,000美元。然后从表格第二行确定您的税收。您将欠837.50+0.15x(20,000 - 8,375美元),即2,581.25美元。图3显示了“2010年订正税率表”表1汇总的税收表所隐含的税收和收入之间的关系。This figure shows the amount of tax you must pay given your adjusted gross income (upper panel) and your taxable income (lower panel). We see two key facts:

::下图显示了根据调整后的总收入(上表)和应纳税收入(下表)你必须缴纳的税额。As an individual’s income increases, he or she pays more in tax (the line slopes upward).

::随着个人收入的增加,他或她的纳税额会增加(线坡向上)。As an individual’s income increases, he or she pays a larger fraction of additional income in tax (the line becomes steeper at higher levels of income).

::随着个人收入的增加,他或她支付更多的税收收入(收入水平越高,这一税项越高)。This leads us to two ways to think about the tax schedule a household faces.

::这让我们想到两种方式来思考家庭面临的税收表。Figure 4: Amount of Tax Owed by Individuals

::图4:个人所欠税款数额The figure shows the amount of tax owed by a single individual in the United States who takes the “standard deduction.” The upper panel has adjusted gross income on the horizontal axis, whereas the lower panel has taxable income on the horizontal axis.

As shown in , there were six different tax rates in effect in 2010, ranging from 10 percent for low-income individuals to 35 percent for high-income individuals. The tax rates in the fourth column are the marginal tax rates since they represent the tax rate paid on marginal (that is, additional) income. Thus higher income households pay higher marginal tax rates. The marginal tax rate can be seen graphically as the slope of the line in 4.

::如前文所示,2010年实行六种不同的税率,从低收入个人10%到高收入个人35%不等,第四栏的税率是边际税率,因为它们代表了对边际(即额外)收入支付的税率,因此,高收入家庭支付较高的边际税率。边际税率可以图形化地看成是4中线的斜坡。We are often interested in knowing what fraction of an individual’s income goes to taxes. This is called the average tax rate. Returning to the example we calculated earlier, if you have an income of $20,000 and thus pay taxes of $2,581.25, your average tax rate is equal to 2,581.2520,000=0.129, or 12.9 percent. The marginal tax rate of 15 percent is greater than the average tax rate of 12.9 percent. There is a difference between the tax you pay on average and the tax rate charged on the last dollar of income. The average tax rate can also be given a graphical interpretation. It is the slope of a line from the origin to the point on the graph.

::我们常常想知道个人收入的哪一部分归税。 这被称为平均税率。 回到我们早先计算的例子,如果你的收入为20,000美元,因此缴纳2,581. 2520,000美元,平均税率等于2,581. 2520,000美元=0. 129,或12.9%。 15%的边际税率高于12.9 % 的平均税率。 你平均支付的税率和对最后1美元收入征收的税率之间存在差异。 平均税率也可以用图形来解释。 这是从来源到图上点的一条线的斜坡。Leaving aside the details of exemptions and deductions, the essence of the income tax code is captured in the table and figures we have just presented. Even these, however, are quite complicated. We want to build income taxes into our framework of the economy, so it would be nice if we could decide on a simpler way to represent the tax code. The art of economics lies in deciding how to take something complicated, like the U.S. income tax code, and represent it in as simple a way as possible while still retaining the features that matter to the problem under discussion .

::撇开豁免和减免的细节不谈,所得税法的精髓已经体现在我们刚刚提出的表格和数字中。 但是,即使这些也相当复杂。 我们想将所得税纳入经济框架,因此,如果我们能决定一个更简单的方式来代表税法,那将是件好事。 经济学艺术在于决定如何采取复杂的事情,比如美国所得税法,并以尽可能简单的方式代表它,同时保留与所讨论的问题相关的特征。Looking at 4, we can see that the relationship between taxes paid and taxable income looks approximately like a straight line. It is not exactly a straight line because it becomes steeper as marginal tax rates increase. For our purposes in this chapter, however, it is a reasonable simplification to represent this relationship as a line—that is, to suppose that the marginal tax rate is constant.

::从4点看,我们可以看到,已付税和应纳税收入之间的关系看起来大致是一条直线。 这并不是一条直线,因为它随着边际税率的上升而变得更为陡峭。 但是,为了我们在本章中的目的,将这种关系作为一条直线(即假设边际税率是不变的 ) , 是一个合理的简化。In addition, we ignore the standard deduction and exemption. That is, we suppose that people start paying taxes on their very first dollar of income. Thus we suppose that

::此外,我们忽略了标准扣减和免税标准。 也就是说,我们假设人们开始对其收入的第一美元纳税。 因此,我们假设人们开始对其收入的第一美元纳税。- taxes paid = tax rate × income .

Representing the tax schedule this way is fine if we want to examine the economy as a whole and are not particularly concerned with the way in which taxes affect different households. We use this simplified model of the tax system at various times in this chapter.

::以这种方式代表税收表是好的,如果我们想对整个经济进行审查,而不特别关注税收如何影响不同家庭,我们在本章中多次使用这一简化的税收制度模式。Effects of Changes in Tax Rates

::税率变动的影响We can use this simple model of the tax system to see how a change in the income tax rate affects both individuals and the economy as a whole. Suppose there is a cut in the tax rate. Since taxes paid = tax rate × income, the immediate impact is to reduce the amount of taxes households pay: for a given income, a reduction in the tax rate reduces taxes paid. This means that disposable income, which is the income left over after paying taxes and receiving transfers, increases.

::我们可以使用这一简单的税收制度模式来观察所得税率变化如何影响个人和整个经济。 如果税率被削减的话。 由于纳税额=税率x收入,直接的影响是降低家庭纳税额:对于特定收入来说,降低税率会降低所付税额。 这意味着可支配收入,也就是纳税和接受转账后留下的收入,会增加。What do households do with the increase in disposable income? A likely answer is that a typical household spends some of this extra income and saves the remainder. If all households follow this pattern, then the increased spending by each household translates into larger consumption in the aggregate economy. At this point, the power of the circular flow of income will take over, and the level of income and output in the economy will increase even further.

::家庭对可支配收入的增加能做什么? 可能答案是典型的家庭将部分额外收入花掉并节省剩余收入。 如果所有家庭都遵循这一模式,那么每个家庭增加的支出将转化为总体经济中更大的消费。 此时,收入循环流动的力量将接管,而经济的收入和产出水平将进一步增加。As the economy expands, the amount of taxes paid starts to increase. In other words, one consequence of a tax cut is that the tax base (income) expands. The ultimate effect of a tax cut on the overall amount of taxes paid depends on both this expansion of the tax base (income) and the reduction of the tax rate.

::随着经济的扩张,纳税额开始增加。 换句话说,减税的一个后果是税基(收入)的扩大。 减税对所付税总额的最终效果取决于税基(收入)的扩大和税率的降低。Taxes and Income Distribution

::税收和收入分配The effects of a tax cut are not the same for everyone. Changes in the tax code effect the distribution of income. If we want to understand such effects, however, it is a mistake to use our simple model of the tax system. We must instead examine how marginal tax rates are different at different levels of income. Suppose that marginal tax rates increase with income, which means that average tax rates increase with income. Higher income households then pay a larger fraction of their income as taxes to the government. As a result, the distribution of income after taxes is more equal than the distribution of income before taxes.

::减税的效果对每个人都不一样。 税法的改变影响收入的分配。 但是,如果我们想了解这种影响,那么,使用我们简单的税制模式是错误的。 我们必须研究不同收入水平的边际税率如何不同。 假设边际税率随收入而增加,这意味着平均税率随收入而增加。 高收入家庭将收入的更大部分作为税收支付给政府。 因此,税后收入的分配比税收前的收入分配更为平等。Imagine that we take two individuals with different levels of income and calculate their tax payments and after-tax income. Suppose that the first individual earns $20,000 per year and the other earns $200,000. shows the amount of tax each pays and their income after taxes, based on the tax schedule from . Notice from the table that the marginal tax of the high-income household is 33 percent, compared with the 15 percent marginal tax of the low-income household. The total tax paid by the high-income individual is $51,116.75, which is almost 20 times the tax paid by the low-income household. Whereas the pre-tax income of the richer household was 10 times greater than that of the poorer household, its after-tax income is 8.5 times greater.

::想象一下我们拿两个收入水平不同的个人来计算他们的纳税和税后收入。 假设第一个个人每年挣20 000美元,另一个个人挣20 000美元。 根据税收表表显示每人纳税和税后收入的数额。 从表中可以看出,高收入家庭的边际税为33%,而低收入家庭的边际税为15%。 高收入个人缴纳的税总额为51116.75美元,几乎是低收入家庭纳税税的20倍。 富裕家庭的税前收入比较贫穷家庭的税前收入高10倍,但其税后收入则高出8.5倍。Table 2 The Redistributive Effects of Taxation (in US$)

::表2 税收的再分配影响(美元)Income Tax Paid Income after Taxes 20,000 2,581.25 17,418.75 200,000 51,116.75 148,883.25 This example shows that the tax code redistributes income from high-income to low-income households. Furthermore, the redistribution does not necessarily stop here. We have not said anything about what the government does with the tax revenues it receives. If the government transfers all those revenues to low-income households, then the combined redistributive effect of taxes and transfers is even stronger.

::这个例子表明税法将收入从高收入家庭重新分配到低收入家庭。 此外,再分配并不一定就停在这里。 我们没有说政府用税收收入做什么。 如果政府将所有这些收入都转移给低收入家庭,那么税收和转拨的合并再分配效果就更加强大了。When we talk about the effects of taxes on labor supply and disposable income, keep in mind that the size of these effects is different for households at different levels of income. These varying effects matter for the politics of tax cuts because lawmakers pay close attention to which income groups are affected by tax policy.

::当我们谈论税收对劳动力供应和可支配收入的影响时,要记住这些影响的规模对于收入水平不同的家庭来说是不同的。 这些影响对于减税政治很重要,因为立法者密切关注哪些收入群体受到税收政策的影响。Taxation

::税务税There are two main categories of taxes: those collected by the federal government and those collected by state and local governments. What percentage is collected and what that revenue is used for varies greatly. The following sections will briefly explain the taxation system in the United States.

::税收分为两大类:联邦政府征收的税以及州和地方政府征收的税。 征收的百分比和收入用于何种税收差别很大。 以下各节将简要解释美国税收制度。Federal Taxes

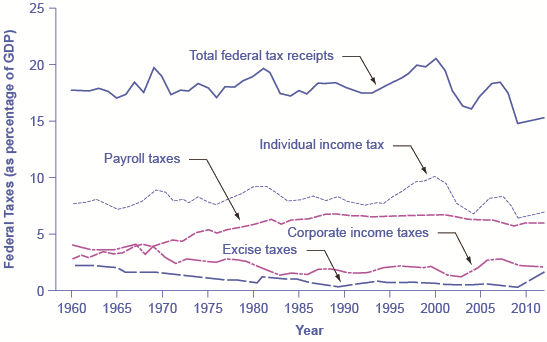

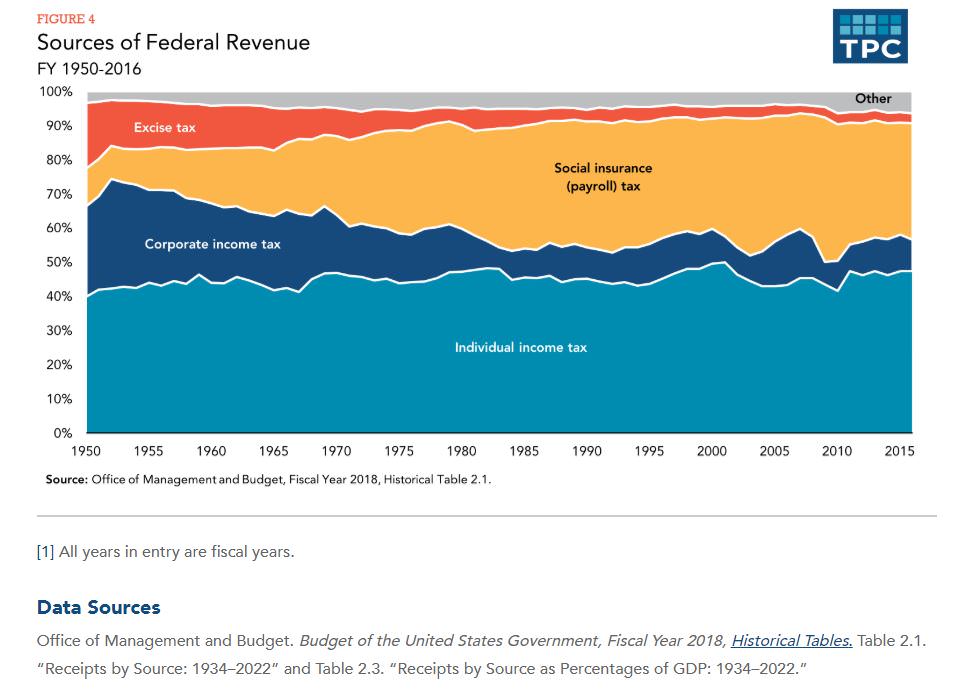

::联邦税Just as many Americans erroneously think that federal spending has grown considerably, many also believe that taxes have increased substantially. The top line of 5 shows total federal taxes as a share of GDP since 1960. Although the line rises and falls, it typically remains within the range of 17% to 20% of GDP, except for 2009, when taxes fell substantially below this level, due to a recession.

::正如许多美国人错误地认为联邦支出已经大幅增长,许多人也认为税收已经大幅增长。 上列5显示自1960年以来联邦税收总额占国内生产总值的比例。 尽管该税额在上升和下降,但通常仍保持在GDP的17%至20%之间,但2009年除外,当时由于经济衰退,税收大大低于这一水平。- Figure 5: Federal Taxes, 1960–2012

Federal tax revenues have been about 17–20% of GDP during most periods in recent decades. The primary sources of federal taxes are individual income taxes and the payroll taxes that finance Social Security and Medicare. Corporate income taxes, excise taxes, and other taxes provide smaller shares of revenue. (Source: Economic Report of the President, Tables B-81 and B-1)

5 also shows the patterns of taxation for the main categories of taxes levied by the federal government: personal income taxes, payroll taxes, corporate income taxes, and excise taxes. When most people think of taxes levied by the federal government, the first tax that comes to mind is the individual income tax that is due every year on April 15 (or the first business day after). The personal income tax is the largest single source of federal government revenue, but it still represents less than half of federal tax revenue.

::5 也显示了联邦政府征收的主要税种的税收模式:个人所得税、工资税、公司所得税和消费税。 当大多数人想到联邦政府征收的税时,首先想到的个人所得税是每年4月15日(或次日第一个营业日)应缴纳的个人所得税。 个人所得税是联邦政府收入的最大单一来源,但仍占联邦税收收入的不到一半。The second largest source of federal revenue is the payroll tax, which provides funds for Social Security and Medicare. Payroll taxes have increased steadily over time. Together, the personal income tax and the payroll tax accounted for about 84% of federal tax revenues in 2012. Although personal income tax revenues account for more total revenue than the payroll tax, nearly three-quarters of households pay more in payroll taxes than in income taxes.

::联邦收入的第二大来源是工资税,它为社会保障和医疗保险提供资金,工资税随着时间推移稳步增加。 2012年,个人所得税和工资税共占联邦税收收入的84%左右,尽管个人所得税收入总额高于工资税,但近四分之三的家庭缴纳的工资税比所得税多。The income tax is a progressive tax, which means that the tax rates increase as a household’s income increases. Taxes also vary with marital status, family size, and other factors. The marginal tax rates (the tax that must be paid on all yearly income) for a single taxpayer range from 10% to 35%, depending on income, as the following Clear It Up feature explains.

::所得税是一种累进税,这意味着税率随着家庭收入的增加而上升。 税收也随婚姻状况、家庭规模和其他因素而变化。 单一个纳税人的边际税率(所有年收入都必须缴纳的税)在10%至35 % 之间,这取决于收入,正如以下“清清楚楚 ” ( Clear It Up)特征所解释的那样。How does the Marginal Rate Work?

::边际税率工作如何?Suppose that a single taxpayer’s income is $35,000 per year. Also suppose that income from $0 to $9,075 is taxed at 10%, income from $9,075 to $36,900 is taxed at 15%, and, finally, income from $36,900 and beyond is taxed at 25%. Since this person earns $35,000, their marginal tax rate is 15%.

::假设一个纳税人的收入是每年35,000美元。 假设一个纳税人的收入是每年35,000美元。 此外,假设从0美元到9,075美元的收入按10%的税率征税,从9,075美元到36,900美元的收入按15%的税率征税,最后,从36,900美元及以后的收入按25%的税率征税。 由于这个人的收入是35,000美元,他们的边际税率是15 % 。The key fact here is that the federal income tax is designed so tax rates increase up to a certain level as income increases. The payroll taxes that support Social Security and Medicare are designed in a different way. First, the payroll taxes for Social Security are imposed at a rate of 12.4% up to a certain wage limit, set at $117,900 in 2014. Medicare, on the other hand, pays for elderly healthcare and is fixed at 2.9%, with no upper ceiling.

::这里的关键事实是,联邦所得税的设计是为了使税率随着收入的增加提高到一定水平。支持社会保障和医疗保险的发薪税是以一种不同的方式设计的。 首先,社会保障工资税的税率为12.4%,最高为一定的工资限额,2014年的定值为117,900美元。 另一方面,医疗保险支付老年保健费用,固定为2.9%,没有上限。In both cases, the employer and the employee split the payroll taxes. An employee only sees 6.2% deducted from his paycheck for Social Security, and 1.45% from Medicare. However, as economists are quick to point out, the employer’s half of the taxes are probably passed along to the employees in the form of lower wages, so in reality, the worker pays all of the payroll taxes.

::在这两种情况下,雇主和雇员均分工资税。 雇员只看到从社会保障工资中扣除6.2%,从医疗保险工资中扣除1.45%。 然而,正如经济学家很快指出的,雇主的一半税收可能以较低工资的形式传给雇员,因此实际上,工人支付所有工资税。The Medicare payroll tax is also called a proportional tax; that is, a flat percentage of all wages earned. The Social Security payroll tax is proportional up to the wage limit, but above that level it becomes a regressive tax, meaning that people with higher incomes pay a smaller share of their income in tax.

::医疗保险工资税也被称为比例税,即所有工资的固定百分比。 社会保障工资税与工资限额成正比,但高于工资限额则成为递减税,这意味着高收入者缴纳的税收收入份额较小。The third-largest source of federal tax revenue, as shown in 5 is the corporate income tax. The common name for corporate income is “profits.” Over time, corporate income tax receipts have declined as a share of GDP, from about 4% in the 1960s to an average of 1% to 2% of GDP in the first decade of the 2000s.

::联邦税收收入的第三大来源是公司所得税。 公司收入的共同名称是“利润 ” 。 随着时间的推移,公司所得税收入在GDP中所占的份额从1960年代的大约4%下降到2000年代第一个十年的1%到2%。The federal government has a few other, smaller sources of revenue. It imposes an excise tax—that is, a tax on a particular good—on gasoline, tobacco, and alcohol. As a share of GDP, the amount collected by these taxes has stayed nearly constant over time, from about 2% of GDP in the 1960s to roughly 3% by 2012, according to the nonpartisan Congressional Budget Office. The government also imposes an estate and gift tax on people who pass large amounts of assets to the next generation—either after death or during life in the form of gifts. These estate and gift taxes collected about 0.2% of GDP in the first decade of the 2000s. By a quirk of legislation, the estate and gift tax was repealed in 2010, but reinstated in 2011. Other federal taxes, which are also relatively small in magnitude, include tariffs collected on imported goods and charges for inspections of goods entering the country.

::联邦政府还有另外几个较小的收入来源,即对汽油、烟草和酒精等特定商品征收消费税,作为国内生产总值的一部分,从1960年代占国内生产总值的2%左右到2012年的3%左右,这些税收在一段时间内几乎保持不变。据无党派的国会预算办公室称,联邦政府还对在死亡后或一生中以赠品形式将大量资产传给下一代的人征收遗产税和礼品税。这些遗产税和礼品税在2000年代头十年征收了约0.2%的国内生产总值。根据立法,2010年废除了遗产税和礼品税,但2011年又恢复了这一税。 其他联邦税收规模相对较小,包括对进口货物征收的关税和对进入该国的货物进行检查的收费。The two main federal taxes are individual income taxes and payroll taxes that provide funds for Social Security and Medicare; these taxes together account for more than 80% of federal revenues. Other federal taxes include the corporate income tax, excise taxes on alcohol, gasoline and tobacco, and the estate and gift tax. A progressive tax is one, like the federal income tax, where those with higher incomes pay a higher share of taxes out of their income than those with lower incomes. A proportional tax is one, like the payroll tax for Medicare, where everyone pays the same share of taxes regardless of income level. A regressive tax is one, like the payroll tax (above a certain threshold) that supports Social Security, where those with high income pay a lower share of income in taxes than those with lower incomes.

::两种主要的联邦税是个人所得税和工资税,它们为社会保障和医疗保险提供资金;这些税加在一起占联邦收入的80%以上;其他联邦税包括公司所得税、酒精、汽油和烟草消费税以及不动产和礼品税。 累进税与联邦所得税一样,是累进税,收入较高的人从收入中支付比收入较低的人更高的税收份额。 比例税与Medicare的工资税一样,人人支付相同的税收份额,而不论收入水平如何。 累进税是一种累进税,如支持社会保障的工资税(高于一定阈值 ) , 高收入的人支付较低的税收收入份额。Sources of Federal Revenue

"Government revenue amounted to $1.3 trillion in the mid-1980s, and then breached $2 trillion in 1992 just after the recession of 1990-91. In the 1990s revenue increases accelerated, reaching $3.2 trillion in 1998 and reaching a peak of $3.7 trillion in 2000. But in the 2000s, with the dot-com crash and 9/11, government revenue declined hitting $3.3 trillion in 2002 before resuming its increase again. Revenue reached above $4 trillion in 2005 and $5 trillion in 2007. Then came the Crash of 2008 and government revenue nose-dived down to $3.6 trillion in 2009. After a few years of catch-up, revenue is expected to hit $6 trillion in 2015." ( retrieved from )

Corporate Income Taxes

::公司所得税Companies that are corporations must pay income taxes on profits earned during the year. Corporate income taxes are considered the third largest category of taxes that the federal government collects. Because a corporation is considered a separate legal entity, they pay taxes based on the amount of profits the company earned. Currently, there are several corporate tax brackets.

::作为公司的公司必须就当年赚取的利润缴纳所得税。 公司所得税被视为联邦政府征收的第三大税。 由于公司被视为一个独立的法律实体,它们根据公司赚取的利润额纳税。 目前,有几个公司税括号。Taxable Income ($)

::应纳税收入(美元)Tax Rate

::税率税率税率税率0 to 50,000

::0至50 00015%

50,000 to 75,000

::50 000至75 000$7,500 + 25% Of the amount over 50,000

::7 500美元+25%75,000 to 100,000

::75 000至100 000$13,750 + 34% Of the amount over 75,000

::13 750美元+34%100,000 to 335,000

::100 000至335 000人$22,250 + 39% Of the amount over 100,000

::22 250美元+10万以上金额的39%335,000 to 10,000,000

::335 000至10 000 000 000$113,900 + 34% Of the amount over 335,000

::113 900美元+34%,超过335 000美元10,000,000 to 15,000,000

::10 000 000至15 000 000至15 000 000$3,400,000 + 35% Of the amount over 10,000,000

::3 400 000美元+35%15,000,000 to 18,333,333

::15 000 000至18 333 333$5,150,000 + 38% Of the amount over 15,000,000

::5 150 000美元+38%18,333,333 and up

::18,333,333,333及以上35%

This rate structure produces a flat 34% tax rate on incomes from $335,000 to $10,000,000, gradually increasing to a flat rate of 35% on incomes above $18,333,333. retrieved from

::其他联邦税

::消费税是对汽油和酒类等某些物品的制造或销售征税,美国《宪法》自批准以来就允许征收消费税。Excise Tax Examples

::税务税实例

::消费税被认为是“递减性”税,因为低收入家庭往往将收入的较大部分花在这些类型的商品上,因此发现这比收入较高的家庭更是一种负担。 国会颁布并随后退让了1991年消费税,又称“奢侈税 ” 。 税收不受欢迎,没有提高国会预计的收入,因此在2002年逐步取消。 阅读更多这方面的信息,请访问网站 — — http://www.wsj.com/articles/SB10418077279794664。to pay a tax. In addition, a gift tax is a tax on donations of money or wealth from one person to another. This tax is to

::联邦税的另一个例子是财产税。这种税是个人死亡时对财产转让征税的一种税。值低于国家最高税额的遗产,不要求继承财产的人纳税。此外,礼品税是个人捐钱或向他人捐财富的税。这项税由赠金赠与人支付。设立这项税的原因是为了防止富人通过在个人死亡前交出其财富或财产而避税。在目前的所有税项中,由政府关税征收的遗产和礼品税是政府关税征收的最小的百分比,这是由从另一个国家带货的人或公司缴纳的联邦税。《美国宪法》赋予国会决定哪些外国产品要征税以及这些产品要缴纳多少税的能力。虽然税收从很低到50 % 不等,但今天的税收比例非常小,比100年前要低。 杂项费或用户费是用于使用国家公园等良好设施的费用。从Regan管理国会期间开始使用这些收费来提高税收的比额相当大。“用户”一词是“税收比税额”。“用户”一词是“税额”。Video: Calculating Federal Taxes and Take Home Pay

::录像:计算联邦税税和拿回家的工资Key Takeaways

::密钥外出The marginal tax rate is the rate paid on an additional dollar of income, and the average tax rate is the ratio of taxes paid to income.

::边际税率是额外收入美元所付税率,平均税率是所付税款与收入之比。When the marginal tax rate is increasing in income, then the tax system redistributes from richer households to poorer households. In this case, after-tax income is more equal than income before taxes are paid.

::当边际税率在增加收入时,税收制度就会从较富裕的家庭向较贫穷的家庭重新分配。 在这种情况下,税后收入比纳税前的收入更平等。Answer the self check questions below to monitor your understanding of the concepts in this section.

::回答下面的自我核对问题,以监测你对本节概念的理解。Self Check Questions

::自查问题1. What is the 16th Amendment?

::1. 第16项修正案是什么?2. Why does the federal government levy a tax?

::2. 联邦政府为何征税?3. What is the payroll withholding system?

::3. 什么是工资单预扣制度?4. Explain the concept of a "tax return."

::4. 解释“税收回报”的概念。5. What is FICA?

::5. 什么是亚洲信任论坛?6. What is a corporate income tax?

::6. 什么是公司所得税?7. List other federal taxes.

::7. 列出其他联邦税。 -

Taxes influence the economy by affecting resource allocation, consumer behavior, and the nation’s productivity and growth.