4.14 赤字、盈余和国民债务

章节大纲

-

Deficits, Surpluses, and the National Debt

::赤字、盈余和国民债务The government projects its future revenues and expenditures, however, it depends on how strong the economy is and whether or not there will be economic growth. A projected surplus means that the government has collected more revenues than it will spend (expenditures) on programs. A projected deficit means that the government will collect less taxes (revenues) than it has estimated it will need to spend to maintain specific programs.

::然而,政府预测未来收入和支出取决于经济的强劲程度,以及是否会出现经济增长。 预测盈余意味着政府收入超过用于方案的支出(支出 ) 。 预计赤字意味着政府税收(收入)将比维持具体方案所需的支出少。Universal Generalizations

::普遍化-

Deficit spending has helped to create the national debt.

::赤字支出帮助创造了国民债务。 -

The federal government’s decision to maintain its economic policies related to the economic goals of economic growth, stability and full employment has impacted annual federal budgets.

::联邦政府决定维持与经济增长、稳定和充分就业等经济目标有关的经济政策,这对联邦年度预算产生了影响。

Guiding Questions

::问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问 问-

If the federal government wanted to lower the national debt, what would it have to do?

::如果联邦政府想降低国民债务,它会怎么做? -

Why is deficit spending sometimes considered necessary?

::为什么有时认为赤字开支是必要的?

Video: WWII Vet Offers Emotional Warning about Growing National Debt

::影片:WWWII Vet 提供对不断增长的国民债务的情感警告Deficit Spending

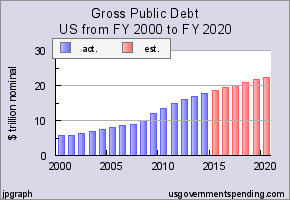

::赤字支出Since the end of World War II, the federal budget has been characterized by an enormous amount of deficit spending. Deficit spending is when the government spends more money than it has collected in revenues (taxes). Sometimes deficit spending by the government is necessary and planned, other times it is forced to do this because of unexpected developments and unforeseen events at home or abroad. When the federal government runs a deficit , it has to finance its spending with money it will need to borrow. Borrowing funds can come from citizens or foreign countries. Treasury bonds and other forms of government debt are sold to raise these necessary funds. If we add up all of the debt, or federal debt, it is the amount of money borrowed from investors to finance the government's current deficit spending.

::自二战结束以来,联邦预算的特点是巨额赤字支出;赤字支出是指政府在收入(税收)方面的支出超过其收入(税收),有时政府赤字支出是必要的和计划性的,有时由于意外发展和国内外意外事件而被迫这样做。当联邦政府出现赤字时,它必须用需要借来的钱来为其支出提供资金。借款可以来自公民或外国。国债和其他形式的政府债务被出售来筹集这些必要的资金。如果我们把所有债务或联邦债务加在一起,它就是从投资者那里借来的钱来为政府当前的赤字支出提供资金。As of July 2015 the national debt stands at $18,581,234,768,000. At the end of FY 2015 the total government debt in the United States, including federal, state, and local, is expected to be $21.694 trillion.

::截至2015年7月,国民债务为18 581 234 768 000美元,到2015财政年度末,包括联邦、州和地方在内的美国政府债务总额预计为21.694万亿美元。(Source: )

Some of the debt is money the government owes to itself, or debt held in government trust funds. These funds are special accounts used to fund specific types of expenditures such as Medicare and Social Security. When the government collects the FICA tax from individuals, it invests that money in the trust or government securities until that money is paid out. While this is money the government owes to itself, it is still a significant portion of the debt.

::有些债务是政府欠自己的钱,或者是政府信托基金中的债务。 这些资金是用来资助特定类型的支出的特别账户,如医疗保险和社会保障。 当政府从个人那里收取FICA税时,它将这笔钱投资于信托或政府证券,直到这笔钱付清为止。 虽然这是政府欠自己的钱,但它仍然是债务的一大部分。This debt is a public debt. Because the government owes it to itself, it does not have the same impact as a private debt. A private debt is one that individuals owe to another and therefore it must be paid. For the government, it does not worry about the eventual repayment of the loan because it can simply issue more bonds to cover the outstanding debt. When the government does repay its debt, there is no loss of purchasing power as there is for individuals who gives up some of its purchasing power to pay off their debts. The government simply collects taxes and then redistributes the money to others. The exception of this rule is the debt that is owed to foreigners, which accounts for between 15-20% of the debt. This money is considered a loss of purchasing power since the money will be diverted from the US economy.

::这笔债务是公共债务。 因为政府欠它自己,它没有私人债务的影响。 私人债务是个人欠他人的债务,因此必须偿还。 对于政府来说,它并不担心贷款的最终偿还,因为政府可以简单地发行更多的债券来偿付未偿债务。 当政府还清债务时,购买力没有损失,因为有些个人放弃部分购买力来偿还债务。 政府只是收税,然后将钱重新分配给其他人。 这一规则的例外是欠外国人的债务,这些债务占债务的15-20 % 。 这笔钱被视为购买力的损失,因为这笔钱将从美国经济中转移。The United States as a Global Borrower

::美国作为全球借款国In the global economy, trillions of dollars of financial investment cross national borders every year. In the early 2000s, financial investors from foreign countries were investing several hundred billion dollars per year more in the U.S. economy than U.S. financial investors were investing abroad. The following Work It Out deals with one of the macroeconomic concerns for the U.S. economy in recent years.

::在全球经济中,每年有数万亿美元的金融投资跨越国界。 2000年代初期,来自外国的金融投资者每年在美国经济中投资数千亿美元,比美国金融投资者在国外投资要多。 随后的《工作出来 》 ( Work It Out)解决了近年来美国经济所关注的宏观经济问题之一。

The Effect of Growing U.S. Debt

::不断增长的美国债务的影响Imagine that the U.S. economy became viewed as a less desirable place for foreign investors to put their money because of fears about the growth of the U.S. public debt. Using the four-step process for analyzing how changes in supply and demand affect equilibrium outcomes, how would increased U.S. public debt affect the equilibrium price and quantity for capital in U.S. financial markets?

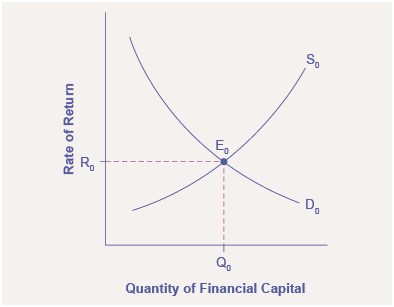

::想象一下,由于担心美国公共债务的增长,美国经济被看成是外国投资者放钱不可取的地方。 利用四步进程分析供求变化如何影响平衡结果,美国公共债务的增加将如何影响美国金融市场资本的平衡价格和数量?Step 1. Draw a diagram showing demand and supply for financial capital that represents the original scenario in which foreign investors are pouring money into the U.S. economy. 3 shows a demand curve, D, and a supply curve, S, where the supply of capital includes the funds arriving from foreign investors. The original equilibrium E 0 occurs at interest rate R 0 and quantity of financial investment Q 0 .

::步骤1. 绘制一张图表,显示金融资本的供需情况,显示外国投资者向美国经济注入资金的最初情景。 3 显示需求曲线、D和供应曲线,S,资本供应包括外国投资者提供的资金,E0的原始平衡按利率R0和资金投资数量Q0计算。The United States as a Global Borrower Before U.S. Debt Uncertainty

::美国作为美国债务不确定性之前的全球借款国The graph shows the demand for financial capital from and supply of financial capital into the U.S. financial markets by the foreign sector before the increase in uncertainty regarding U.S. public debt. The original equilibrium (E 0 ) occurs at an equilibrium rate of return (R 0 ) and the equilibrium quantity is at Q 0 .

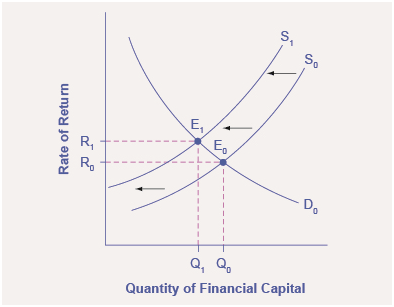

::图表显示了外国部门在美国公共债务不确定性增加之前对来自美国金融市场的金融资本的需求和向美国金融市场的金融资本供应情况。 最初的平衡(E0)以平衡的回报率(R0)发生,平衡数量为Q0。Step 2. Will the diminished confidence in the U.S. economy as a place to invest effect demand or supply of financial capital? Yes, it will effect supply. Many foreign investors look to the U.S. financial markets to store their money in safe financial vehicles with low risk and stable returns. As the U.S. debt increases, debt servicing will increase—that is, more current income will be used to pay the interest rate on past debt. Increasing U.S. debt also means that businesses may have to pay higher interest rates to borrow money because business is now competing with the government for financial resources.

::步骤2. 对美国经济作为投资影响性金融资本需求或供应的场所的信心降低是否会影响金融资本供应? 是的,这将影响供应。 许多外国投资者期待美国金融市场将其资金储存在风险低、回报稳定的安全金融工具中。 随着美国债务的增加,还本付息将增加 — — 也就是说,将用更多的流动收入支付过去债务的利率。 增加美国债务还意味着企业可能不得不支付更高的利率来借钱,因为企业现在与政府争夺财政资源。Step 3. Will supply increase or decrease? When the enthusiasm of foreign investors’ for investing their money in the U.S. economy diminishes, the supply of financial capital shifts to the left. 4 shows the supply curve shift from S 0 to S 1 .

::步骤3. 供应会增加还是减少?当外国投资者将其资金投向美国经济的热情减弱时,金融资本的供应向左转移。 4显示供应曲线从S0向S1的转变。The United States as a Global Borrower Before and After U.S. Debt Uncertainty

::美国作为美国债务不确定性前后的全球借款国The graph shows the demand for financial capital and supply of financial capital into the U.S. financial markets by the foreign sector before and after the increase in uncertainty regarding U.S. public debt. The original equilibrium (E 0 ) occurs at an equilibrium rate of return (R 0 ) and the equilibrium quantity is at Q 0 .

::图表显示了外国部门在美国公共债务不确定性增加之前和之后对金融资本的需求以及向美国金融市场提供金融资本的需求。 最初的平衡(E0)以平衡的回报率(R0)发生,平衡数量为Q0。Step 4. Thus, foreign investors’ diminished enthusiasm leads to a new equilibrium, E 1 , which occurs at the higher interest rate, R 1 , and the lower quantity of financial investment, Q 1 .

::4. 因此,外国投资者的热情减弱导致新的平衡,即E1, 利率较高,R1, 金融投资量较低,Q1。The economy has experienced an enormous inflow of foreign capital. According to U.S. Bureau of Economic Analysis, by 2012, U.S. investors had accumulated $20.1 trillion of foreign assets, but foreign investors owned a total $25.2 trillion of U.S. assets. If foreign investors were to pull their money out of the U.S. economy and invest elsewhere in the world, the result could be a significantly lower quantity of financial investment in the United States, available only at a higher interest rate. This reduced inflow of foreign financial investment could impose hardship on U.S. consumers and firms interested in borrowing.

::美国经济分析局指出,到2012年,美国投资者积累了20.1万亿美元外国资产,但外国投资者拥有总共25.2万亿美元美国资产。 如果外国投资者从美国经济中提款到世界其他地方投资,其结果可能是美国金融投资量大幅下降,只能以更高的利率获得。 外国金融投资流入量的减少可能会给美国消费者和有兴趣借贷的公司带来困难。In a modern, developed economy, financial capital often moves invisibly through electronic transfers between one bank account and another. Yet these flows of funds can be analyzed with the same tools of demand and supply as markets for goods or labor.

::在现代发达经济中,金融资本往往通过一个银行账户和另一个银行账户之间的电子转账来隐蔽地流动。 然而,这些资金流动可以用与货物或劳动力市场相同的供求工具来分析。Video: The National Debt and Federal Budget Deficit Deconstructed

::录像:国家债务和联邦预算赤字减少Federal Deficits and the National Debt

::联邦赤字和国家债务Having discussed the revenue (taxes) and expense (spending) side of the budget, we now turn to the annual budget deficit or surplus, which is the difference between the tax revenue collected and spending over a fiscal year, which starts October 1 and ends September 30 of the next year.

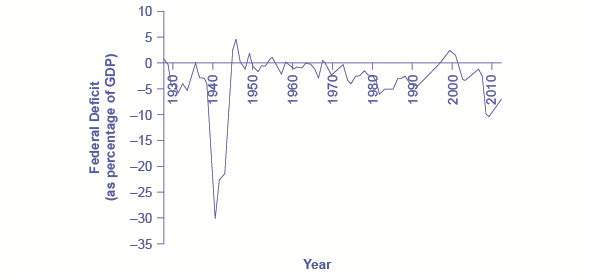

::在讨论了预算的收入(税收)和支出(支出)方面之后,我们现在转向年度预算赤字或盈余,即从10月1日开始至下一年9月30日结束的一个财政年度的税收收入与支出之间的差额。5 shows the pattern of annual federal budget deficits and surpluses, back to 1930, as a share of GDP. When the line is above the horizontal axis, the budget is in surplus; when the line is below the horizontal axis, a budget deficit occurred. Clearly, the biggest deficits as a share of GDP during this time were incurred to finance World War II. Deficits were also large during the 1930s, the 1980s, the early 1990s, and most recently during the recession of 2008–2009.

::5是1930年前联邦年度预算赤字和盈余占GDP的比例。 当项目高于水平轴时,预算为盈余;当项目低于水平轴时,出现预算赤字。 显然,这一时期最大的赤字占GDP的比例用于为二战提供资金。 在1930年代、1980年代、1990年代初以及最近的2008-2009年衰退期间,赤字也很大。Pattern of Federal Budget Deficits and Surpluses, 1930–2012

::1930-2012年联邦预算赤字和盈余模式The federal government has run budget deficits for decades. The budget was briefly in surplus in the late 1990s before heading into deficit again in the first decade of the 2000s—and especially deep deficits in the recession of 2008–2009. (Source: Economic Report of the President, Table B-79, http://www.gpo.gov/fdsys/pkg/ERP-2013/content-detail.html)

Debt/GDP Ratio

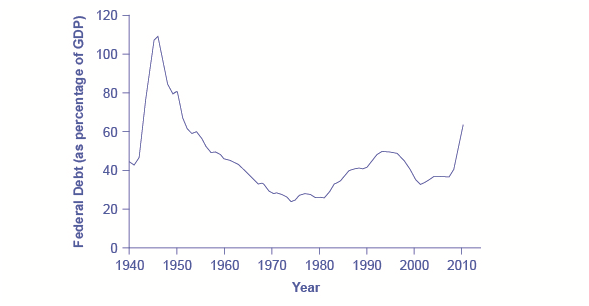

::债务/国内总产值比率Another useful way to view the budget deficit is through the prism of accumulated debt rather than annual deficits. The national debt refers to the total amount that the government has borrowed over time; in contrast, the budget deficit refers to how much has been borrowed in one particular year. 6 shows the ratio of debt/GDP since 1940. Until the 1970s, the debt/GDP ratio revealed a fairly clear pattern of federal borrowing. The government ran up large deficits and raised the debt/GDP ratio in World War II, but from the 1950s to the 1970s the government ran either surpluses or relatively small deficits, and so the debt/GDP ratio drifted down. Large deficits in the 1980s and early 1990s caused the ratio to rise sharply. When budget surpluses arrived from 1998 to 2001, the debt/GDP ratio declined substantially. The budget deficits starting in 2002 then tugged the debt/GDP ratio higher—with a big jump when the recession took hold in 2008–2009.

::观察预算赤字的另一个有用方式是通过累积债务的棱镜而不是年度赤字。 国民债务指的是政府长期借入的总额;相反,预算赤字指的是某一年借入的金额。 6是1940年以来的债务/GDP比率。 直到1970年代,债务/GDP比率显示出相当明确的联邦借款模式。 在二战期间,政府经历了巨大的赤字,提高了债务/GDP比率,但从1950年代到1970年代,政府要么有盈余,要么有相对较小的赤字,因此债务/GDP比率逐渐下降。 1980年代和1990年代初的高赤字导致比率急剧上升。 当1998年至2001年的预算盈余出现时,债务/GDP比率大幅下降。 2002年开始的预算赤字又拉高了债务/GDP比率 — — 在2008年至2009年衰退期间,预算赤字持续大幅上升。Federal Debt as a Percentage of GDP, 1940–2010

::1940-2010年联邦债务占国内生产总值的百分比When government spending exceeds taxes, the gap is the budget deficit. When taxes exceed spending, the gap is a budget surplus. The recessionary period starting in late 2007 saw higher spending and lower taxes, combining to create a large deficit in 2009. (Source: Economic Report of the President, Tables B-80, B-81, and B-1, )

Government spending as a share of GDP declined steadily through the 1990s. The biggest single reason was that defense spending declined from 5.2% of GDP in 1990 to 3.0% in 2000, but interest payments by the federal government also fell by about 1.0% of GDP. However, federal tax collections increased substantially in the later 1990s, jumping from 18.1% of GDP in 1994 to 20.8% in 2000. Powerful economic growth in the late 1990s fueled the boom in taxes. Personal income taxes rise as income goes up; payroll taxes rise as jobs and payrolls go up; corporate income taxes rise as profits go up. At the same time, government spending on transfer payments such as unemployment benefits, foods stamps, and welfare declined with more people working.

::20世纪90年代,政府支出占国内生产总值的比例稳步下降。 最大的一个原因是国防支出从1990年占GDP的5.2%下降到2000年的3.0%,但联邦政府支付的利息也下降了约GDP的1.0 % 。 但是,1990年代后期,联邦税收大幅增长,从1994年占GDP的18.1%上升到2000年的20.8%。 1990年代后期强劲的经济增长刺激了税收的繁荣。 随着收入的上升,个人所得税上升;随着就业和工资的增加,工资税上升;随着利润的上升,公司所得税上升。 与此同时,政府用于失业福利、食品券和福利等转移税的支出随着更多人的工作而下降。This sharp increase in tax revenues and a decrease in expenditures on transfer payments was largely unexpected--even by experienced budget analysts. Budget surpluses came as a surprise. In the early 2000s, many of these factors started running in reverse. Tax revenues sagged, due largely to the recession that started in March 2001, which reduced revenues. A series of tax cuts were enacted by Congress and signed into law by President George W. Bush in 2001. In addition, government spending swelled due to increases in defense, healthcare, education, Social Security, and support programs for those who were hurt by the recession and the slow growth that followed. Deficits returned. When the severe recession hit in late 2007, spending climbed and tax collections fell to historically unusual levels, resulting in enormous deficits.

::税收的急剧增长和转移支付支出的减少在很大程度上是出乎意料的,即使经验丰富的预算分析家也是如此。预算盈余令人吃惊。在2000年代初,许多这些因素开始逆转。主要由于2001年3月开始的衰退,税收收入减少。国会颁布了一系列减税措施,并由乔治·W·布什总统于2001年签署成为法律。 此外,由于国防、保健、教育、社会保障和为那些因经济衰退和随后的缓慢增长而受伤害的人的支助方案的增加而导致政府支出膨胀。 赤字再次出现。 2007年底严重衰退时,支出攀升和税收下降到历史不寻常的水平,导致巨额赤字。Longer-term forecasts of the U.S. budget, a decade or more into the future, predict enormous deficits. The higher deficits run during the recession of 2008–2009 have repercussions, and the demographics will be challenging. The primary reason is the “baby boom”—the exceptionally high birthrates that began in 1946, right after World War II, and lasted for about two decades. Starting in 2010, the front edge of the baby boom generation began to reach age 65, and in the next two decades, the proportion of Americans over the age of 65 will increase substantially. The current level of the payroll taxes that support Social Security and Medicare will fall well short of the projected expenses of these programs, as the following Clear It Up feature shows; thus, the forecast is for large budget deficits. A decision to collect more revenue to support these programs or to decrease benefit levels would alter this long-term forecast.

::更长期的美国预算预测 — — 未来十年或十年以上 — — 预测会出现巨大的赤字。 2008—2009年衰退期间赤字增加产生了影响,人口构成也将面临挑战。 主要原因是“婴儿繁荣 ” — —1946年即第二次世界大战后开始的、持续了大约20年的极高出生率。 从2010年开始,婴儿繁荣一代的前端开始到65岁,而在未来20年,65岁以上的美国人比例将大幅上升。 支持社会保障和医疗保险的当前工资税水平将远远低于这些计划的预计支出水平,正如以下的“清晰增长”特征所显示的;因此,预测是巨大的预算赤字。 增加收入支持这些计划或降低福利水平的决定将改变这一长期预测。What is the Long-term Budget Outlook for Social Security and Medicare?

::《社会保障和医疗保险长期预算展望》是什么?In 1946, just one American in 13 was over age 65. By 2000, it was one in eight. By 2030, one American in five will be over age 65. Two enormous U.S. federal programs focus on the elderly—Social Security and Medicare. The growing numbers of elderly Americans will increase spending on these programs, as well as on Medicaid. The current payroll tax levied on workers, which supports all of Social Security and the hospitalization insurance part of Medicare will not be enough to cover the expected costs. So, what are the options?

::1946年,13个美国人中只有1个超过65岁,到2000年,这一数字是8:1。到2030年,五分之一美国人将超过65岁。 两大美国联邦方案都以老年人——社会保障和医疗保险为重点。 越来越多的美国老年人将增加这些方案以及医疗补助的支出。 目前对工人征收的工资税支持医疗保险的所有社会保障和住院保险部分将不足以支付预期成本。 因此,有什么选择呢?Long-term projections from the Congressional Budget Office in 2009 are that Medicare and Social Security spending combined will rise from 8.3% of GDP in 2009 to about 13% by 2035 and about 20% in 2080. If this rise in spending occurs without any corresponding rise in tax collections, then some mix of changes must occur: (1) taxes will need to be increased dramatically; (2) other spending will need to be cut dramatically; (3) the retirement age and/or age receiving Medicare benefits will need to increase, or (4) the federal government will need to run extremely large budget deficits.

::国会预算办公室2009年的长期预测是,医疗保险和社会保障支出合并将从2009年占国内生产总值的8.3%增加到2035年的13%和2080年的20%左右。 如果支出的增加没有相应增加税收,那么就必须发生一些变化1) 税收需要大幅提高;(2) 其他支出需要大幅削减;(3) 领取医疗保险福利的退休年龄和(或)年龄需要提高,或者(4) 联邦政府需要大量预算赤字。

Some proposals suggest removing the cap on wages subject to the payroll tax, so those with very high incomes would have to pay the tax on the entire amount of their wages. Other proposals suggest moving Social Security and Medicare from systems in which workers pay for retirees toward programs that set up accounts where workers save funds over their lifetimes and then draw out after retirement to pay for healthcare.

::有些建议建议取消工资税的上限,因此那些收入非常高的人必须缴纳全部工资的税。 其他建议建议将社会保障和医疗保险从工人为退休人员支付工资的制度转移到建立账户的方案上,即工人在一生中储蓄资金,然后退休后提取资金支付医疗保健费用。The United States is not alone in this problem. Indeed, providing the promised level of retirement and health benefits to a growing proportion of elderly with a falling proportion of workers is an even more severe problem in many European nations and in Japan. How to pay promised levels of benefits to the elderly will be a difficult public policy decision.

::事实上,在许多欧洲国家和日本,向越来越多的工人比例下降的老年人提供所承诺的退休和健康福利水平是一个更为严重的问题。 如何向老年人支付所承诺的福利水平将是一项困难的公共政策决定。In the next module, we shift to the use of fiscal policy to counteract business cycle fluctuations. In addition, we will explore proposals requiring a balanced budget—that is, for government spending and taxes to be equal each year. Fiscal policy and government borrowing also will affect national saving—and thus affect economic growth and trade imbalances.

::在下一个单元中,我们将转向使用财政政策来抵制商业周期的波动。 此外,我们将探讨要求平衡预算的建议,即政府开支和税收每年相等,财政政策和政府借贷也将影响国民储蓄,从而影响经济增长和贸易不平衡。For most of the twentieth-century, the U.S. government took on debt during wartime then slowly paid down that debt in peacetime. However, it took on quite substantial debts in peacetime in the 1980s and early 1990s before a brief period of budget surpluses from 1998 to 2001. This was followed by a return to annual budget deficits since 2002, with very large deficits in the recession of 2008 and 2009. A budget deficit or budget surplus is measured annually. Total government debt or national debt is the sum of budget deficits and budget surpluses over time.

::20世纪的大部分时间,美国政府在战争期间承担债务,然后在和平时期缓慢偿还债务,然而,在1980年代和1990年代初的和平时期,在1998年至2001年短暂的预算盈余期之前,美国政府在1980年代和1990年代初承担了相当可观的债务,随后又恢复到2002年以来的年度预算赤字,2008年和2009年的衰退期间出现非常巨大的赤字。 预算赤字或预算盈余每年衡量一次。 政府债务或国民债务总额是长期预算赤字和预算盈余的总和。The Question of a Balanced Budget

::预算平衡问题For many decades, going back to the 1930s, proposals have been put forward to require that the U.S. government balance its budget every year. In 1995, a proposed constitutional amendment that would require a balanced budget passed the U.S. House of Representatives by a wide margin and failed in the U.S. Senate by only a single vote. (For the balanced budget to have become an amendment to the Constitution would have required a two-thirds vote by Congress and passage by three-quarters of the state legislatures.)

::早在1930年代,数十年来,一直有人提议要求美国政府每年平衡预算。 1995年,一项要求平衡预算的拟议宪法修正案以大幅度的幅度通过了美国众议院,但美国参议院只以一票就失败了。 (平衡预算要成为宪法修正案,就需要国会三分之二的选票和四分之三的州立法机构通过。 )Most economists view the proposals for a perpetually balanced budget with bemusement. After all, in the short term, economists would expect the budget deficits and surpluses to fluctuate up and down with the economy and the automatic stabilizers. Economic recessions should automatically lead to larger budget deficits or smaller budget surpluses while economic booms lead to smaller deficits or larger surpluses. A requirement that the budget is balanced each and every year would prevent these automatic stabilizers from working and would worsen the severity of economic fluctuations.

::多数经济学家都对长期平衡预算的建议持乐观态度。 毕竟,从短期看,经济学家会期望预算赤字和盈余会随着经济和自动稳定因素而上下波动。 经济衰退应该自动导致更大的预算赤字或较小的预算盈余,而经济繁荣则会导致较小的赤字或更大的盈余。 预算平衡的要求每年都会阻碍这些自动稳定因素的运转,并会加剧经济波动的严重性。Some supporters of the balanced budget amendment like to argue, since households must balance their own budgets, the government should too. But this analogy between household and government behavior is severely flawed. Most households do not balance their budgets every year. Some years households borrow to buy houses or cars or to pay for medical expenses or college tuition. Other years they repay loans and save funds in retirement accounts. After retirement, they withdraw and spend those savings. Also, the government is not a household for many reasons, one of which is that the government has macroeconomic responsibilities. The argument of Keynesian macroeconomic policy is that the government needs to lean against the wind, spending when times are hard and saving when times are good, for the sake of the overall economy.

::平衡预算修正案的一些支持者认为,由于家庭必须平衡自己的预算,政府也应该这样做。但家庭和政府行为之间的这种类比有严重缺陷。大多数家庭并不每年平衡预算。有些年份,家庭借钱购买房屋或汽车,或支付医疗费用或大学学费。有些年份,他们还偿还贷款,在退休账户中存留资金。退休后,他们撤回并用掉这些储蓄。此外,由于许多原因,政府不是家庭,其中一个原因是政府负有宏观经济责任。凯恩斯主义宏观经济政策的论据是政府需要依靠风力,为了整个经济,在时间好的时候,花费时间是困难的,节省时间。There is also no particular reason to expect a government budget to be balanced in the medium term of a few years. For example, a government may decide that by running large budget deficits, it can make crucial long-term investments in human capital and physical infrastructure that will build the long-term productivity of a country. These decisions may work out well or poorly, but they are not always irrational. Such policies of ongoing government budget deficits may persist for decades. As the U.S. experience from the end of World War II up to about 1980 shows, it is perfectly possible to run budget deficits almost every year for decades, but as long as the percentage increases in debt are smaller than the percentage growth of GDP, the debt/GDP ratio will decline at the same time.

::也没有特别的理由期待政府预算在几年的中期内实现平衡。 比如,政府可以决定,通过大量预算赤字,它可以对人力资本和物质基础设施进行至关重要的长期投资,从而建设国家的长期生产力。 这些决定可能效果良好或差,但并不总是不合理。 这种政府持续预算赤字的政策可能持续数十年。 正如美国从二战结束到大约1980年的经验所显示的那样,几十年来几乎每年都有预算赤字,但只要债务增长的百分比小于GDP的增长率,债务/GDP比率就会同时下降。Nothing in this argument should be taken as a claim that budget deficits are always a wise policy. In the short run, a government that runs a very large budget deficit can shift aggregate demand to the right and trigger severe inflation. Additionally, governments may borrow for foolish or impractical reasons. Large budget deficits reduce national savings and can, in certain cases, reduce economic growth and even contribute to international financial crises. A requirement that the budget be balanced in each calendar year, however, is a misguided overreaction to the fear that in some cases, budget deficits can become too large.

::这一论点中的任何内容都不应被看作预算赤字总是明智政策的说法。 短期而言,预算赤字非常庞大的政府可以将总需求转向右翼并触发严重通货膨胀。 此外,政府可能出于愚蠢或不切实际的原因借钱。 巨额预算赤字会减少国民储蓄,在某些情况下会降低经济增长,甚至会助长国际金融危机。 但是,要求每个日历年平衡预算的要求是对担心在某些情况下预算赤字会变得太大的错误反应。No Yellowstone Park?

::没有黄石公园?-

Yellowstone National Park is one of the many national parks forced to close down during the government shut down in October 2013.

The federal budget shutdown of 2013 illustrated the many sides to fiscal policy and the federal budget. In 2013, Republicans and Democrats could not agree on which spending policies to fund and how large the government debt should be. Due to the severity of the recession in 2008–2009, the fiscal stimulus, and previous policies, the federal budget deficit and debt was historically high. One way to try to cut federal spending and borrowing was to refuse to raise the legal federal debt limit or tie on conditions to appropriation bills to stop the Affordable Health Care Act. This disagreement led to a two-week shutdown of the federal government and got close to the deadline where the federal government would default on its Treasury bonds. Finally, however, a compromise emerged and default was avoided. This shows clearly how closely fiscal policies are tied to politics.

::2013年联邦预算的停产表明了财政政策和联邦预算的诸多方面。 2013年,共和党和民主党无法就哪些支出政策融资以及政府债务应该有多大达成一致。 由于2008-2009年衰退、财政刺激和以往政策的严重性,联邦预算赤字和债务历来居高不下。 试图削减联邦支出和借款的一个方法就是拒绝提高法定联邦债务限额或将财政法案与拨款条件挂钩以阻止负担得起的保健法案。 这一分歧导致联邦政府关闭两周,并接近联邦政府拖欠国库债券的最后期限。 然而,最终出现了妥协和违约。 这清楚地表明财政政策与政治的紧密联系。Balanced budget amendments are a popular political idea, but the economic merits behind such proposals are questionable. Most economists accept that fiscal policy needs to be flexible enough to accommodate unforeseen expenditures, such as wars or recessions. While persistent, large budget deficits can indeed be a problem, a balanced budget amendment prevents even small, temporary deficits that might, in some cases, be necessary.

::平衡预算修正是一个流行的政治理念,但这种提案背后的经济优势值得怀疑。 大多数经济学家都认为财政政策必须足够灵活,以适应意外支出,如战争或衰退。 尽管长期存在的巨额预算赤字确实可能是一个问题,但平衡预算修正案甚至阻止了在某些情况下可能必要的小型临时赤字。The Impacts of Government Borrowing

::政府借款的影响Balanced budget amendments are a popular political idea, but the economic merits behind such proposals are questionable. Most economists accept that fiscal policy needs to be flexible enough to accommodate unforeseen expenditures, such as wars or recessions. While persistent, large budget deficits can indeed be a problem, a balanced budget amendment prevents even small, temporary deficits that might, in some cases, be necessary.

::平衡预算修正是一个流行的政治理念,但这种提案背后的经济优势值得怀疑。 大多数经济学家都认为财政政策必须足够灵活,以适应意外支出,如战争或衰退。 尽管长期存在的巨额预算赤字确实可能是一个问题,但平衡预算修正案甚至阻止了在某些情况下可能必要的小型临时赤字。Governments have many competing demands for financial support. Any spending should be tempered by fiscal responsibility and by looking carefully at the spending’s impact. When a government spends more than it collects in taxes, it runs a budget deficit. Then it needs to borrow. When government borrowing becomes especially large and sustained, it can substantially reduce the financial capital available to private sector firms, as well as lead to trade imbalances and even financial crises.

::政府有许多相互竞争的财政支持需求。 任何支出都应该受到财政责任和仔细观察支出影响的影响的制约。 当政府支出超过税收时,它就会出现预算赤字。 然后它就需要借款。 当政府借贷变得特别庞大和持续时,它可以大幅削减私人企业的金融资本,并导致贸易失衡甚至金融危机。We have discussed the concepts of deficits and debt, as well as how a government could use fiscal policy to address recession or inflation. This chapter begins by building on the national savings and investment identity, to show how government borrowing affects firms’ physical capital investment levels and trade balances. A prolonged period of budget deficits may lead to lower economic growth, in part because the funds borrowed by the government to fund its budget deficits are typically no longer available for private investment. Moreover, a sustained pattern of large budget deficits can lead to disruptive economic patterns of high inflation, substantial inflows of financial capital from abroad, plummeting exchange rates, and heavy strains on a country’s banking and financial system.

::我们讨论了赤字和债务的概念,以及政府如何利用财政政策应对衰退或通胀。 本章首先以国民储蓄和投资身份为基础,展示政府借贷如何影响企业的有形资本投资水平和贸易平衡。 长期的预算赤字可能导致经济增长放缓,部分原因是政府为其预算赤字融资的资金通常不再可用于私人投资。 此外,持续的巨大预算赤字模式可能导致高通胀、国外大量金融资本流入、汇率暴跌以及一国银行和金融体系的沉重压力等破坏性经济模式。How Government Borrowing Affects Investment and the Trade Balance

::政府借款如何影响投资和贸易平衡When governments are borrowers in financial markets, there are three possible sources for the funds from a macroeconomic point of view: (1) households might save more; (2) private firms might borrow less; and (3) the additional funds for government borrowing might come from outside the country, from foreign financial investors. Let’s begin with a review of why one of these three options must occur, and then explore how interest rates and exchange rates adjust to these connections.

::当政府是金融市场的借款人时,从宏观经济角度看,资金有三种可能的来源The National Saving and Investment Identity

::国家储蓄和投资身份The national saving and investment identity provides a framework for showing the relationships between the sources of demand and supply in financial capital markets. The identity begins with a statement that must always hold true: the quantity of financial capital supplied in the market must equal the quantity of financial capital demanded.

::国民储蓄和投资身份提供了一个框架,用以显示金融资本市场供求来源之间的关系,其特征始于必须始终真实的声明:市场提供的金融资本数量必须与所需金融资本数量相等。The U.S. economy has two main sources for financial capital: private savings from inside the U.S. economy and public savings.

::美国经济有两个主要的金融资本来源:美国经济内部的私人储蓄和公共储蓄。Total savings = Private savings (S) + Public savings (T – G)

::储蓄总额=私人储蓄(S)+公共储蓄(T-G)These include the inflow of foreign financial capital from abroad. The inflow of savings from abroad is, by definition, equal to the trade deficit. So this inflow of foreign investment capital can be written as imports (M) minus exports (X). There are also two main sources of demand for financial capital: private sector investment (I) and government borrowing. Government borrowing in any given year is equal to the budget deficit, and can be written as the difference between government spending (G) and net taxes (T). Let’s call this equation 1.

::从定义上说,国外储蓄的流入相当于贸易赤字。 因此,外国投资资本的流入可以记为进口(M)减去出口(X)。 对金融资本的需求还有两个主要来源:私营部门投资(I)和政府借贷。 任何一年的政府借贷都相当于预算赤字,也可以记为政府支出(G)和净税(T)之间的差额。 我们称之为1等式。Quantity supplied of financial capital = Quantity demanded of financial capital

::提供的金融资本数量 = 要求的金融资本数量Private savings + Inflow of foreign savings= Private investment + Government budget deficit

::私人储蓄+外国储蓄流入量=私人投资+政府预算赤字S + (M – X) = I + (G –T)

::S+ (M - X) = I + (G - T)Governments often spend more than they receive in taxes and, therefore, public savings (T – G) is negative. This causes a need to borrow money in the amount of (G – T) instead of adding to the nation’s savings. If this is the case, governments can be viewed as demanders of financial capital instead of suppliers. So, in algebraic terms, the national savings and investment identity can be rewritten like this:

::政府往往花在税收上的钱多于所得,因此,公共储蓄(T-G)是负数的。 这导致需要借钱(G-T)而不是增加国家储蓄。 如果是这样的话,政府可以被视为金融资本需求者而不是供应商。 因此,用代数术语来说,国家储蓄和投资身份可以重写成这样:Private investment = Private savings + Public savings + Trade deficit

::私人投资 = 私人储蓄 + 公共储蓄 + 贸易赤字I = S + (T – G) + (M – X)

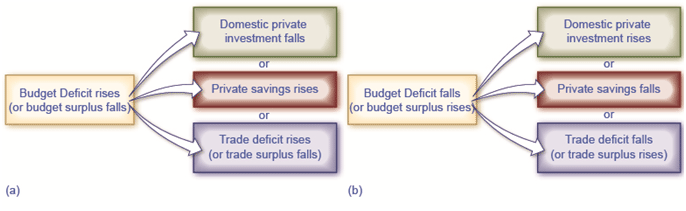

::I = S + (T - G) + (M - X)Let’s call this equation 2. A change in any part of the national saving and investment identity must be accompanied by offsetting changes in at least one other part of the equation because the equality of quantity supplied and quantity demanded is always assumed to hold. If the government budget deficit changes, then either private saving or investment or the trade balance—or some combination of the three—must change as well. 8 shows the possible effects.

::将这一方程式称为2. 在改变国民储蓄和投资特征的任何部分的同时,必须至少对等方程式的另外一部分进行抵消性改变,因为所供应的量和所要求量的等同性总是假定维持不变的。 如果政府预算赤字发生变化,那么私人储蓄或投资或贸易平衡 — — 或者三者之间的某种组合 — — 也必须有所改变。 8 显示了可能的效果。Effects of Change in Budget Surplus or Deficit on Investment, Savings, and The Trade Balance

::预算盈余或赤字对投资、储蓄和贸易平衡的影响Chart (a) shows the potential results when the budget deficit rises (or budget surplus falls). Chart (b) shows the potential results when the budget deficit falls (or budget surplus rises).

What about Budget Surpluses and Trade Surpluses?

::那么预算盈余和贸易盈余呢?The national saving and investment identity must always hold true because, by definition, the quantity supplied and quantity demanded in the financial capital market must always be equal. However, the formula will look somewhat different if the government budget is in deficit rather than surplus or if the balance of trade is in surplus rather than deficit. For example, in 1999 and 2000, the U.S. government had budget surpluses, although the economy was still experiencing trade deficits. When the government was running budget surpluses, it was acting as a saver rather than a borrower, and supplying rather than demanding financial capital. As a result, the national saving and investment identity during this time would be more properly written:

::国民储蓄和投资特性必须始终保持真实,因为根据定义,金融资本市场的供给量和所需数量必须始终相等;然而,如果政府预算出现赤字而不是盈余,或者贸易平衡出现盈余而不是赤字,公式将有所不同。 例如,在1999年和2000年,美国政府预算盈余,尽管经济仍然有贸易赤字。 当政府运行预算盈余时,它只是作为储蓄者而不是借款者,提供而不是要求金融资本。 因此,在此期间,国民储蓄和投资身份将更恰当地写成:Quantity supplied of financial capital= Quantity demanded of financial capital

::提供的金融资本数量=要求的金融资本数量Private savings + Trade deficit + Government surplus= Private Investment

::私人储蓄+贸易赤字+政府盈余=私人投资S + (M – X) + (T – G) = I

::S+ (M - X) + (T - G) = ILet's call this equation 3. Notice that this expression is mathematically the same as equation 2 except the savings and investment sides of the identity have simply flipped sides.

::注意这个表达方式在数学上与方程式2相同 除了这个身份的储蓄和投资方面 只是翻转了两面During the 1960s, the U.S. government was often running a budget deficit, but the economy was typically running trade surpluses. Since a trade surplus means that an economy is experiencing a net outflow of financial capital, the national saving and investment identity would be written:

::20世纪60年代,美国政府经常出现预算赤字,但经济通常会出现贸易顺差。 由于贸易顺差意味着一个经济体正在经历金融资本净流出,国家储蓄和投资身份将写成:Quantity supplied of financial capital = Quantity demanded of financial capital

::提供的金融资本数量 = 要求的金融资本数量Private savings = Private investment + Outflow of foreign savings + Government budget deficit

::私人储蓄 = 私人投资 + 外国储蓄流出 + 政府预算赤字S= I + (X – M) + (G – T)

::S=I + (X - M)+ (G - T)Instead of the balance of trade representing part of the supply of financial capital, which occurs with a trade deficit, a trade surplus represents an outflow of financial capital leaving the domestic economy and being invested elsewhere in the world.

::贸易顺差代表了金融资本供应的部分贸易平衡,而贸易逆差是贸易逆差造成的,而贸易顺差则代表了金融资本流出,离开国内经济,在世界其他地方投资。Quantity supplied of financial capital= Quantity demanded of financial capital demand

::提供的金融资本数量=要求的金融资本需求数量Private savings = Private investment + Government budget deficit + Trade surplus

::私人储蓄 = 私人投资 + 政府预算赤字 + 贸易盈余I + (G – T) + (X – M)

::I + (G - T) + (X - M)The point to this parade of equations is that the national saving and investment identity is assumed to always hold. So when you write these relationships, it is important to engage your brain and think about what is on the supply side and what is on the demand side of the financial capital market before you put pencil to paper.

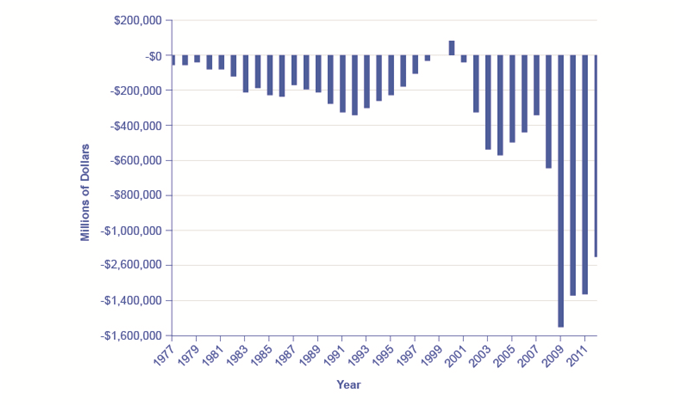

::这一系列方程式的要点是,国家储蓄和投资身份被假定永远维持。 因此,当您写下这些关系时,重要的是在您把铅笔贴在纸上之前,让您的大脑思考一下金融资本市场的供应方和需求方。As can be seen in 9, the Office of Management and Budget shows that the United States has consistently run budget deficits since 1977, with the exception of 1999 and 2000. What is alarming is the dramatic increase in budget deficits that has occurred since 2008, which in part reflects declining tax revenues and increased safety net expenditures due to the Great Recession. (Recall that T is net taxes. When the government must transfer funds back to individuals for safety net expenditures like Social Security and unemployment benefits, budget deficits rise.) These deficits have implications for the future health of the U.S. economy.

::从9中可以看出,管理和预算厅表明,美国自1977年以来,除了1999年和2000年之外,一直存在预算赤字,但1999年和2000年除外。 令人震惊的是,自2008年以来,预算赤字急剧增加,这在一定程度上反映了税收下降和安全网支出的增加,因为大衰退。 (回顾T是净税,当政府必须把资金转还给个人,用于社会保障和失业福利等安全网支出时,预算赤字就会增加。 )这些赤字对美国经济的未来健康产生影响。United States On-Budget, Surplus, and Deficit, 1977–2012 (in millions)

::1977-2012年美国预算、盈余和赤字(百万美元)The United States has run a budget deficit for over 30 years, with the exception of 1999 and 2000. Military expenditures, entitlement programs, and the decrease in tax revenue coupled with increased safety net support during the Great Recession are major contributors to the dramatic increases in the deficit after 2008. (Source: )

A rising budget deficit may result in a fall in domestic investment, a rise in private savings, or a rise in the trade deficit. The following modules discuss each of these possible effects in more detail. A change in any part of the national saving and investment identity suggests that if the government budget deficit changes, then either private savings, private investment in physical capital, or the trade balance—or some combination of the three—must change as well.

::预算赤字增加可能导致国内投资下降、私人储蓄增加或贸易赤字增加,以下单元更详细地讨论其中每一种可能的影响。 国民储蓄和投资特性的任何部分的改变都表明,如果政府预算赤字发生变化,那么私人储蓄、实物资本私人投资或贸易平衡(或三者组合的某些组合)也必须发生变化。How Government Borrowing Affects Private Saving

::政府借款如何影响私人储蓄A change in government budgets may impact private saving. Imagine that people watch government budgets and adjust their savings accordingly. For example, whenever the government runs a budget deficit, people might reason: “Well, a higher budget deficit means that I’m just going to owe more taxes in the future to pay off all that government borrowing, so I’ll start saving now.” If the government runs budget surpluses, people might reason: “With these budget surpluses (or lower budget deficits), interest rates are falling, so that saving is less attractive. Moreover, with a budget surplus the country will be able to afford a tax cut sometime in the future. I won’t bother saving as much now.”

::政府预算的改变可能会影响私人储蓄。 想象一下人们会看到政府预算并相应调整储蓄。 比如,当政府出现预算赤字时,人们可能会提出理由 : “ 高预算赤字意味着我将来会欠更多的税来偿还所有政府借款,所以我现在就开始储蓄。 ”如果政府运行预算盈余,人们可能会提出理由 : “ 随着这些预算盈余(或较低的预算赤字 ) , 利率正在下降,因此储蓄的吸引力将降低。 此外,如果预算盈余在未来某个时候能够让国家承担减税。 我将不再费钱储蓄了。 ”The theory that rational private households might shift their saving to offset government saving or borrowing is known as Ricardian equivalence because the idea has intellectual roots in the writings of the early nineteenth-century economist David Ricardo (1772–1823). If Ricardian equivalence holds completely true, then in the national saving and investment identity, any change in budget deficits or budget surpluses would be completely offset by a corresponding change in private saving. As a result, changes in government borrowing would have no effect at all on either physical capital investment or trade balances.

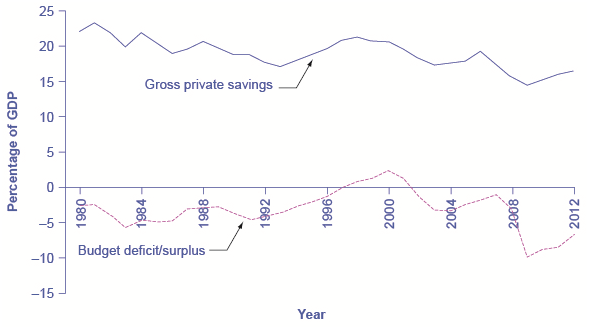

::理性的私人家庭可能将其储蓄转用于抵消政府储蓄或借款的理论被称为“哥斯达黎加等值 ” , 因为这一理念在十九世纪初的经济学家大卫·里卡多(David Ricardo)的著作(1772 - 1823 ) 中具有知识根基(1772 - 1823 ) 。 如果哥斯达黎加等值完全正确,那么在国民储蓄和投资身份中,预算赤字或预算盈余的任何变化都会被相应的私人储蓄变化完全抵消。 结果,政府借贷的变化将完全对有形资本投资或贸易平衡没有任何影响。In practice, the private sector only sometimes and partially adjusts its savings behavior to offset government budget deficits and surpluses. 10 shows the patterns of U.S. government budget deficits and surpluses and the rate of private saving—which includes saving by both households and firms—since 1980. The connection between the two is not at all obvious. In the mid-1980s, for example, government budget deficits were quite large, but there is no corresponding surge of private saving. However, when budget deficits turn to surpluses in the late 1990s, there is a simultaneous decline in private saving. When budget deficits get very large in 2008 and 2009, on the other hand, there is some sign of a rise in saving. A variety of statistical studies based on the U.S. experience suggests that when government borrowing increases by $1, private saving rises by about 30 cents. A World Bank study done in the late 1990s, looking at government budgets and private saving behavior in countries around the world, found a similar result.

::实际上,私营部门只是有时和部分调整其储蓄行为,以抵消政府预算赤字和盈余。 10 显示1980年以来美国政府预算赤字和盈余以及私人储蓄(包括家庭和企业的储蓄)的格局,两者之间的关系并不明显。例如,在1980年代中期,政府预算赤字相当大,但没有相应的私人储蓄激增。然而,当预算赤字在1990年代末变为盈余时,私人储蓄同时下降。另一方面,当2008年和2009年预算赤字非常庞大时,出现了储蓄增加的迹象。基于美国经验的各种统计研究表明,当政府借款增加1美元时,私人储蓄增加约30美分。 世界银行在1990年代末进行的一项研究,研究了世界各国的政府预算和私人储蓄行为,也得出了类似的结果。U.S. Budget Deficits and Private Savings

::美国预算赤字和私人储蓄The theory of Ricardian equivalence suggests that any increase in government borrowing will be offset by additional private saving, while any decrease in government borrowing will be offset by reduced private saving. Sometimes this theory holds true, and sometimes it does not hold true at all. (Source: Bureau of Economic Analysis and Federal Reserve Economic Data)

So private saving does increase to some extent when governments run large budget deficits, and private saving falls when governments reduce deficits or run large budget surpluses. However, the offsetting effects of private saving compared to government borrowing are much less than one-to-one. In addition, this effect can vary a great deal from country to country, from time to time, and over the short run and the long run.

::因此,当政府出现巨额预算赤字,私人储蓄下降,政府减少赤字或出现巨额预算盈余时,私人储蓄就会在某种程度上增加。 然而,私人储蓄与政府借贷相比的抵消效应远远低于一对一。 此外,这种效应可能因国而异,有时甚至从短期到长期。If the funding for a larger budget deficit comes from international financial investors, then a budget deficit may be accompanied by a trade deficit. In some countries, this pattern of a twin deficits has set the stage for international financial investors first to send their funds to a country and cause an appreciation of its exchange rate and then to pull their funds out and cause a depreciation of the exchange rate and a financial crisis as well. It depends on whether funding comes from international financial investors.

::如果为更大预算赤字提供的资金来自国际金融投资者,那么预算赤字可能伴随着贸易赤字。 在某些国家,这种双赤字模式为国际金融投资者首先将资金汇往一国并导致其汇率升值,然后将其资金抽出并导致汇率贬值和金融危机创造了条件。 这取决于国际金融投资者是否提供资金。The theory of Ricardian equivalence holds that changes in government borrowing or saving will be offset by changes in private saving. Thus, higher budget deficits will be offset by greater private saving, while larger budget surpluses will be offset by greater private borrowing. If the theory holds true, then changes in government borrowing or saving would have no effect on private investment in physical capital or on the trade balance. However, empirical evidence suggests that the theory holds true only partially.

::哥斯达黎加等值理论认为,政府借贷或储蓄的变化将被私人储蓄的变化所抵消。 因此,更高的预算赤字将被私人储蓄的增加所抵消,而更大的预算盈余将被私人借款的增加所抵消。 如果理论是正确的,那么政府借贷或储蓄的变化不会对私人对实物资本的投资或贸易平衡产生影响。 但是,经验证据表明,这一理论只能部分成立。Fiscal Policy and the Trade Balance

::财政政策和贸易平衡Government budget balances can affect the trade balance. As discusses, a net inflow of foreign financial investment always accompanies a trade deficit, while a net outflow of financial investment always accompanies a trade surplus. One way to understand the connection from budget deficits to trade deficits is that when government creates a budget deficit with some combination of tax cuts or spending increases, it will increase aggregate demand in the economy, and some of that increase in aggregate demand will result in a higher level of imports. A higher level of imports, with exports remaining fixed, will cause a larger trade deficit. That means foreigners’ holdings of dollars increase as Americans purchase more imported goods. Foreigners use those dollars to invest in the United States, which leads to an inflow of foreign investment. One possible source of funding our budget deficit is foreigners buying Treasury securities that are sold by the U.S. government. So a budget deficit is often accompanied by a trade deficit.

::政府预算平衡可能会影响贸易平衡。 正如讨论的那样,外国金融投资的净流入总是伴随着贸易赤字,而金融投资的净流出总是伴随着贸易盈余。 理解预算赤字与贸易赤字之间的联系的一个途径是,当政府创造预算赤字,同时将减税或增加支出结合起来时,它会增加经济总需求,而总需求的某些增长将导致进口水平的提高。 进口水平的提高,加上出口保持不变,将导致更大的贸易赤字。 这意味着随着美国人购买更多的进口货物,外国人的美元持有量会增加。 外国人利用这些美元在美国投资,这导致外国投资的流入。 我们预算赤字的可能资金来源是外国人购买美国政府出售的国库证券。 因此,预算赤字往往伴随着贸易赤字。Twin Deficits?

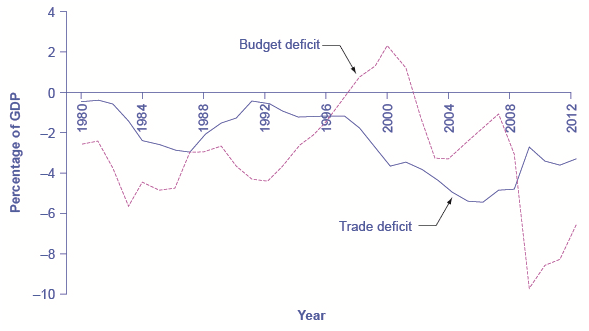

::双赤字?In the mid-1980s, it was common to hear economists and even newspaper articles refer to the twin deficits, as the budget deficit and trade deficit both grew substantially. 11 shows the pattern. The federal budget deficit went from 2.6% of GDP in 1981 to 5.1% of GDP in 1985—a drop of 2.5% of GDP. Over that time, the trade deficit moved from 0.5% in 1981 to 2.9% in 1985—a drop of 2.4% of GDP. In the mid-1980s, the considerable increase in government borrowing was matched by an inflow of foreign investment capital, so the government budget deficit and the trade deficit moved together.

::在1980年代中期,人们经常听到经济学家甚至报纸文章提到双重赤字,因为预算赤字和贸易赤字都大幅度增长。 11 显示出这种格局,联邦预算赤字从1981年占国内生产总值的2.6 % 下降到1985年的5.1% — — 下降了GDP的2.5 % 。 在此期间,贸易赤字从1981年的0.5 % 下降到1985年的2.9% — — 下降了GDP的2.4 % 。 在1980年代中期,政府借贷的大幅增长与外国投资资本的流入相匹配,因此政府预算赤字和贸易赤字一起转移。- U.S. Budget Deficits and Trade Deficits

In the 1980s, the budget deficit and the trade deficit declined at the same time. However, since then, the deficits have stopped being twins. The trade deficit grew smaller in the early 1990s as the budget deficit increased, and then the trade deficit grew larger in the late 1990s as the budget deficit turned into a surplus. In the first half of the 2000s, both budget and trade deficits increased. But in 2009, the trade deficit declined as the budget deficit increased.

::1980年代,预算赤字和贸易赤字同时下降,但自那以后,赤字不再是双胞胎。 1990年代初,随着预算赤字的增加,贸易赤字缩小了。 1990年代后期,随着预算赤字变成顺差,贸易赤字扩大。 2000年代上半期,预算赤字和贸易赤字都增加了。 2009年,贸易赤字随着预算赤字的增加而下降。Of course, no one should expect the budget deficit and trade deficit to move in lockstep, because the other parts of the national saving and investment identity—investment and private savings—will often change as well. In the late 1990s, for example, the government budget balance turned from deficit to surplus, but the trade deficit remained large and growing. During this time, the inflow of foreign financial investment was supporting a surge of physical capital investment by U.S. firms. In the first half of the 2000s, the budget and trade deficits again increased together, but in 2009, the budget deficit increased while the trade deficit declined. The budget deficit and the trade deficits are related to each other, but they are more like cousins than twins.

::当然,没有人应该料到预算赤字和贸易赤字会陷入僵局,因为国民储蓄和投资身份投资以及私人储蓄的其他部分也往往会发生变化。 比如,在1990年代末,政府预算平衡从赤字转向盈余,但贸易赤字仍然巨大且在增长。 在此期间,外国金融投资的流入支持了美国公司实物资本投资的激增。 在2000年代的前半期,预算和贸易赤字再次同时增加,但在2009年,预算赤字在贸易赤字下降的同时增加。 预算赤字和贸易赤字彼此相关,但它们更像表亲而不是双胞胎。Budget Deficits and Exchange Rates

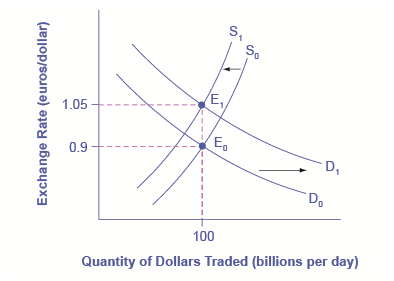

::预算赤字和汇率Exchange rates can also help to explain why budget deficits are linked to trade deficits. 12 shows a situation using the exchange rate for the U.S. dollar, measured in euros. At the original equilibrium (E 0 ), where the demand for U.S. dollars (D 0 ) intersects with the supply of U.S. dollars (S 0 ) on the foreign exchange market, the exchange rate is 0.9 euros per U.S. dollar and the equilibrium quantity traded in the market is $100 billion per day (which was roughly the quantity of dollar–euro trading in exchange rate markets in the mid-2000s). Then the U.S. budget deficit rises and foreign financial investment provides the source of funds for that budget deficit.

::汇率也可以帮助解释为什么预算赤字与贸易赤字相关。 12 12 显示一种使用美元汇率(以欧元计)的情况。 在最初的平衡(E0 ) , 美元(D0)需求与外汇市场对美元(S0)的供应交织在一起,汇率为0.9欧元兑1美元,市场交易的平衡量为每天1 000亿美元(大约相当于2000年代中期美元兑欧元的汇率市场交易量 ) 。 接着,美国预算赤字增加,外国金融投资为这一预算赤字提供了资金来源。International financial investors, as a group, will demand more U.S. dollars on foreign exchange markets to purchase the U.S. government bonds, and they will supply fewer of the U.S. dollars that they already hold in these markets. Demand for U.S. dollars on the foreign exchange market shifts from D 0 to D 1 and the supply of U.S. dollars falls from S 0 to S 1 . At the new equilibrium (E 1 ), the exchange rate has appreciated to 1.05 euros per dollar while, in this example, the quantity of dollars traded remains the same.

::作为一个集团,国际金融投资者将在外汇市场上对购买美国政府的债券提出更多的美元要求,并将减少他们在这些市场上已经持有的美元供应量。 外汇市场从D0到D1以及美元供应从S0到S1对美元的需求从S0下降到S1。 在新的平衡(E1)下,汇率已升至每美元1.05欧元,而在这个例子中,交易的美元数量保持不变。- Budget Deficits and Exchange Rates

Imagine that the U.S. government increases its borrowing and the funds come from European financial investors. To purchase U.S. government bonds, those European investors will need to demand more U.S. dollars on foreign exchange markets, causing the demand for U.S. dollars to shift to the right from D 0 to D 1 . European financial investors as a group will also be less likely to supply U.S. dollars to the foreign exchange markets, causing the supply of U.S. dollars to shift from S 0 to S 1 . The equilibrium exchange rate strengthens from 0.9 euro/ dollar at E 0 to 1.05 euros/dollar at E 1 .

::想象一下美国政府会增加借款,而资金来自欧洲金融投资者。 为了购买美国政府债券,这些欧洲投资者将需要在外汇市场上要求更多美元,导致对美元的需求从D0转向D1。 欧洲金融投资者作为一个集团也不太可能向外汇市场提供美元,导致美元的供应从S0转向S1。 平衡汇率从0.9欧元兑1美元,以E0兑1.05欧元兑1美元,以E1兑1.05欧元兑1美元。A stronger exchange rate, of course, makes it more difficult for exporters to sell their goods abroad while making imports cheaper, so a trade deficit (or a reduced trade surplus) results. Thus, a budget deficit can easily result in an inflow of foreign financial capital, a stronger exchange rate, and a trade deficit.

::当然,更强劲的汇率让出口商更难在国外出售货物,同时降低进口价格,因此贸易赤字(或贸易盈余减少 ) 。 因此,预算赤字很容易导致外国金融资本的流入、更强劲的汇率和贸易赤字。You can also imagine this appreciation of the exchange rate as being driven by interest rates. As explained earlier a budget deficit increases demand in markets for domestic financial capital, raising the domestic interest rate. A higher interest rate will attract an inflow of foreign financial capital, and appreciate the exchange rate in response to the increase in demand for U.S. dollars by foreign investors and a decrease in supply of U. S. dollars. Because of higher interest rates in the United States, Americans find U.S. bonds more attractive than foreign bonds. When Americans are buying fewer foreign bonds, they are supplying fewer U.S. dollars. The depreciation of the U.S. dollar leads to a larger trade deficit (or reduced surplus). The connections between inflows of foreign investment capital, interest rates, and exchange rates are all just different ways of drawing the same economic connections: a larger budget deficit can result in a larger trade deficit, although the connection should not be expected to be one-to-one.

::也可以想象汇率的这一升值是由利率驱动的。 正如早些时候解释的那样,预算赤字增加了国内金融资本市场的需求,提高了国内利率。 更高的利率将吸引外国金融资本的流入,并随着外国投资者对美元需求的增加和美元供应的减少而升值汇率。 由于美国利率的提高,美国人发现美国债券比外国债券更有吸引力。 当美国人购买的外国债券较少时,他们供应的美国债券就更少了。 美元贬值导致更大的贸易赤字(或盈余减少 ) 。 外国投资资本、利率和汇率的流入都是不同的经济联系方式:更大的预算赤字可能导致更大的贸易赤字,尽管不应该指望这种联系是一对一的。From Budget Deficits to International Economic Crisis

::从预算赤字到国际经济危机The economic story of how an outflow of international financial capital can cause a deep recession is laid out, step-by-step. When international financial investors decide to withdraw their funds from a country like Turkey, they increase the supply of the Turkish lira and reduce the demand for lira, depreciating the lira exchange rate. When firms and the government in a country like Turkey borrow money in international financial markets, they typically do so in stages. First, banks in Turkey borrow in a widely used currency like U.S. dollars or euros, then convert those U.S. dollars to lira, and then lend the money to borrowers in Turkey. If the value of the lira exchange rate depreciates, then Turkey’s banks will find it impossible to repay the international loans that are in U.S. dollars or euros.

::关于国际金融资本的外流会如何导致深度衰退的经济故事已经逐步得到阐述。 当国际金融投资者决定从土耳其这样的国家提款时,他们就会增加土耳其里拉的供应并减少里拉的需求,从而降低里拉的汇率。 当土耳其这样的国家的公司和政府借钱到国际金融市场时,它们通常会分阶段这样做。 首先,土耳其银行以美元或欧元等广泛使用的货币借款,然后将美元兑换成里拉,然后将资金借给土耳其的借款人。 如果里拉汇率贬值,那么土耳其银行将发现无法偿还以美元或欧元计值的国际贷款。The combination of less foreign investment capital and banks that are bankrupt can sharply reduce aggregate demand, which causes a deep recession. Many countries around the world have experienced this kind of recession in recent years: along with Turkey in 2002, this general pattern was followed by Mexico in 1995, Thailand and countries across East Asia in 1997–1998, Russia in 1998, and Argentina in 2002. In many of these countries, large government budget deficits played a role in setting the stage for the financial crisis. A moderate increase in a budget deficit that leads to a moderate increase in a trade deficit and a moderate appreciation of the exchange rate is not necessarily a cause for concern. But beyond some point that is hard to define in advance, a series of large budget deficits can become a cause for concern among international investors.

::减少外国投资资本和破产银行的组合可以大幅降低总需求,从而导致深度衰退。 近年来,世界许多国家都经历了这种衰退:与2002年的土耳其一样,墨西哥在1995年、泰国和东亚各国于1997-1998年、俄罗斯于1998年和阿根廷于2002年都遵循了这一总体模式。 在这些国家中,巨大的政府预算赤字在为金融危机做好准备方面发挥了作用。 预算赤字的适度增长导致贸易赤字温和增长以及汇率适度升值并不一定引起关注。 但除了难以事先界定的一点之外,一系列庞大的预算赤字可能令国际投资者担忧。One reason for concern is that extremely large budget deficits mean that aggregate demand may shift so far to the right as to cause high inflation. The example of Turkey is a situation where very large budget deficits brought inflation rates well into double digits. In addition, very large budget deficits at some point begin to raise a fear that the borrowing will not be repaid. In the last 175 years, the government of Turkey has been unable to pay its debts and defaulted on its loans six times. Brazil’s government has been unable to pay its debts and defaulted on its loans seven times; Venezuela, nine times; and Argentina, five times. The risk of high inflation or a default on repaying international loans will worry international investors, since both factors imply that the rate of return on their investments in that country may end up lower than expected. If international investors start withdrawing the funds from a country rapidly, the scenario of less investment, a depreciated exchange rate, widespread bank failure, and deep recession can occur. The following Clear It Up feature explains other impacts of large deficits.

::令人担心的一个原因是,巨大的预算赤字意味着总需求可能到目前为止可能会转向高通胀。 土耳其的例子就是巨大的预算赤字使通胀率达到两位数。 此外,在某个时刻,巨大的预算赤字开始让人担心借款不会偿还。 在过去的175年中,土耳其政府无力偿还债务并拖欠了六次贷款。 巴西政府无力偿还债务并拖欠了七次贷款;委内瑞拉9次;阿根廷5次。 高通胀或违约偿还国际贷款的风险会令国际投资者担忧,因为这两个因素都意味着他们在该国的投资回报率可能比预期的要低。 如果国际投资者开始迅速从一个国家撤出资金,投资减少、汇率贬值、银行破产和严重衰退的情况就会发生。 之后的“清廉”特征解释了巨额赤字的其他影响。What are the Risks of Chronic Large Deficits in the United States?

::美国慢性大短缺的风险是什么?If a government runs large budget deficits for a sustained period of time, what can go wrong? According to a recent report by the Brookings Institution, a key risk of a large budget deficit is that government debt may grow too high compared to the country’s GDP growth. As debt grows, the national savings rate will decline, leaving less available in financial capital for private investment. The impact of chronically large budget deficits is as follows:

::如果政府持续地存在巨额预算赤字,又会出什么问题? 根据布鲁金斯学会最近的报告,大规模预算赤字的一个关键风险是政府债务可能比国家GDP增长高。 随着债务增长,国民储蓄率将下降,私人投资的金融资本将减少。 长期巨额预算赤字的影响如下:-

As the population ages, there will be an increasing demand for government services that may cause higher government deficits. Government borrowing and its interest payments will pull resources away from domestic investment in human capital and physical capital that is essential to economic growth.

::随着人口老化,对政府服务的需求将不断增加,这可能导致政府赤字增加。 政府借贷及其利息支付将占用国内人力资本和对经济增长至关重要的有形资本投资的资源。 -

Interest rates may start to rise so that the cost of financing government debt will rise as well, creating pressure on the government to reduce its budget deficits through spending cuts and tax increases. These steps will be politically painful, and they will also have a contractionary effect on aggregate demand in the economy.

::利率可能会开始上升,这样政府债务融资成本也会上升,从而给政府带来压力,要求政府通过削减支出和增加税收来减少预算赤字。 这些步骤在政治上将是痛苦的,也会对经济总需求产生收缩效应。 -

Rising percentage of debt to GDP will create uncertainty in the financial and global markets that might cause a country to resort to inflationary tactics to reduce the real value of the debt outstanding. This will decrease real wealth and damage confidence in the country’s ability to manage its spending. After all, if the government has borrowed at a fixed interest rate of, say, 5%, and it lets inflation rise above that 5%, then it will effectively be able to repay its debt at a negative real interest rate.

::债务占GDP的百分比上升将给金融和全球市场带来不确定性,从而可能导致一个国家采用通胀策略来降低未偿债务的实际价值。 这将减少实际财富并损害对国家管理支出能力的信心。 毕竟,如果政府以固定利率(比如5 % ) 5%的利率借款,让通胀超过5 % , 那么它就能以负实际利率有效地偿还债务。

The conventional reasoning suggests that the relationship between sustained deficits that lead to high levels of government debt and long-term growth is negative. How significant this relationship is, how big an issue it is compared to other macroeconomic issues, and the direction of causality, is less clear.

::传统推理认为,导致政府债务高水平的持续赤字与长期增长之间的关系是消极的。 这种关系有多重要,与其他宏观经济问题相比问题有多大,以及因果关系的方向如何,都不太清楚。What remains important to acknowledge is that the relationship between debt and growth is negative and that for some countries, the relationship may be stronger than in others. It is also important to acknowledge the direction of causality: does high debt cause slow growth, slow growth cause high debt, or are both high debt and slow growth the result of third factors? In our analysis, we have argued simply that high debt causes slow growth. There may be more to this debate than we have space to discuss here.

::必须承认的是,债务与增长之间的关系是消极的,对某些国家来说,这种关系可能比其他国家更牢固,同样重要的是承认因果关系:高债务是造成缓慢增长,缓慢增长导致高债务,还是高债务和缓慢增长都是第三个因素造成的?我们的分析认为,高债务造成缓慢增长,高债务造成缓慢增长。我们的辩论可能比我们在这里讨论的空间还要多。Using Fiscal Policy to Address Trade Imbalances

::利用财政政策解决贸易不平衡问题If a nation is experiencing the inflow of foreign investment capital associated with a trade deficit because foreign investors are making long-term direct investments in firms, there may be no substantial reason for concern. After all, many low-income nations around the world would welcome direct investment by multinational firms that ties them more closely into the global networks of production and distribution of goods and services. In this case, the inflows of foreign investment capital and the trade deficit are attracted by the opportunities for a good rate of return on private sector investment in an economy.

::如果一个国家正在经历与贸易赤字相关的外国投资资本流入,因为外国投资者正在对公司进行长期直接投资,那么就没有理由担心。 毕竟,全世界许多低收入国家都欢迎跨国公司的直接投资,这些跨国公司将它们更紧密地连接到商品和服务生产和分销的全球网络中,在这种情况下,外国投资资本流入和贸易赤字被私营部门对经济的投资获得良好回报的机会所吸引。However, governments should beware of a sustained pattern of high budget deficits and high trade deficits. The danger arises in particular when the inflow of foreign investment capital is not funding long-term physical capital investment by firms, but instead is short-term portfolio investment in government bonds. When inflows of foreign financial investment reach high levels, foreign financial investors will be on the alert for any reason to fear that the country’s exchange rate may decline or the government may be unable to repay what it has borrowed on time. Just as a few falling rocks can trigger an avalanche; a relatively small piece of bad news about an economy can trigger an enormous outflow of short-term financial capital.

::然而,政府应该警惕预算赤字和贸易赤字高企的持久模式。 特别是当外国投资资本的流入不是为企业的长期实物资本投资提供资金,而是为政府债券的短期证券投资提供资金时,风险就出现了。 当外国金融投资的流入达到高水平时,外国金融投资者会因为担心国家汇率可能下降或政府可能无法及时偿还贷款而处于警戒状态。 正如几起下跌的岩石可能引发雪崩一样;一小段关于一个经济体的坏消息可能会引发短期金融资本的巨大外流。Reducing a nation’s budget deficit will not always be a successful method of reducing its trade deficit, because other elements of the national saving and investment identity, like private saving or investment, may change instead. In those cases when the budget deficit is the main cause of the trade deficit, governments should take steps to reduce their budget deficits, lest they make their economy vulnerable to a rapid outflow of international financial capital that could bring a deep recession.

::减少一个国家的预算赤字并不总是一个减少其贸易赤字的成功方法,因为国民储蓄和投资身份的其他要素,如私人储蓄或投资,可能会相反地发生变化。 在预算赤字是贸易赤字主要原因的情况下,政府应该采取措施减少预算赤字,以免其经济受到可能导致深度衰退的国际金融资本快速外流的影响。The government need not balance its budget every year. However, a sustained pattern of large budget deficits over time risks causing several negative macroeconomic outcomes: a shift to the right in aggregate demand that causes an inflationary increase in the price level; crowding out private investment in physical capital in a way that slows down economic growth; and creating a dependence on inflows of international portfolio investment which can sometimes turn into outflows of foreign financial investment that can be injurious to a macroeconomy.

::政府不必每年平衡预算。 然而,长期持续的大量预算赤字可能会带来若干负面宏观经济结果:转向总需求右,导致物价水平的通胀性上涨;以减缓经济增长的方式排挤对实物资本的私人投资;以及造成对国际证券投资流入的依赖,这些流入有时会转化为外国金融投资的流出,从而损害宏观经济。Answer the self check questions below to monitor your understanding of the concepts in this section.

::回答下面的自我核对问题,以监测你对本节概念的理解。Self Check Questions

::自查问题1. What is the federal spending deficit? What will the federal government need to do if it runs a deficit?

::1. 联邦支出赤字是什么?联邦政府如果出现赤字需要做什么?2. What is the federal debt?

::2. 联邦债务是多少?3. Define the term "balanced budget."

::3. 界定“平衡预算”一词的定义。4. Go online and research what the current national debt is. Research to answer the question: What impact does the national debt have on the federal government?

::4. 上网研究当前的国民债务是什么,研究回答问题:国民债务对联邦政府有什么影响?5. Go online and research the Gramm-Rudman-Hollings Act of 1985 (also known as the Balanced Budget and Emergency Deficit Control Act of 1985). Why did it fail?

::5. 上网研究1985年《格拉姆-鲁德曼-霍林斯法》(又称1985年《平衡预算和紧急赤字控制法》),为何失败?6. Go online and research the Budget Enforcement Act of 1990. Was it successful? Why or why not?

::6. 上网研究1990年《预算执行法》是否成功?为什么不成功?7. Why was 1998 an important year in federal spending? Go online and research the reasons for the budget surplus.

::7. 为什么1998年是联邦开支的一个重要年头?8. What are entitlements? How can this spending category impact the federal budget? Give an example.

::8.什么是应享权利?这种支出类别如何影响联邦预算?举一个例子。 -

Deficit spending has helped to create the national debt.